Nvidia has released its highly anticipated Q3 2026 earnings and Q4 (Q426) guidance, delivering an impressive beat-and-raise accompanied by extremely bullish commentary on GPU demand. Investors are well conditioned to Nvidia beating expectations—yet despite the high bar, the company has once again exceeded key metrics.

Market Reaction: Strong Gains Across NVDA, Semis, and the NASDAQ

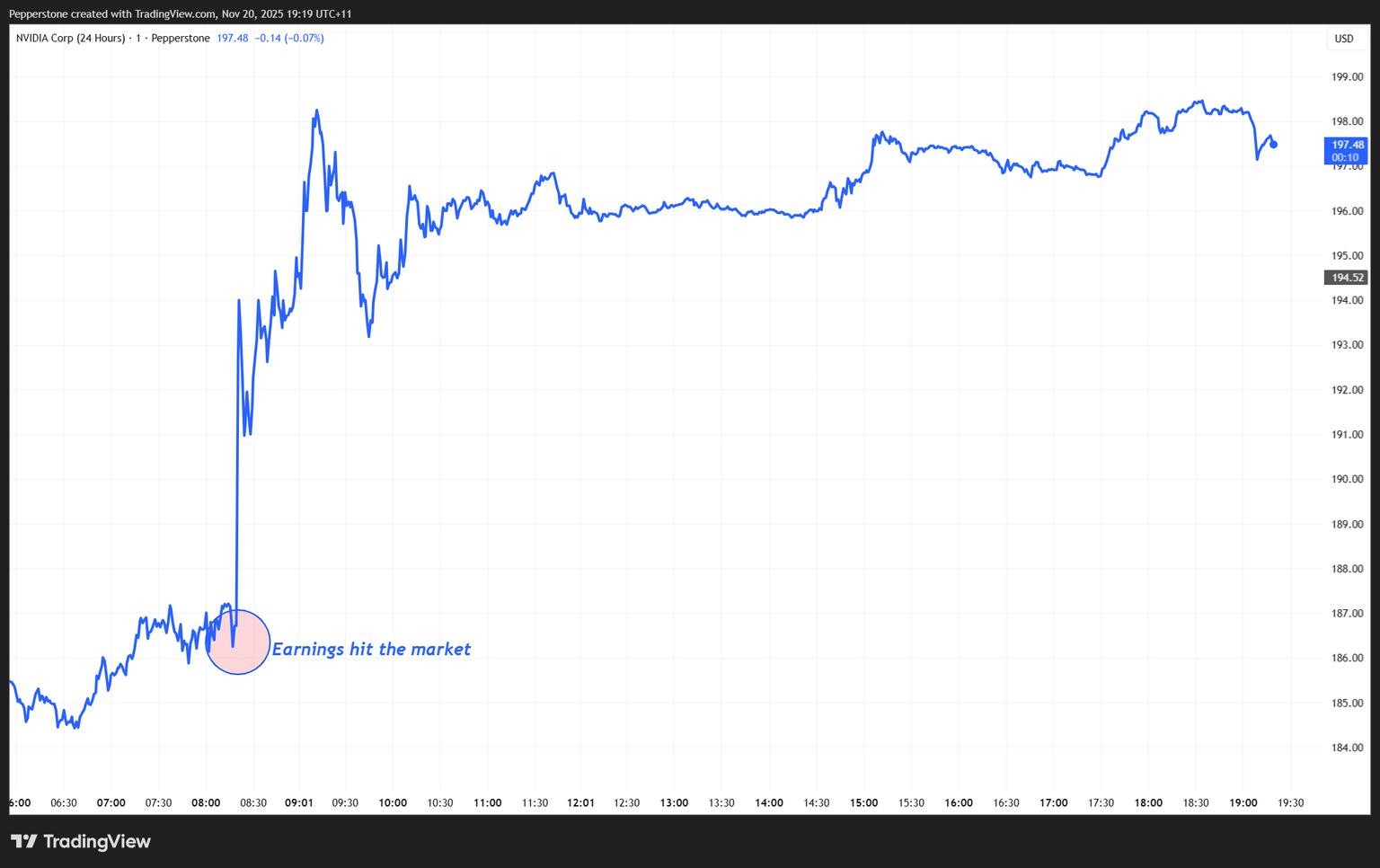

Nvidia 24-hour CFDs rallied to a session high of $198.53 (+6.2%) following the earnings release. The positive sentiment spread quickly:

• The broader semiconductor sector strengthened

• NASDAQ 100 futures gained +1.8%

Traders are now asking whether these results are enough to reverse the recent negative sentiment surrounding AI and semiconductors—and whether Nvidia can:

• Push back above $200, and

• Re-test the all-time high of $212.11

Alternatively, some caution that the earnings rally could fade if investors sell into strength, dragging price back toward key support at $179.20.

My view: The higher-probability outcome is a run toward the all-time highs.

Key Results: Nvidia’s Q3 Earnings and Q4 Guidance

The Numbers That Have Hit Home:

• Q3 sales: $57B vs. $55.2B expected

• Q4 revenue guidance: $65B vs. $62B expected

• Q3 gross margin: 73.6% (in line)

• Q4 gross margin guidance: 75% vs. 74.7% expected

• Data-center revenue: $51.2B vs. $49.34B expected

Despite elevated expectations, Nvidia delivered a solid beat on Q3 results, and the $3B beat on Q4 revenue guidance was the standout metric driving the stock higher. With gross margins trending up and Nvidia’s flawless track record of over-delivering, the company continues to cement its position as the premier AI play across both training and inference.

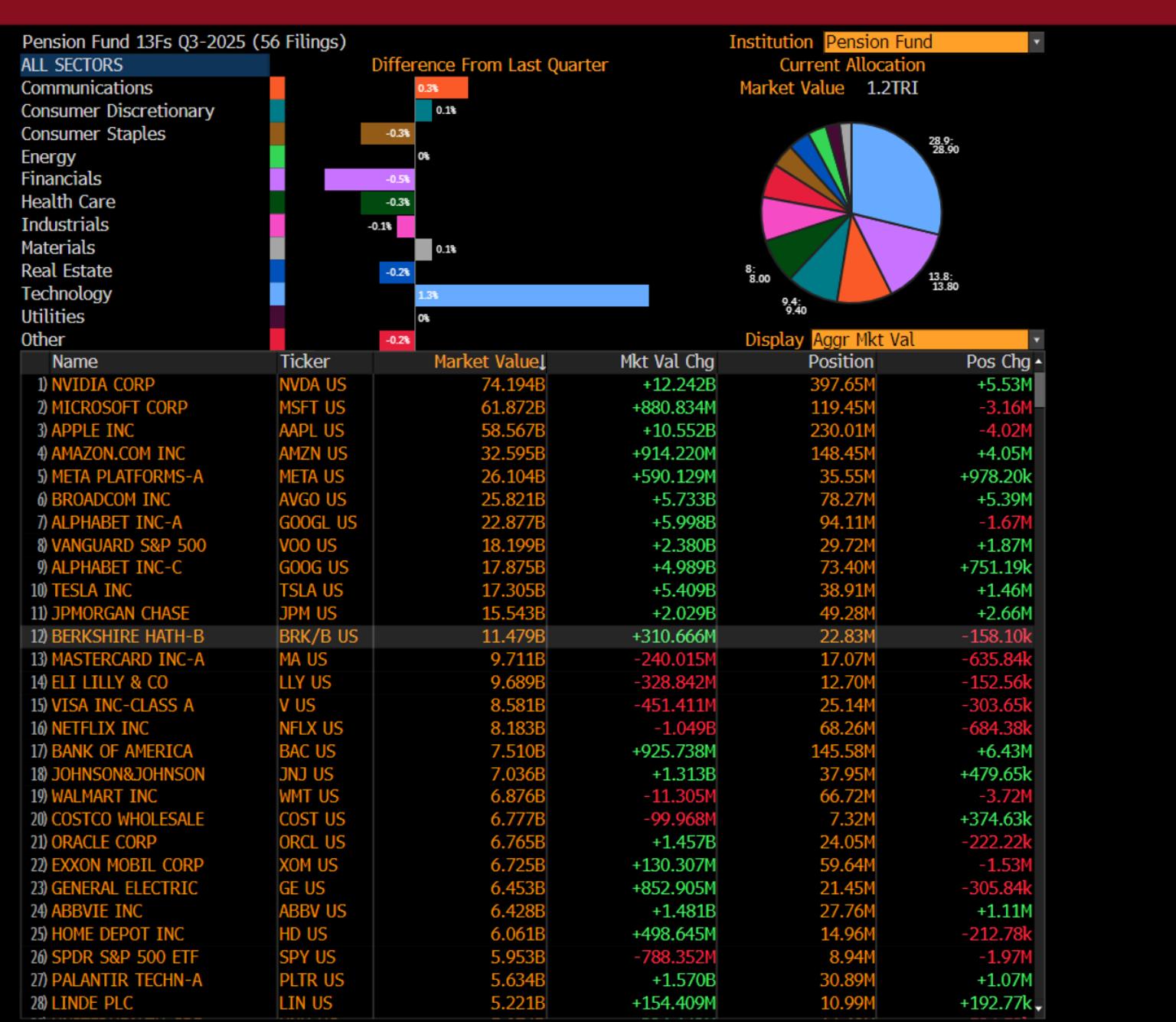

Institutional ownership remains enormous—397 million Nvidia shares are held by pension funds and asset managers, more than three times the next-largest S&P 500 holding (Microsoft). Nvidia’s 8% index weight makes it a mandated holding for many.

Explosive Demand for Blackwell Architecture

Investors weren’t only impressed by the numbers, the commentary around demand was extraordinarily bullish. As expected, CEO Jensen Huang offered a positive outlook, but the tone was particularly strong.

Key highlights from management:

• “Blackwell GPUs are sold out”

• Demand for Blackwell chips described as “off the charts”

• Blackwell is now Nvidia’s leading architecture

• Nvidia’s cloud GPUs are sold out

This messaging underscores Nvidia’s continued dominance in AI compute and the near-limitless appetite for its GPU ecosystem.

Where Nvidia Fell Slightly Short: OpEx and Free Cash Flow

A few areas came in softer than expected:

• Operating expenses: $5.0B (slightly above forecasts)

• Free cash flow: $22B vs. ~$28B expected

However, neither metric was large enough to dent sentiment, with the market focused squarely on the strength of revenue, margins, and forward demand.

Bottom Line: Nvidia Delivers Another Impressive Quarter

Nvidia exceeded expectations across the board, delivering:

• A major Q3 revenue beat

• Strong Q4 guidance

• Explosive data-center growth

• Red-hot demand for Blackwell GPUs

• Strong and rising gross margins

Despite minor softness in operating expenses and free cash flow, Nvidia remains the clear global leader in AI compute. The business is in a true “sweet spot,” and lingering concerns about an “AI bubble” have been tempered by overwhelming demand for Nvidia’s products—suggesting any meaningful risk is a post-2027 story at the earliest.

For traders, the focus now shifts to whether analysts revise earnings estimates higher, and whether the market decides to chase the move.

Good luck to all.

.png?format=pjpg&auto=webp&width=1536&quality=75&branch=main)