- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

Breaking down the markets

USDCNH remains central to the positive USD bias, and despite the best efforts of the PBoC to push back on the yuan weakness, the daily chart is a thing of beauty – perhaps the better way to think about price is to question how high USDCNH would be if the PBoC hadn’t been ‘fixing’ the yuan at stronger levels each day, and Chinese state banks weren’t selling USDs.

With the China proxies in the doghouse, we see NZD and AUD finding few friends, although we may see a few lightening up on shorts into the RBNZ meeting. I stay biased long EURAUD, although understand sentiment towards China is shot to pieces -this week's high-frequency China data may only need a small beat to cause a strong upside reaction in China proxies.

USDJPY eyes a retest of the 145.07 highs and the manner by which US Treasuries are trading, both on a nominal and real basis, it's hard to fade the upside in USDJPY, although we may run into JPY intervention headlines this coming week.

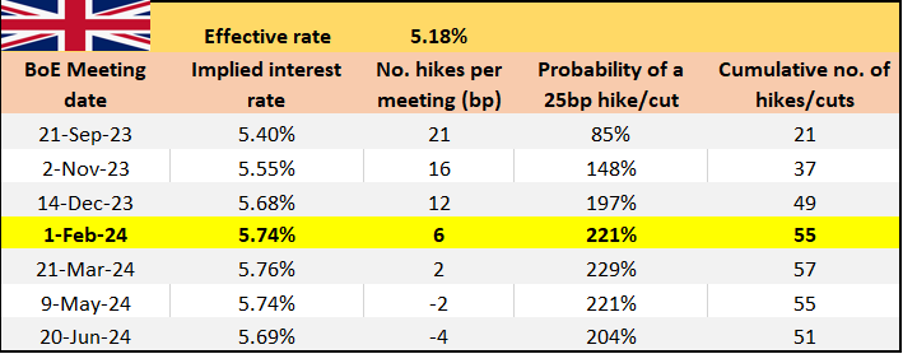

With a focus on bond markets, it's hard to go past moves in the UK bond market, where the 10yr gilt is above 4.5% and eyeing recent highs of 4.71%. We see 2- and 5-year UK gilt yields moving higher vs US Treasuries, and this is offering some support to the GBP. We continue to watch this dynamic with UK wages and CPI due this week.

The preference remains to cast the net towards the crosses, where GBPAUD, GBPNZD or GBPJPY have been solid plays and will need to big downside UK core CPI print to halt the bullish trends.

With China joining the UK as a central focus this week, we see big underperformance in the HK50, CHINAH, and CN50. With China's new yuan loans printing a 14-year low last week and renewed concerns on property developers, the Chinese authorities need to get in front of economics and sentiment. The market wants bold action, and anything less will attract sellers. I like the CHINAH index into 6200, but realise sentiment is shot and we also have Tencent reporting this week.

US500 DAILY – eyes on the 50-day MA

Elsewhere, given views on US real rates, the USD as well as the general flow, I stay negative on gold and silver, but see modest upside risks in energy. We watch price action in broad large-cap tech and the A.I plays where we’re seeing dicey moves and real vulnerability emerge, and this could be a big theme that has to be on all trader's radars. The mega-cap tech/AI trade is one crowded position that if even modestly unwound could have big ramifications for risk. The 50-day MA on the US500 (4448) needs to hold this week, and a close below this average may hold big implications for market structure.

While monthly options expiry could be price action, we watch to see if we see a move higher in volatility and our trading environment.

The Risk Manager; navigating the marquee data/central bank meetings

China high-frequency economic data (all due 15 Aug 12:00 AEST) – After the recent weak trade and credit data, and a big push higher in USDCNH, we watch the monthly high-frequency economic data. Here, the market looks for industrial production to grow at 4.3% YoY, retail sales at 4.2% YoY and fixed asset investment at 3.8% YoY. The market is craving stimulus on both a fiscal level, backed by new monetary policy easing. Will bad economic data result in upside for Chinese equities, as it accelerates the need for stimulus? I am not so sure, but the cleaner trade remains USDCNH upside, where weakness in the yuan should in turn weigh on the AUD.

Australia Q2 Wage Price Index (15 Aug 11:30 AEST) – the market looks for wages to grow at 0.9% QoQ, and 3.7% YoY (unchanged from Q1) – unless we get a YoY WPI print above 4% YoY, the data shouldn’t alter Aussie rates pricing to intently where the market prices 15bp (or a 59% chance) of hikes by December.

UK employment and weekly earnings (ex-bonus) report (15 Aug 16:00 AEST) – the market expects wages to push to 7.4% (from 7.3%), with the UK unemployment rate eyed at 4%. The GBP was a relative outperformer last week in G10 FX, notably vs JPY and NZD – so GBP longs will look for big wage print this week, which would confirm expectations of a 25bp hike from the BoE on 21 September and lift peak rate expectations towards 6%.

US retail sales (15 Aug 22:30 AEST) - the market looks for sales to grow 0.4% with the ‘control group’, the basket of sales that feeds more directly into the Q3 GDP calculation, eyed at 0.5%.

Canada CPI inflation (15 Aug 22:30 AEST) – the market prices 5bp of hikes for the next BoC meeting (6 Sep), so the CPI report could alter that pricing resulting in increased CAD volatility. Here, the market sees headline CPI coming in at 3% YoY (from 2.8%) or 0.3% MoM. Core CPI is eyed at 3.7% (3.9 yoy). It may take a 4-handle on core CPI to see the September meeting as a ‘live’ event.

China new home prices (16 Aug 11:30) – with the Chinese property market in focus, as well as property developers and if we are to see a credit event, new home sales could get the headlines and move Chinese assets.

RBNZ meeting (16 Aug 12:00 AEST) – the market is firmly of the view that RBNZ keep rates unchanged at 5.5%, and we see only 6bp of hikes priced for the remainder of 2023. It seems unlikely the NZD will move too intently on the RBNZ statement and may revert quickly to following moves in the yuan and China equity markets.

UK July CPI (16 Aug 16:00 AEST) – coming after last week’s hotter UK Q2 GDP print, and Tuesday’s UK labour report, the market expects headlines inflation to drop to 6.8% YoY (from 7.9%). However, core CPI is likely to remain frustrating sticky also at 6.8% (from 6.9%). Unless core inflation falls markedly, then a 25bp hike in Sept is all but assured.

UK interest rate pricing per BoE meeting

- July FOMC meeting minutes (17 Aug 04:00 AEST) – the Fed have moved to a firm data-dependent approach, so the minutes may not offer any surprising insights. The market is waiting for new data, where they can potentially revisit low expectations of a hike in the November FOMC meeting, which is currently priced at a 33% chance.

- Australia July employment report (17 Aug 11:30 AEST) – the usual monthly labour market lottery – the consensus is we see 15k net jobs being added, with the unemployment rate eyed at 3.6% - again, it’s hard to see the data altering rate expectations too intently and unless we get a big beat/miss shouldn’t see any lasting move in the AUD. On the day, I would be fading extreme moves intraday through buy/sell limit orders in AUD.

- Norges central bank meeting (17 Aug 18:00 AEST) – The Norwegian central bank should almost certainly hike by 25bp to 4%. The NOK takes its cues from energy markets, although the 20-day rolling correlation between Brent crude and the NOK is not overly impressive at 56%. The NOK was the weakest G10 currency last week, so unless we get a great surprise from the Norges Bank, we should see the NOK revert to watching crude, Nat Gas, and being a high beta risk proxy.

- Japan July CPI (18 Aug 09:30 AEST) – with the market establishing JPY shorts as the preferred funding currency for carry exposures, we question if the JP national CPI print really matters given the JPY’s lack of cyclical qualities. We shall see, but the market looks for headline CPI at 3.3% and core at 4.3% (4.2%). With USDJPY eyeing a retest of the 30 June highs of 145.07, and the trade-weighted JPY breaking to new lows, the market may be looking out more intently for JPY intervention headlines.

Stocks to watch; earnings front of mind:

- HK – Tencent (report on 16 Aug) – with a market cap of HK$3.21t, Tencent has easily the biggest weight and influence on the HK50. The implied move for earnings is 2.7%, so it could get lively.

- US – we get the retail names due this week with Home Depot (15 Aug), Target (16 Aug), and Walmart (17 Aug) offering insights into consumer trends.

- Australia – 52 ASX200 companies report numbers this week – including, JBH (14 Aug), CSL (15 Aug), COH (15 Aug)

Related articles

_(6).jpg?height=420)

_(3).jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.