The initial market reaction to President Trump's weekend threat to tariffs of 10%, potentially increasing to 25% at a later date, on a host of European nations in relation to the US seeking to gain control of Greenland has been a relatively predictable one; albeit, with the important caveat that trade in the G10 FX market is always incredibly thin at this time of the week, more so this week with US markets closed for MLK Day tomorrow.

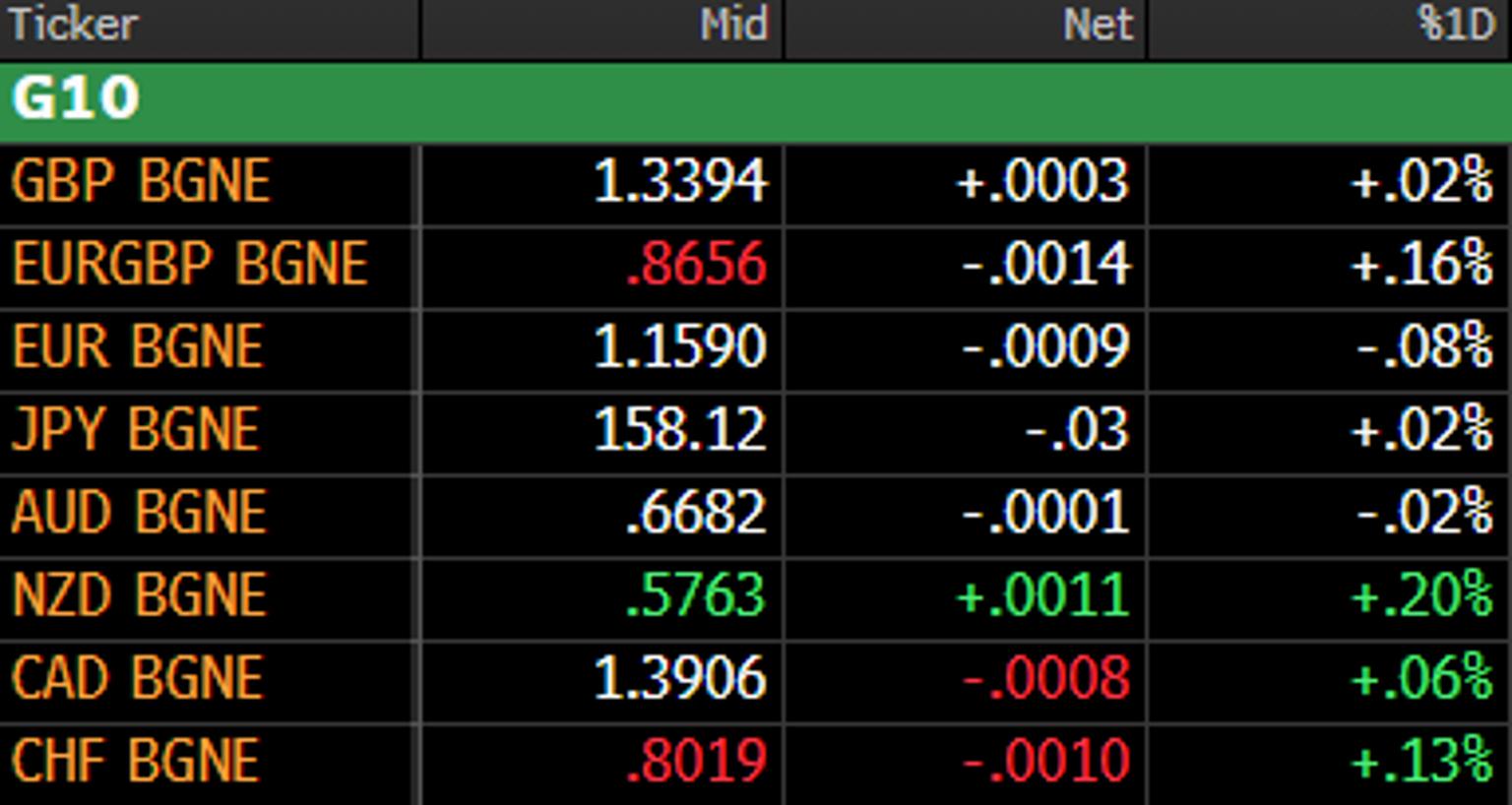

Perhaps surprisingly, foreign exchange traders appear to be taking things relatively in their stride for the time being, with both the GBP and EUR little changed in early trade, and with just the slightest hint of haven demand for the CHF also making itself known. Conditions are, however, on the whole, more muted than one might've reasonably expected. Prices below are as of the Wellington open (6pm GMT, Sunday):

That said, one would still expect a relatively risk-averse open for equity futures a little later on this evening, while there is little to suggest that the recent rally in precious metals could take a pause for breath, with further gains in both gold and silver likely.

Clearly, participants' focus, once risk has been managed, and exposures trimmed as deemed appropriate, will relatively rapidly turn to what comes next. Potential European retaliation is the first area to watch here, with France pushing for use of the EU's 'anti coercion instrument', and EU ambassadors due to meet tonight. Use of the ACI, however, in my view, would be counter-intuitive; akin to the EU saying 'the US have shot themselves in the foot, let's now do the same thing', not least considering that it will be US consumers footing the bill for the bulk of these tariffs, if they go into effect.

That, of course, is not guaranteed, and yet again the entire tariff threat does seem to be constructed as a negotiating gambit, in an attempt by the Trump Admin to gain leverage, focus minds, extract concessions, and achieve some sort of a 'deal' in shorter order. It is likely no coincidence that the threat has come on the eve of the WEF in Davos this week. There are also question marks over the legal justification that could be used for these tariffs, with a Supreme Court ruling on the IEEPA potentially coming as soon as this week.

By and large, then, my working assumption is that an 'off ramp' from these threats will soon be found, and that this turns into yet another 'TACO moment', or an example of the 'art of the deal', depending on how one views these things. Against that backdrop, with the fundamental bull case for risk still a resilient one, and providing that any European retaliation remains largely rhetorical, I would view equity dips as buying opportunities for now, and wouldn't be surprised to see the week's initial FX moves fade relatively rapidly either.

.png?format=pjpg&auto=webp&width=1536&quality=75&branch=main)