- 中文版

- English

分析

A Traders’ Week Ahead Playbook: Low volatility still offers abundant opportunity

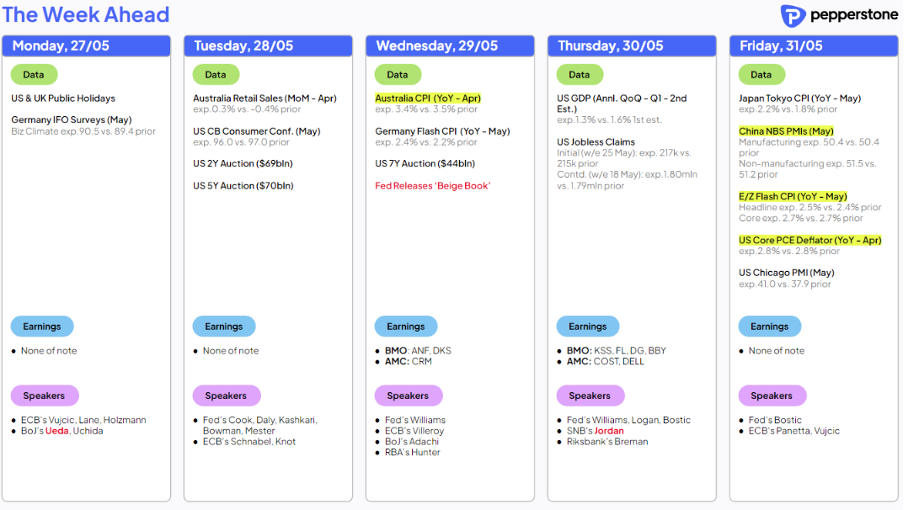

- Key event risks for the week ahead

- Nvidia looking to close higher for a sixth week

- JPY shorts are growing – risks to that trade

- EUR moving in line with reduced ECB rate cut expectations

- US core PCE inflation - A playbook for the USD

- The prospect of weekend gapping risk in crude and the MXN

- Will we see a ‘sell the fact’ play out in ETHUSD?

As the week rolls on traders need to consider if there is the possibility of gapping risk in crude and the Mexican peso (MXN) for the following Monday open, with the OPEC+ meeting pushed out to Sunday, and taking place on the same day as the Mexico election. Staying on the political vibe, the South Africa election takes place on Wednesday, while traders navigate US core PCE inflation, as well as Australia, Japan (Tokyo) and EU CPI reports. We also approach month-end, so price action could be impacted by opaque rebalancing flows.

At a micro level, Nvidia was a major focal point last week and as many have felt first-hand, the wind is firmly to Nvidia’s back, with the stock adding $426b in market cap last week and closing higher for a fifth straight week. Clearly, a solid set of earnings results, but the key factor was that investors heard that demand remains hot, and will continue to outstrip supply and the transition towards its new product range is going smoothly and will lead to a new phase of growth – If Nvidia is going to generate $34 of EPS in 2025 (as is consensus), and market conditions stay favourable, we can easily see this name trading on a 40x PE multiple (currently 36x) and voila, this is a $1300+ stock.

The move in Nvidia can help underpin the NAS100 and keep the index ticking towards 19k – unless that is, we see some hefty profit taking, as there doesn’t seem much out there this week from the macro that can derail this juggernaut. For the tactical traders, the NAS100/US30 ratio (Dow) sits at an all-time high at 0.48x, and I think this can push further higher – as I do Long NAS100 / short US2000, where the ratio could make new highs this week.

(Long NAS100 / short US30 as a ratio)

The set-up in European equity indices is worth putting on the radar too, notably the DAX40 and EUStoxx50. These markets have seen a limited retracement from the mid-May highs and we see consolidation in the price action. That said, from a tactical perspective, there is a lot to like in these markets, so an upside break in the GER40 above 18,760 and momentum may see new all-time highs being tested.

In Asia, we see a positive open to start the week for the HK50, ASX200 and NKY200. We’ve seen good two-way flow in the HK50 of late, but the heat has certainly come out of the April rally, although after 4 days of losses, on Friday we saw signs of stability and indecision from the sellers to push the index through 18,600. The ASX200 holds the former breakout high (from 18 April) at 7723, so the bulls will want to see this level hold, and at least they know where their risk sits.

The NKY225 has been grinding higher since 19 April, with the index working in a bullish channel and printing a series of higher highs and lows. Those positioned on the long side will want a push, and a subsequent hold above 39,240 for a further continuation. Conversely, those positioned short of the NKY225 will want trend support to give way and a move below 38,400 for the downside to open up.

A growing interest to be short JPY – What are the risks?

Perhaps the bigger focal point (over the JPN225) this week is the JPY, given signs the carry trade is growing legs, with traders flocking to fund the trade with short JPY and CHF positions. Notably, NOKJPY has gained for 13 straight days and is on fire. EURJPY has broken out and looks strong above ¥170 and easily could kick further, while USDJPY looks well supported, and while caution is warranted, a kick through ¥157.00 could see USDJPY shorts cover hard.

Worthy of note, and a risk to JPY short positions - through the week we hear comments from BoJ gov Ueda today at 10:05 AEST, while month-end rebalancing flows from pension funds suggest they could be big buyers of JPY. On Friday, we also see Japan (Tokyo) CPI where expectations are for a lift to 2.2% on headline CPI (from 1.8%) with core eyed at 1.9% (1.6%).

Other notable event risks in Asia this week is the China PMI data on Friday (11:30 AEST), with economists expecting an unchanged read in the manufacturing index (at 50.4),while a small improvement in the services PMI index (51.5 vs 51.2 in April) is expected. In Australia, we get Aussie (April) CPI, as well as various partials for the Q1 GDP calculation (due on 6 June). The Aussie monthly CPI read is expected to tick down to 3.4%, but with Australian interest rate futures not pricing any move in the cash rate this year it will take a big surprise to change that pricing.

AUDUSD lacks direction on the higher timeframes, and there are clearer directional trades for me in FX markets – long NOK (vs the crosses), and short CHF (vs the crosses) are front of mind.

EURUSD to stage a move to 1.10?

EURUSD and the EUR FX cross rates get close attention, with EU CPI due on Friday (19:00 AEST), with the market expecting a slight tick up in headline CPI to 2.5%, while core CPI is expected to remain at 2.7%. A June cut (from the ECB) is seen as a done deal, but it is what happens after June that is driving the EUR and interest rate traders have seen enough stabilization in EU growth data to price just one further rate cut this year, to be in line with expected cuts from the Fed. As such, we’ve seen EU bond yields rise by more than US bond yields and this has helped lift EURUSD.

EURUSD vs German 10yr-US 10yr yield spread

On the daily timeframe, technically, EURUSD eyes a breakout of a bull flag formation, where an upside break of 1.0857 would raise the risk of a move into 1.10+. Long EURCHF has been my preferred EUR play, where a move above parity is a real risk this week and the market may run long positions into that CPI data.

US data is focused on core PCE

On the US data front, there are several tier-two releases, including consumer confidence, personal income & spending, and a Q1 GDP revision. The main event though will be core PCE inflation on Friday, with the consensus eyeing core PCE at 0.2% m/m / 2.8% y/y, and headline PCE inflation at 0.3% / 2.7%. A 25bp cut in September is priced at a 50/50 proposition, with a total of 57bp of cuts priced by December - so we’d need a big surprise to change that pricing. US Core PCE above 3% could do the trick, and that would get the USD humming along, while a print below 2.7% could see relief resonate through markets – the USD trades lower, with 2yr Treasuries lower by 5-8bp and gold and the NAS100 & S&P500 likely making new highs into month-end.

As mentioned, do keep an eye on crude for any tweaks to the group's output restrictions, while we sharpen our political game with idiosyncratic risk from the Mexican elections. For the crypto traders we keep an eye on headlines for a formal blessing from the SEC of an ETH spot ETF and crypto traders will be looking to see if we see similar price action as we saw in BTC, and a ‘sell on fact’ play out. As I detail in the article “The Implications of an ETH spot ETF” the risk in ETH remains to the upside and pullbacks are a buying opportunity.

Good luck to all.

Related articles

此处提供的材料并未按照旨在促进投资研究独立性的法律要求进行准备,因此被视为营销沟通。虽然它并不受到在投资研究传播之前进行交易的任何禁令,但我们不会在向客户提供信息之前谋求任何优势。

Pepperstone并不保证此处提供的材料准确、及时或完整,因此不应依赖于此。无论是来自第三方还是其他来源的信息,都不应被视为建议;或者购买或出售的要约;或是购买或出售任何证券、金融产品或工具的征求;或是参与任何特定交易策略。它并未考虑读者的财务状况或投资目标。我们建议此内容的读者寻求自己的建议。未经Pepperstone批准,不得复制或重新分发此信息。