- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

The price action suggests staying cautious at this stage, and for any sustainable bull trending conditions, my thesis is that I want to see:

- An inflation scare – this is where we flock to gold as a hedge. At this juncture, my simplistic ‘inflation shock’ model suggests the markets sees inflation, but absolutely no fear of a future inflation shock.

- Disinflation/deflation shock – this sends both nominal and real bond yields lower; a factor which means yield-less assets become a quasi ‘store of value.’

- The increased use of the Fed’s balance sheet - we hear an appetite that the Fed are prepared to cap the long end of the US bond curve and it’s on for gold.

My own view is until the expected return on gold improves (as per the conditions above) and we see a far lower correlation to equities (the 30-day rolling correlation with the S&P500 is -0.35), then gold will fail to find any real trend and the opportunity cost of holding gold reduces the investment case. So, ideally, I want one of these three conditions to be met before I turn tactically bullish.

As always, I have an open mind on gold. And while I acknowledge the level of sentiment has become bearish, perhaps to the point of extremes, I don’t see any of these three variables being met anytime soon. That includes the debate about the Fed capping long-end Treasuries, which is the subject of huge debate, but where I still see as a low probability.

Subsequently, I can’t get excited about a lasting bullish trend in gold, at this stage, but I do see rising scope of a tactical trading rally to emerge.

The Fed will be more concerned with short-term interest rates than long-end bonds

All the focus last week was on the bond market, but we can’t go past the moves in global interest rate and swaps markets – this must be on the radar. The wash-up is that on Friday the market was pricing a rate hike for next year in Australia, New Zealand, Canada, and the US, and almost a full hike in Switzerland and the UK too. Rates traders may hear guidance from the likes of the Fed and RBA that rates are on hold until 2024, but they’re not buying it. The market is front running a change in forward guidance, and this is one consideration reducing the appeal of gold.

With the ECB due to report its bond-buying figures today, the RBA meeting tomorrow and a raft of Fed speakers due this week, the risk is central banks fight back and throw some doubt in rates traders’ minds that the earlier hike schedule is mispriced. This may calm the move in rates, and even long-end bonds and may put a better bid in gold.

Certainly, tomorrow's RBA meeting will be significant given the market is front running a belief that they will be compelled to end yield curve control (YCC) early. While the RBA’s daily bond purchases are at the highest level since they started QE, I think they’ll hit home that they have control here, despite on current trajectory they’re on schedule to own over 50% of the short to medium duration bonds. This could be a very interesting meeting.

Gold traders always need to have an eye on real Treasury yields. However, I think they’ll be sensitive to moves in US interest rates market too – consider we see Eurodollar rates market pricing 76bp or three hikes (if we assume 25bp increments) between the March 2021 to September 2023 period. This is significant as this represents the Fed’s forward guidance on rates. As we see in the chart below, the market disagrees and sees a real risk they raise sooner.

A rising interest rate regime, without an inflation overshoot is not a great stomping ground for gold.

Yield spread between Eurodollar Sept 2023 minus March 2021

So, there's a mismatch between the Fed’s guidance on rates and market pricing, and this is where volatility arises. It's not often the market front-running a central bank pivot, but when they see a scenario and refuse to listen to the narrative it can be devastating – so this is a huge week for the Fed. Jay Powell’s speech on 5 March (04:0 AEDT) is going to be huge.

So, what does this mean for gold? Well, a cohesive push back on the market’s pricing on rate expectations could be good for gold, but we then ask will the market buy the narrative.

Naturally, moves in the USD will affect the gold price, but this is the beauty of being able to trade gold in AUD, EUR, CHF, GBP, and JPY. Tactually, we buy gold in the weakest currency and take shorts in the strongest and maximize the profits. Trade Spot Gold CFDs with spreads from as low as 0.05 points.

Sentiment is shot

Options risk reversals - I always pull this chart out as it’s a great measure of sentiment – here we see 1-week and 1-month risk reversals (RR). In effect, RR take call option implied volatility (for 1-week and 1-month options) and subtract put implied volatility. So, when we see this at a negative number it shows put vol wears a premium to calls. As we see from the lower pane, the current put premium is at extremes – could this offer a bullish contrarian signal?

(Upper – 1-week RR, lower - 1-monbth RR)

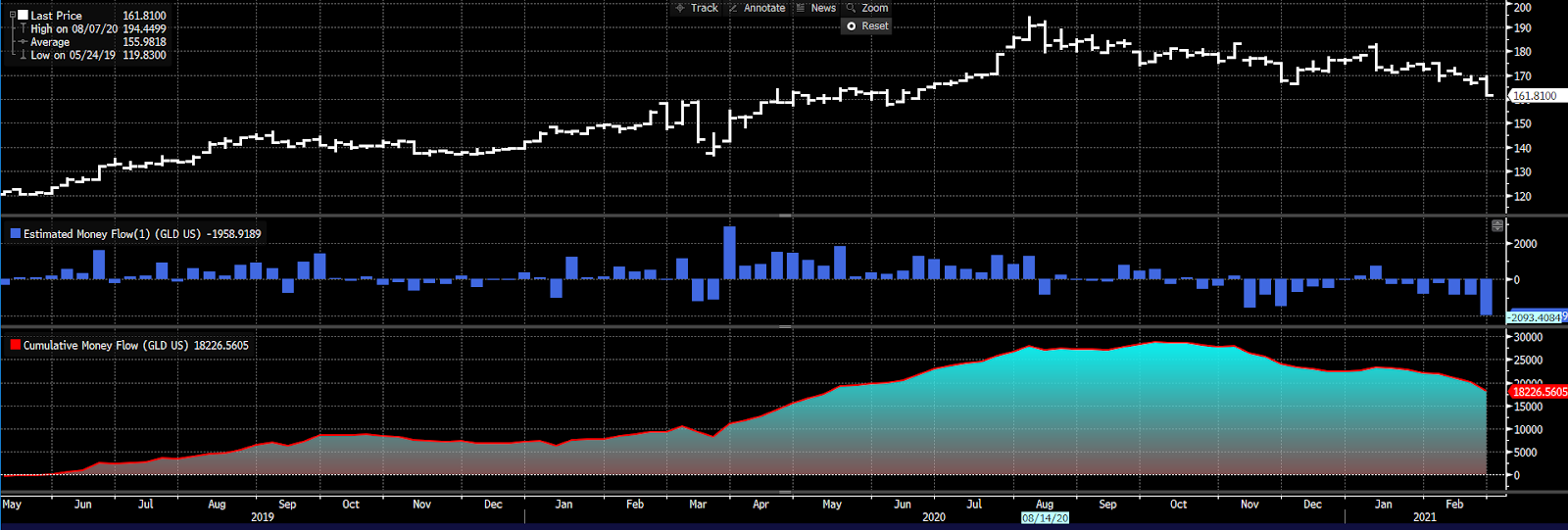

We’ve also seen seven consecutive weeks of outflows from the GLD ETF, where we saw $1.6b of outflows last week alone. A lagging indicator perhaps, but it marries well with other extreme sentiment gauges.

The trade

We can look at any indicator or relationship with other markets, but the best real-time flow aggregator is always price. Everything I see is that the yellow metal is oversold, and that sentiment is shot to pieces. I also see a rising risk that central banks exert themselves on the rates market this week, but until price changes direction, then I would be looking elsewhere for trades.

That said, the 1700/1705 area interests (pink circled area) and I’ll see how price reacts should it get there – however, when it comes to gold, I am a buyer of strength and not before.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.