Summary

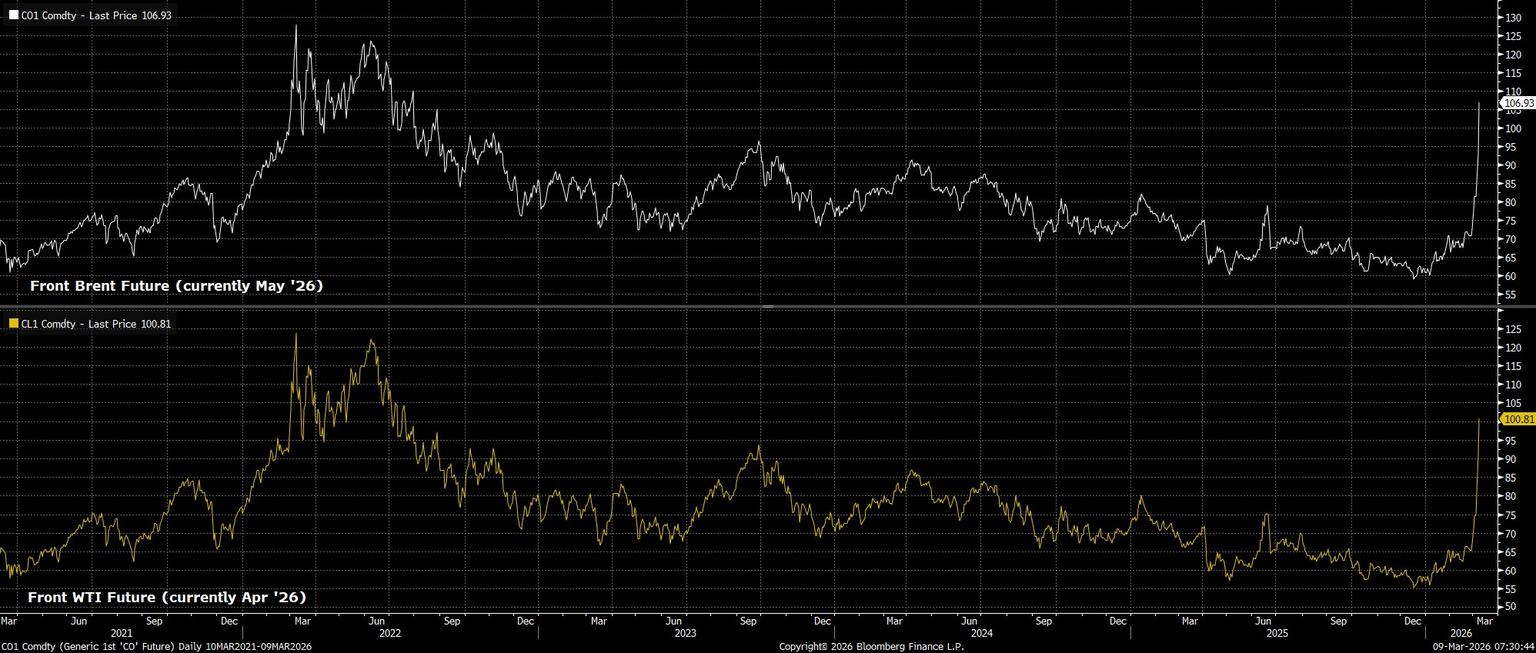

- Crude Surges: Continued supply disruption as the Strait of Hormuz remains impassable has lifted both Brent & WTI north of $100bbl to start the new trading week

- Broader Risk Aversion: In turn, the continued energy shock has led to broad-based de-risking, as stocks face headwinds, gold rolls over, and the dollar remains the only true safe haven

- Zooming Out: The impact of the commodity shock will hinge largely on its duration, though participants are now pondering whether financial market pressure may force the Trump Admin into a U-turn

Geopolitical events remain ‘front and centre’ for market participants, as the week begins on a risk-averse note, with most assets continuing to display a very tight correlation indeed with crude benchmarks.

Crude Benchmarks Surge

Said benchmarks, both front Brent and front WTI, have now risen north of $100bbl, up as much as 30% apiece, after a weekend where there was little-to-no sign of de-escalation in terms of tensions in the Middle East. Not only that, but in some respects the conflict has escalated, after the targeting of domestic energy infrastructure inside Iran, though at this stage export facilities remain unharmed.

Still, the Strait of Hormuz remains essentially impassable, meaning that physical conditions within the crude market continue to tighten, not helped by various Gulf states being forced to cut crude output in order to prevent storage from filling, and a complete production halt being required.

At this stage, so long as Hormuz remains impassable, conditions are likely to tighten further, exerting upward pressure on price. While a G7 SPR release is now being rumoured, this would more likely be a short-term psychological measure, as opposed to one that eases all physical stress. In fact, the only durable way to do that is to ensure safe transit of the Strait – be that, insurance guarantees, US Navy escorts, an end to the conflict, or some combination of those factors.

Participants De-Risk Across The Board

As noted, markets continue to react to this commodity shock in fairly ‘textbook’ manner – Govvies soften given expectations for higher inflation and a more hawkish policy stance; energy-importing FX (e.g. GBP, EUR, JPY) sinks to the bottom of the leaderboard; while, amid that sell-off in DM rates, gold faces stiff headwinds. Naturally, stocks continue to soften too. In fact, the only real haven remains the greenback, as participants broadly de-risk their portfolios, and seek shelter in cash for the time being.

Interestingly, all of that is the exact opposite of President Trump’s stated aims when it comes to financial markets. On numerous occasions, Trump has noted his desire for lower oil prices, higher stock prices, a weaker dollar, lower rates, and a more dovish Fed. What he’s actually getting right now is higher oil prices, lower stock prices, a stronger dollar, higher rates, and a Fed that’s stuck between a ‘rock and a hard place’.

Testing The ‘Trump Put’

I suppose, then, that this is the time that we put the ‘Trump put’ structure to the test. To be clear, I’m not saying that we are immediately going to see a U-turn, or another ‘TACO’ moment. In fact, I’d wager that ‘TACO-ing’ your way out of a geopolitical conflict is orders of magnitude harder than doing so out of some tariffs.

However, it does seem as if we are getting towards a stage where various ‘pressure points’ are increasingly being pressed, and pressed very hard indeed. That’s before, of course, considering the electoral implications of the now-inevitable spike in gasoline prices, at a time when ‘affordability’ was already a totemic issue ahead of November’s midterm elections. Furthermore, when one considers the rather ambiguous aims for the US operation in Iran, which don’t appear to have quantifiable goals, there is a world in which ‘mission accomplished’ could be declared simply in an effort to becalm financial markets.

Short-Term Turbulence, or Longer-Run Hit?

All that said, we don’t seem to be at that stage yet, and for the time being the general mood among market participants is one of ‘sell first, ask questions later’, as participants seek to, or are forced to, take down risk levels as both implied and realised vol surge. Against that backdrop, this is the sort of situation where a substantial move in the energy complex can kick-off a spiral of hysteria and panic, where participants all seek to head for the exit at the same time, as the macro outlook is turned on its head.

The extent of any macro impact, though, depends entirely on how long the present commodity shock lasts.

Here, I would note that moves remain afoot to ensure safe transit through Hormuz, via insurance guarantees and US Navy escorts, with significantly higher crude prices likely hastening progress on that front. My view remains that all this is more likely to prove short-term market turbulence, as opposed to a longer-run turning point for markets and the economy, though the more protracted conflict proves to be, the more risks will tilt in favour of the latter, more bearish, scenario.