April 2026 FOMC Preview: Still In ‘Wait & See’ Mode As Powell’s Departure Nears

Summary

- Standing Pat: The FOMC are set to maintain the target range for the fed funds rate at 3.50% - 3.75%, in an 11-1 vote

- Unchanged Guidance: Policymakers will likely reiterate a 'data-dependent', 'wait and see' approach, while noting the 'uncertain' implications of recent geopolitical events

- Handover: Chair Powell's post-meeting press conference may prove to be his final one, as the nomination of Kevin Warsh to succeed him as Chair from mid-May makes its way through the Senate

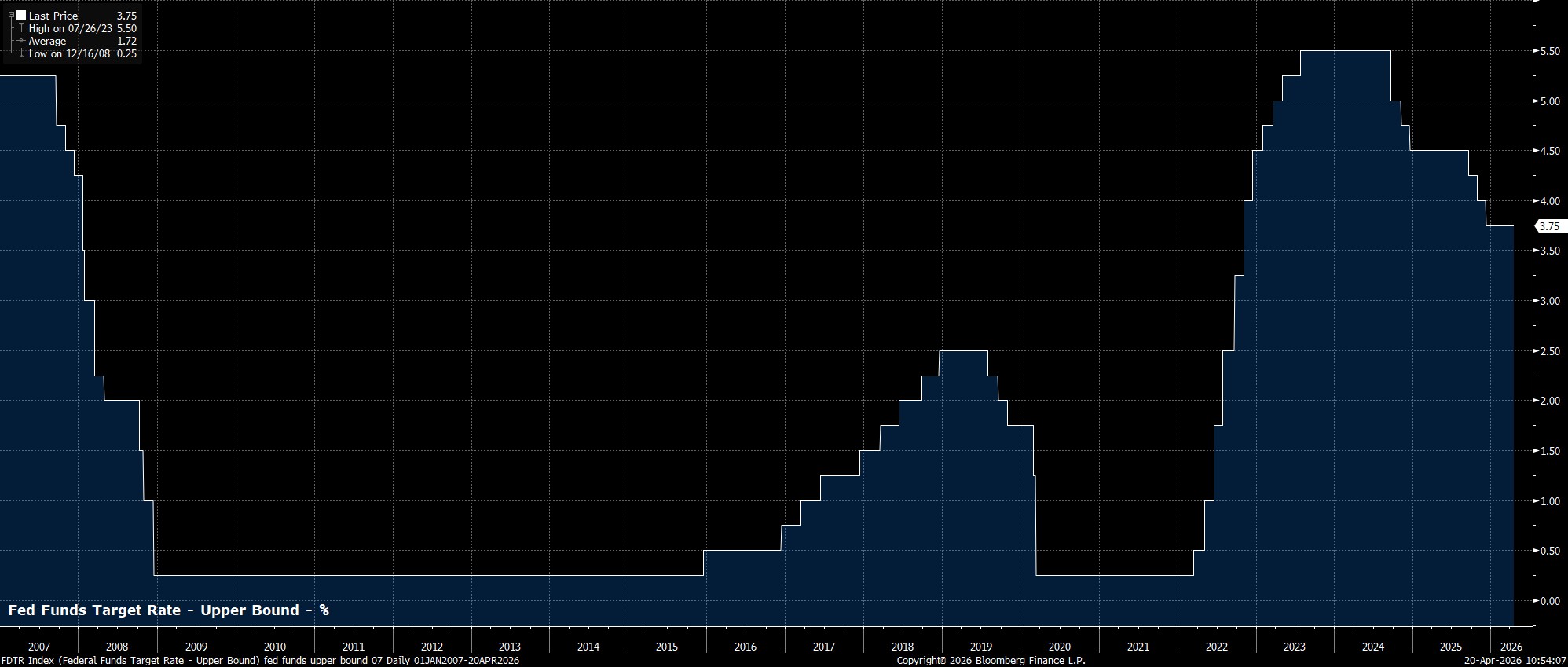

Policy Pause To Continue

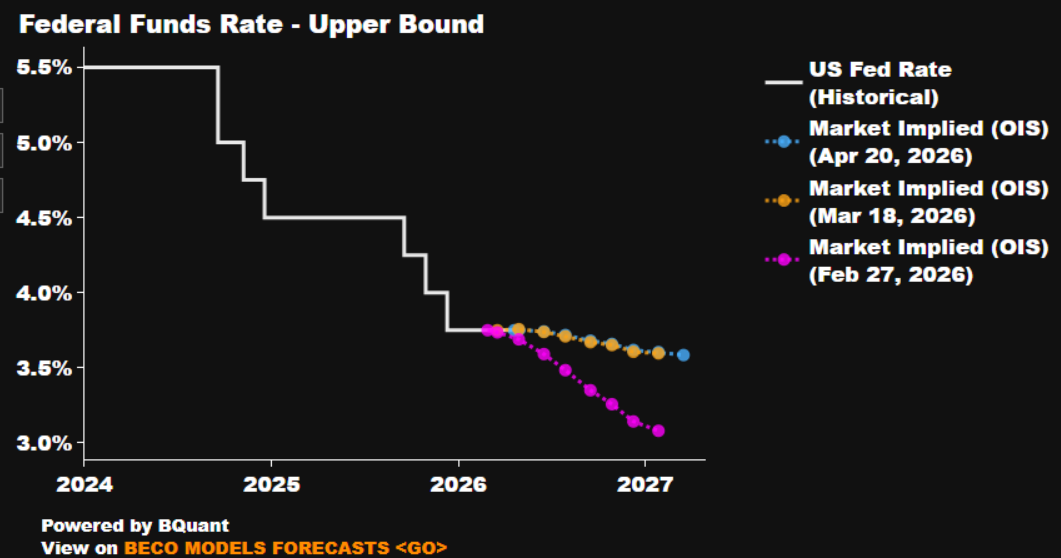

As mentioned, the FOMC are set to stand pat at the April meeting, maintaining the target range for the fed funds rate at 3.50% - 3.75%, and as such extending a policy pause which begun at the turn of the year. Money markets, per the USD OIS curve, discount no chance of any policy action at the upcoming meeting, though do price around 12bp of easing by year-end, implying a roughly even chance of a sole rate reduction being delivered by December.

Once again, though, the Committee will likely be divided as to the appropriate course of policy action.

At the March meeting, the FOMC voted by 11-1 to stand pat, and such a vote is likely to be seen again this time out, with only Governor Miran dissenting in favour of a 25bp cut. Other potential dovish dissenters, such as Governors Waller and Bowman, have noted a preference for further rate reductions in recent remarks, though both are likely to seek further clarity on the economic impact of conflict in the Middle East, before voting in favour of a rate cut.

Commentary Likely Little Changed

Meanwhile, in the accompanying policy statement, the FOMC are likely to repeat the relatively ‘boilerplate’ language that was used in terms of both the economic assessment, and policy guidance, last time out.

As such, the economy is set to be described as having grown at a ‘solid pace’, despite the recent downwards revision to the shutdown-impacted Q4 GDP report, with inflation still ‘somewhat elevated’, and unemployment ‘little changed’.

In terms of guidance, the statement should reiterate the Committee’s data-dependent approach to future decisions, while again noting that the impact of recent events in the Middle East on the US economy is ‘uncertain’. Were the Committee so minded, they may seek to elaborate on this, noting the potential for developments to create ‘upward pressure on inflation and…weigh on economic activity’, mirroring language used in the aftermath of Russia’s invasion of Ukraine around four years ago.

Assessing Recent Economic Developments

Since the March FOMC meeting, conflict in the Middle East has continued and, as at the time of writing, a formal peace deal to bring hostilities to a durable end has yet to be agreed.

Despite that, and the Strait of Hormuz remaining essentially impassable, crude futures have modestly retraced in the month following the last confab, with front WTI trading around 10% below where it was the last time that the FOMC sat round the table in the Eccles Building.

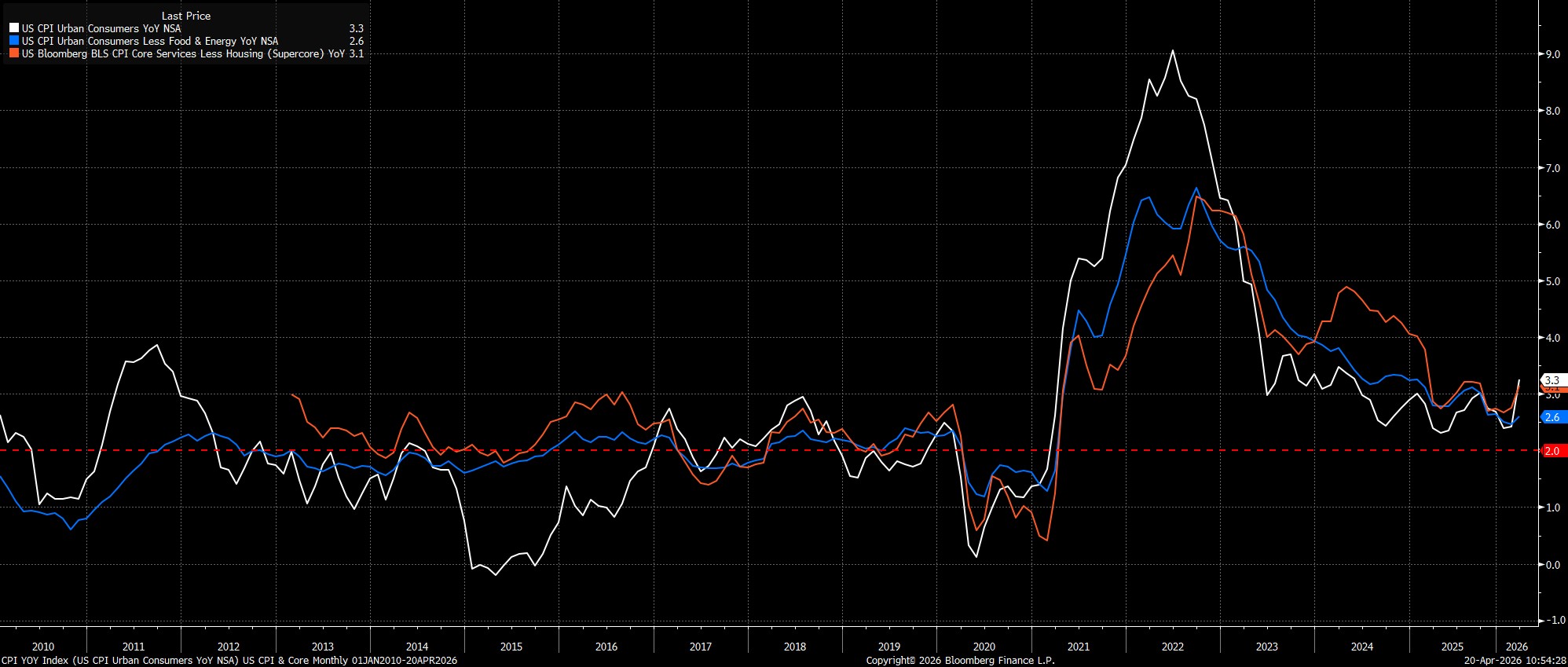

That said, headline inflation did nonetheless jump in March, with CPI rising 0.9% MoM, the biggest one-month increase in almost four years, and by 3.4% YoY, the fastest annual rate since May 2024. Core inflation metrics, though, remained somewhat more subdued, at 0.2% MoM/2.6% YoY likely, for now, lessening some concern that higher energy prices may result in more broad-based price pressures.

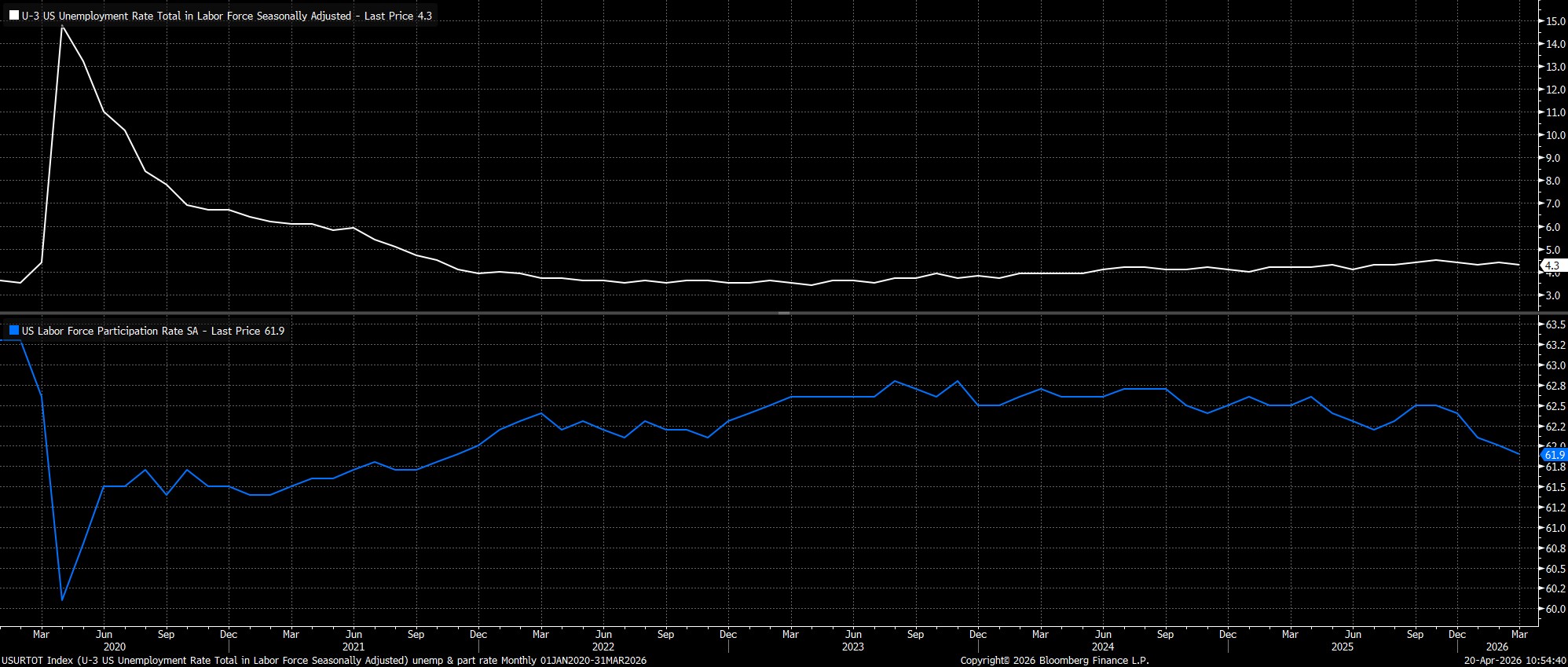

Furthermore, the labour market backdrop remains fragile, with the ‘no hire, no fire’ dynamic continuing. While headline payrolls did rise by +178k in March, this came on the back of a -133k decline in February, with such large swings in headline payrolls figures increasingly likely to be seen, with the breakeven pace of job growth now at, or approaching, zero. Hence, the household survey is likely a considerably better indicator of labour market conditions at this stage.

On this note, and reflecting the delicate balance in which the labour market currently finds itself, unemployment dipped marginally to 4.3% in March, though this decline was entirely by virtue of a further decline in labour force participation, which fell to fresh cycle lows at 61.9%. All in all, the latest labour market data not only suggest that the risk of second-round inflation effects is relatively low, amid broadly target-consistent earnings growth, but also that the employment backdrop could well warrant additional policy support at the current juncture.

(Possibly) Powell’s Last Presser

Turning to the post-meeting press conference, there is every chance that this will prove the final time we hear Chair Powell’s dulcet tones, and the familiar reassurance of Powell’s “good afternoon” opening line.

While the nomination of Kevin Warsh to succeed Powell as Chair is somewhat stalled in the Senate, as a result of the ongoing DoJ investigation ostensibly regarding the Fed’s building renovations, senior administration officials believe that Warsh will be confirmed to the Chair role by mid-May. In any case, Chair Powell did stress, at the March press conference, that he would remain on the Board ‘until the investigation is well and truly over, with transparency and finality’.

As for near-term policy matters, concrete guidance is likely to be relatively thin on the ground, understandably so considering the fluid economic outlook. Consequently, Powell will likely reiterate his recent view that policy is in a ‘good place to wait and see’, while also noting that inflation expectations remain ‘well-anchored’ and that policymakers need to ‘balance risks’ facing each side of the dual mandate.

Conclusion

To conclude, the FOMC are overwhelmingly likely to stand pat at the April meeting, which could prove to be Powell’s last as Chair.

That said, with the impact of higher energy prices on headline inflation set to be temporary in nature, and with the potential for second-round inflation risks to materialise remaining relatively low, the direction of travel for the fed funds rate remains lower. In fact, once policymakers have obtained sufficient confidence to ‘look through’ any ‘hump’ in headline inflation, there remains a path for a couple of rate cuts to be delivered in the second half of the year, as focus pivots back to the employment side of the dual mandate, and a labour market that could well use a less restrictive policy stance.

Pepperstone不保证这里提供的材料准确、最新或完整,因此不应依赖这些信息。这些信息,无论来自第三方与否,不应被视为推荐;或者买卖的要约;或者购买或出售任何证券、金融产品或工具的邀约;或者参与任何特定的交易策略。它不考虑读者的财务状况或投资目标。我们建议阅读此内容的任何读者寻求自己的建议。未经Pepperstone批准,不得转载或重新分发这些信息。