Macro Trader: Hawkish Fed Repricing Has Run Too Far

Something that seems to have, rather suddenly, captured a lot of attention over the last couple of days has been the SOFR options market, and the probabilities that said market implies for the likely path of the fed funds rate over the remainder of the year.

The reason this, perhaps previously relatively niche, market has attracted such focus recently is due to the rather eye-catching nature of the recent hawkish repricing that begun in the aftermath of the March CPI report, which surprised to the upside of consensus expectations for the third month running.

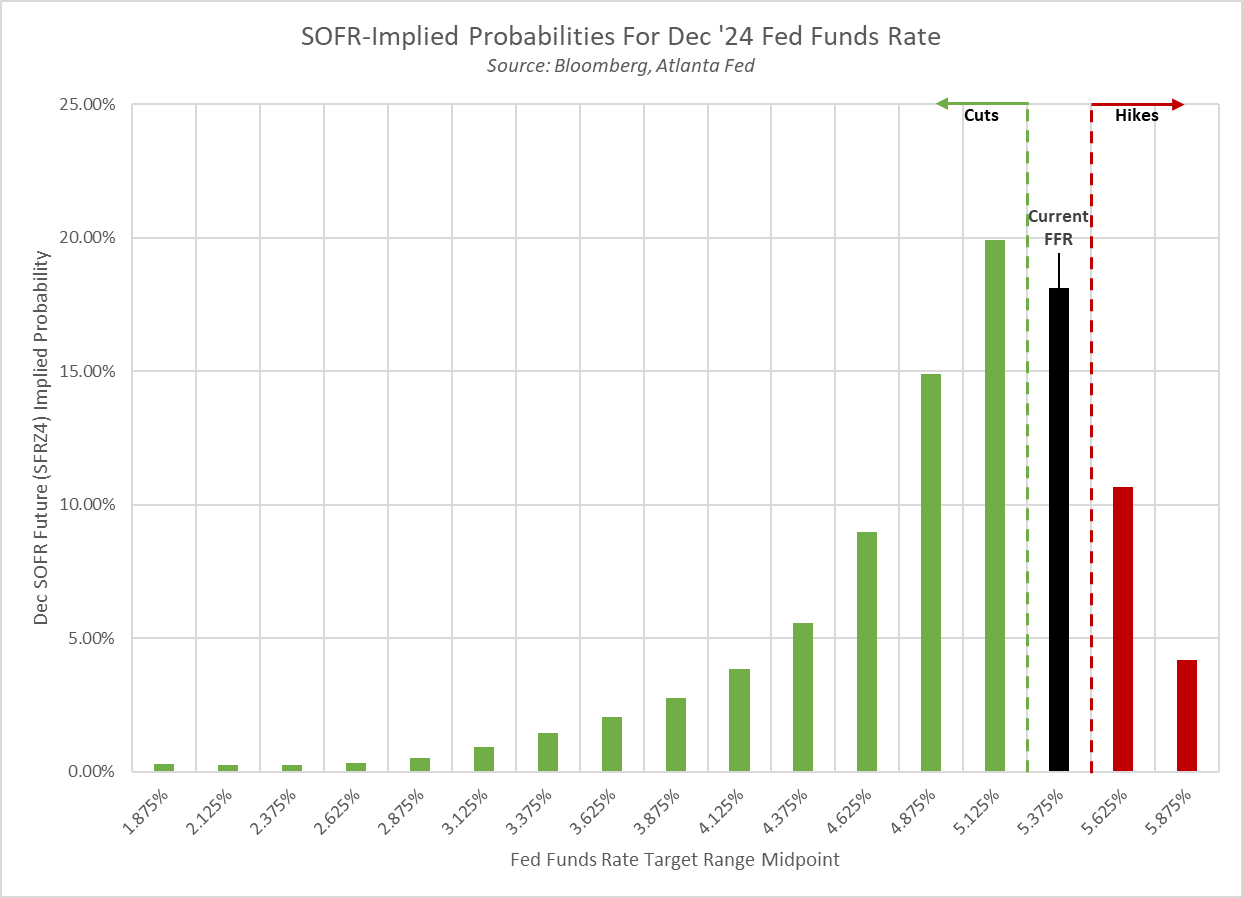

Using SOFR options pricing (derivatives on futures based upon expectations of the 3-month SOFR rate at a time in the future) as a proxy for the fed funds rate, one can derive not only a median expectation for where markets expect overnight rates to settle, but also derive a probability distribution covering a range of potential rate outcomes. This is where things begin to get interesting, with the aforementioned probability distribution showing that options, roughly, price around a 15% chance of a Fed hike by the end of the year.

There are a few things to digest here.

Firstly, the actual statement itself, “15% chance of a hike”, is perhaps a little disingenuous.

While that is indeed what the probability distribution implies, and is factually correct, one must recall that a significant degree of options volume is associated with hedging flows. Hence, contracts traded at a price below that of the current front SOFR level (i.e., yield > current spot) may just as easily be institutional investors mitigating the risk associated with positions elsewhere, rather than outright bets on the Fed pulling an uber-hawkish pivot and raising rates once more. In fact, I would wager that this represents the bulk of the activity taking place in this part of the market.

Secondly, based on the above pricing, it feels safe to say that the hawkish repricing the market has undergone of late, now seeing just 42bp of cuts by year-end, compared to around double that a month ago, has gone to a relatively extreme level, with the curve likely having moved too far, too fast, in a hawkish direction.

This leaves scope for a retracement not only in the STIRs space, but also at the front-end of the Treasury curve, where the 2-year yielding as near as makes no difference 5% is likely to prove an appealing prospect for buyers, mere months ahead of the likely start of policy normalisation.

Thirdly, we must consider recent Fed communication, and whether the prospect of a hike is a realistic one. To put it bluntly, right now, it clearly isn’t.

The FOMC have, perhaps in contrast to other G10 central banks, been incredibly clear in their communication of late. Chair Powell has summed this up best, noting that recent inflation data has shown a lack of further progress, and that it is “appropriate” to give policy further time to work, given that it will “likely” now take longer than previously thought to obtain the necessary confidence in inflation returning towards the 2% target. In other words, rates remaining ‘higher for longer’.

This is a stance that has been mirrored by plenty of other FOMC members, with almost all singing from the same hymn sheet, being in no rush to cut rates, while being prepared to hold rates at their current level for as long as necessary in order to bear down on price pressures.

While there have – notably from Williams and Bostic – been mentions of the possibility of another hike, these remarks have typically followed explicit questioning on the matter. This leads to something of a bind for a central banker, with it being impossible to rule out such action, in order to avoid becoming a hostage to fortune, but at the same time needing to stress that a hike is not the base case. Communicating this optionality, albeit surrounding a very low probability outcome, is ‘central banking 101’ and doesn’t provide much, if anything, by way of policy signal.

As a result, it remains the case that the most likely next move in the fed funds rate will be a cut. In terms of the medium-run outlook for risk assets, this supportive policy backdrop should continue to encourage investors to move further out the risk curve, keeping dips relatively shallow, volatility subdued, and the path of least resistance leading to the upside.

Naturally, this view would be invalidated if FOMC officials were to seriously endorse the prospect of further tightening being required though any such pivot appears unlikely at present, even if inflation remains relatively stubborn.

Related articles

此处提供的材料并未按照旨在促进投资研究独立性的法律要求进行准备,因此被视为营销沟通。虽然它并不受到在投资研究传播之前进行交易的任何禁令,但我们不会在向客户提供信息之前谋求任何优势。

Pepperstone并不保证此处提供的材料准确、及时或完整,因此不应依赖于此。无论是来自第三方还是其他来源的信息,都不应被视为建议;或者购买或出售的要约;或是购买或出售任何证券、金融产品或工具的征求;或是参与任何特定交易策略。它并未考虑读者的财务状况或投资目标。我们建议此内容的读者寻求自己的建议。未经Pepperstone批准,不得复制或重新分发此信息。