- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

We got the 50bp cut that was slightly favoured at the time in US swaps pricing, and while the larger cut was a catch-up play, where in hindsight the Fed would have preferred to have gone in July, the initial reaction was to sell USDs and buy US Treasuries, gold, and equity risk. In fact, these flows continued right up to the moment that Chair Powell spoke, and for the most part overlooked the fact that the new set of ‘dots’ forecast fewer cuts for both this year, and for 2025 – where US swaps pricing were pricing 150bp of cuts for 2025, and not the 100bp of cuts implied from the Fed’s new set of dots.

The Fed’s new economic projections were largely in line with expectations, although the central projection for the unemployment rate for 2024 and 2025 to hit 4.4% was higher than most had pencilled in. Moving forward, it is this metric that will gain the greatest level of attention, and where the balance of risk is clearly skewed to higher levels than the Fed forecast, and the Fed and the market know this.

The initial moves in broad markets reversed intently from the moment Jay Powell spoke in his presser. Had you told me that we’d get a 50bp cut married with a message of control, and that the Fed were internally celebrating that they’d skilfully managed price pressures and yet felt on track for a soft landing, I would have strongly felt that equity would have feasted on that and gone on a run.

The result in the price action was far from that outcome, and while the confidence expressed may ultimately prove to be a positive for risk in the days ahead, in this small window, the market was impacted by a Fed that is thinking strongly of future cuts in 25bp increments, that is not looking to alter its course on balance sheet runoff, that still sees the labour market as “strong” (which it is) and have limited confidence in its pricing of where the neutral rate is.

In essence, the Fed’s ongoing reaction function is still unclear – they remain on an unscripted path, and where the data – notably revisions to payrolls and the Beige Book – will guide.

The reversal in markets triggered by Powell’s messaging of celebration and confidence was clear-cut. The US 2-year Treasury pushed from 3.53% to 3.61% on the close, and the USD followed in sympathy, with USDJPY rallying from 140.44 to 142.29 (currently). Gold hit the big level of $2600, but subsequently lost a lazy $50 to $2546 before the buyers stepped in. The S&P500, after initially spiking 0.9% into 5690 on the 50bp cut, was treated to an out-and-out chop fest, before settling -0.3% on the day, with tech, staples and utilities attracting the selling flow.

With the flows abating, and increased liquidity returning to the top of the order book, the market can start to think ahead with a more orderly and calmer mindset and as such we get a more realistic visual of how the market really aggregates the Fed’s current thinking. Chair Powell would be pleased with how the broad market digested the totality of the statement and presser, but when we step back, we consider that this is a Fed feeling in control, where a soft-landing is still very much their base case, and while the bias of easing is in increments of 25bp and getting to wherever neutral is will be a slower journey than many expected, this is a Fed that will not hesitate to cut in 50bp clips on any sign of higher unemployment and layoffs.

The US swaps market already sees the risk of 50bp cuts, and currently price 32bp of cuts for the November FOMC meeting and 68bp for December. We have two NFP prints to digest and guide before the November meeting, and we may even be forced to start reviewing the Fed’s Beige book- and, we have the small affair that is the US election. However, all the signs are that we could once again go into the November FOMC meeting with the market debating a 25bp vs 50bp cut.

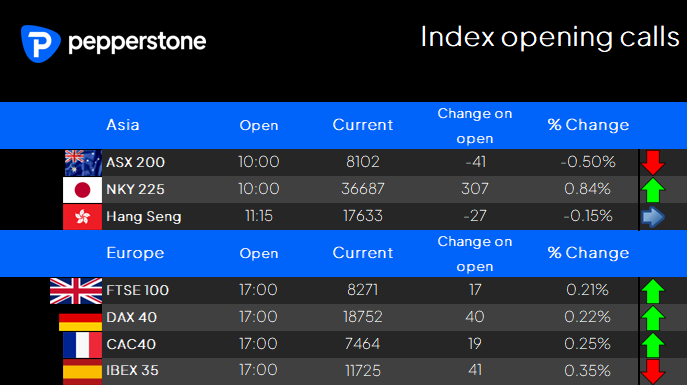

Looking ahead to the Asian equity open, we see that our calls for the respective index open are mixed, with the ASX200 eyed to open on a heavy tone, while we see the NKY225 outperforming and where the HK50 should unwind on a flat note. It will be fascinating to see how Asia trades as we take in and react to all that was heard from the Fed, but I’m not sure much has changed – we’re all data dependent and sentiment hasn’t really shifted because of what we’ve heard. The ‘Fed put’ is as strong as ever and the bank will react intently to any further fragility.

By way of event risk to navigate today, we see NZ 2Q GDP, Aussie employment data, the BoE meeting, and US weekly jobless claims.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.