- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

US Dollar Breakout: Safe Haven Flows, Rising Yields and America’s Energy Edge Drive USD Buying

Summary

• The US dollar has outperformed all G10 currencies amid rising geopolitical tensions

• Initial safe haven flows favored the Swiss franc before rotating back into USD

• Higher oil prices have reduced expectations for Federal Reserve rate cuts

• US Treasury yields have risen, boosting the dollar’s yield advantage

• The US energy export position strengthens its macro resilience

• Surging European natural gas prices could pressure the euro further

A Shift in G10 FX Dynamics

We have seen significant developments across G10 currency markets, particularly in the direction of the US dollar.

When FX markets reopened on Monday, traders initially reduced exposure to the US dollar, preferring the Swiss franc as the primary safe haven. Some investors considered the Japanese yen, but with oil prices rising sharply and Japan heavily dependent on energy imports, there was less appetite to hold yen given the negative economic implications of higher oil prices.

As the session progressed, the focus shifted toward petrocurrencies such as the Norwegian krone and Canadian dollar. However, by the start of European trade, the dynamic changed again.

The US Dollar Index (USDX) lifted from 97.80 and trended steadily higher toward 98.75, where it has since consolidated in choppy trade. On the day, the US dollar outperformed all G10 peers, surprising many participants. Technically, the Dollar Index has broken above the 98 range highs and closed above its 50-day, 100-day and 200-day moving averages. The question now is whether momentum can extend toward 100, especially with EURUSD trading below the 19 Feb lows of 1.1742 and closing under 1.1700.

The dollar has also seen solid gains against the SEK and the CHF, with USDCHF, which traded lower through the Asian session, rallied sharply back toward 0.7800.

Why the Rethink on the US Dollar?

There are several drivers behind the renewed strength in the greenback.

1. The Safe Haven Debate One school of thought suggests the US dollar has reasserted itself as a safe haven currency amid heightened geopolitical uncertainty. Traders appear less willing to hold the yen or Swiss franc compared with previous episodes of risk aversion. While this remains open to debate, it has clearly supported dollar flows.

2. Rising Oil Prices and Fed Expectations Higher oil prices have altered interest rate expectations. Markets have priced out 11 basis points of implied Federal Reserve rate cuts over the next 12 months. As a result, US Treasury yields have risen sharply, driven by the repricing of rates, but also higher inflation expectations.

Importantly, the relative increase in US yields compared with other G10 bond markets has been more pronounced, reinforcing the dollar’s yield advantage.

Higher yields and reduced rate cut expectations create a powerful tailwind for the USD.

The US Energy Advantage

A critical and often underappreciated factor is the United States’ role as a global energy powerhouse.

• The US produces around 13 million barrels of crude oil per day

• Approximately 65 percent of crude production is used domestically

• The US is the world’s largest LNG exporter

• Around 80 to 85 percent of total US energy production is consumed domestically

This domestic energy resilience makes the US less vulnerable to supply shocks than energy-importing nations such as Japan or many European countries. With key refineries and terminals temporarily halted in Saudi Arabia, Qatar and Israel, and with the Strait of Hormuz constrained, transport and insurance costs have surged.

Shipping rates charged for crude and LNG transportation effectively doubled overnight, taking the YTD increase for chartering large vessels (in this case to China) to $439k a day - in some cases insurers will not insure vessels on certain routes. Higher transport costs may render imports uneconomical for some buyers. As a result, Asian and European energy consumers could increasingly turn to US supply to meet demand. This dynamic positions the US as a relative beneficiary of constrained Gulf logistics.

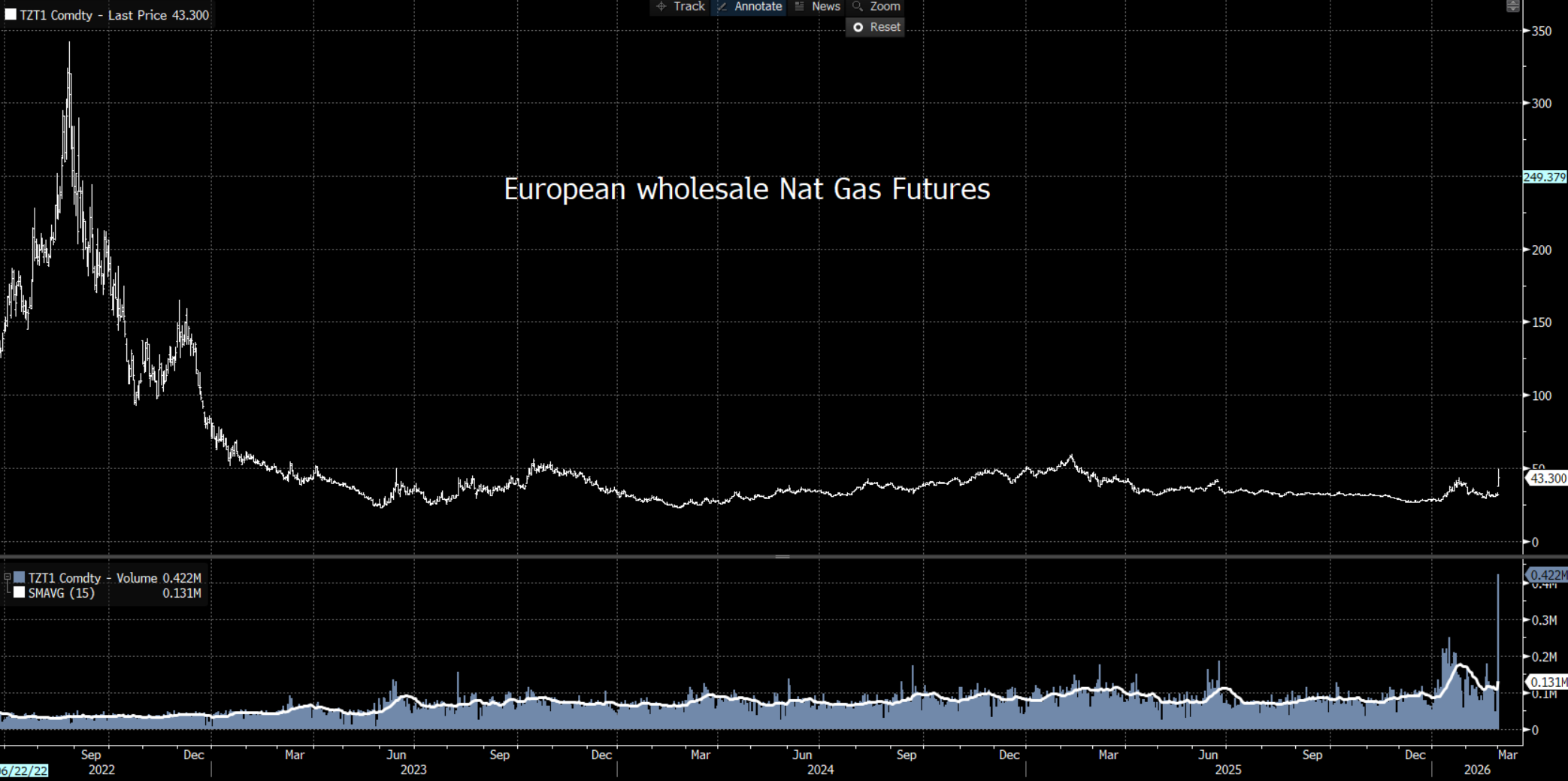

European Gas Prices and the Euro Risk

Another key development is the 39% surge in European natural gas prices. Granted, at 43 (€ / MWh) the levels are still well below what we saw in 2022, and we know this market can be highly volatile, but should this kick higher then it could see the (inverse) relationship with the EUR build.

If European gas prices continue to rise, the euro could face renewed structural pressure. The correlation between natural gas prices and EURUSD is therefore critical to monitor in the sessions ahead.

Can the Dollar Index (USDX) Push to 100?

With the Dollar Index breaking key technical resistance levels, attention now turns to whether momentum can extend toward 100. Further short covering in the US dollar could fuel additional gains. However, sustainability will depend on:

• The persistence of elevated oil prices

• Continued upward pressure on US Treasury yields • Ongoing constraints in Gulf transport routes

• Developments in European natural gas markets

If logistical bottlenecks around Hormuz remain severe and additional regional energy facilities face curtailment, the US stands to benefit as a key alternative supplier.

In that environment, the US dollar may remain firm as both a yield play and a structural energy beneficiary. For now, the combination of rising yields, shifting safe haven dynamics and America’s energy dominance provides a compelling explanation for USD strength.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.