- English

Trading the Week Ahead: Oil, USD Strength and Rising Drawdown Risk in the S&P 500

We turned the page on what was a huge week in financial markets, and we now look ahead to a week packed with scheduled and unscheduled event risk. Last week clearly marked a further shift toward capital preservation and a flight to safety across certain parts of financial markets, with higher short-term inflation expectations, a strong repricing in G7 rates markets, and private credit concerns hitting sentiment.

Oil continues to dictate the tone and drive increased correlations across macro markets. After the low print of $81.16 seen on Tuesday, Brent crude futures pushed steadily higher through the week and closed near the highs of that run.

As energy prices moved higher, its correlation with risk assets rose sharply, and also within single stock names too. S&P 1-month implied individual stock correlations have risen to 35%, the highest level since May 2025. This is not yet at a major extreme but rising single-stock equity correlation signals increasing risk aversion, where equities move together rather than trade on individual fundamentals. When correlations rise, particularly when paired with the VIX rising above 30%, would suggest the major equity benchmarks may be vulnerable to deeper drawdowns.

Equity technicals & internals breaking down

The weekly chart of S&P 500 futures shows that over the past three weeks traders have increasingly been selling rallies rather than buying dips. Some buying remains in the market, although this has been concentrated in energy, ultra-predictable cash flow sectors, and traditional safe-haven industries.

Market breadth is also weakening, with four of the seven MAG7 stocks now trading below their 200-day moving average, which is often seen as a negative omen for future index performance. Currently, 51% of S&P 500 constituents remain above their 200-day moving average, but that figure is trending lower.

Private credit is also emerging as a background concern. This is placing pressure on financial stocks, particularly after JPMorgan announced it was marking down loans tied to private credit funds following a review of credit quality. European financials have also come under pressure, falling roughly 15% from their highs. At the same time, US high-yield credit spreads widened by 18 basis points last week, signalling a modest deterioration in risk appetite within credit markets.

King Dollar making a move

In currencies, the US dollar has emerged as the clear front-runner and a preferred positioning in this market environment. The US dollar index (DXY) has broken above 100 and the defined range highs that had held since August. Notable gains in the dollar were seen against the Swedish krona, South African rand, and New Zealand dollar. Implied volatility in FX markets has risen, although the increase has been modest compared with the surge in volatility seen in short-term interest rate markets. The repricing of rate cuts and the broader interest rate outlook has been particularly aggressive, which in turn has helped support the US dollar.

The US eyeing measures to change control in the Strait of Hormuz

Reports this morning suggest the Trump administration is considering announcing a coalition of forces to escort ships through the Strait of Hormuz. This idea is receiving significant attention as markets gear up for the new week, although there remains uncertainty around if and when such a major move might occur. The proposal feeds directly into the market’s escalation versus de-escalation narrative, which continues to drive cross-asset volatility and price action. A show of clear military force could carry significant operational risks and challenges, and if executed poorly it could exacerbate tensions rather than calm them. There is also no guarantee that such a move would immediately restore normal shipping flows through the strait. As a result, markets will watch developments closely, although the timing and structure of any action remain unclear.

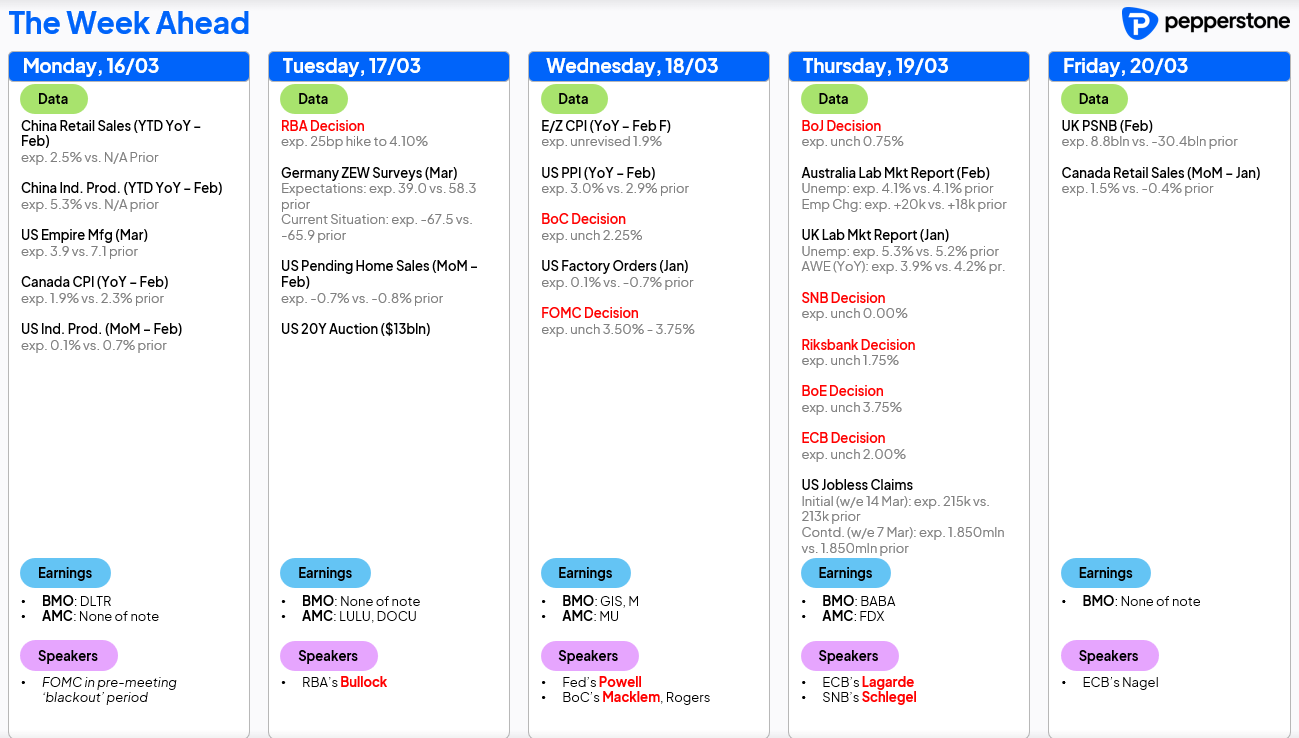

A huge week of central bank meetings

Central banks will dominate the macro calendar this week. The Federal Reserve meeting on Wednesday will attract the greatest attention. Markets will focus heavily on the Fed’s rhetoric around energy prices and how rising oil costs could influence short- and longer-term inflation expectations. Higher energy prices will likely push headline inflation higher in the March CPI and PCE data, potentially creating a wide divergence between headline and core inflation.

Traders will also scrutinise the revised dot plot projections to determine whether the median projection signals no rate cuts this year or maintains expectations for one cut.

The Reserve Bank of Australia meeting tomorrow is also seen as highly live. Markets currently price a 64% probability of a rate hike at this meeting. However, that outcome is far from guaranteed, and the decision remains finely balanced. As a result, volatility in the Australian dollar around the announcement could be elevated.

Elsewhere, the European Central Bank, Bank of England, Bank of Japan, and the Riksbank are not expected to move on rates. However, their guidance and policy statements could still introduce short-term volatility in their respective currencies.

Beyond central banks, the technology sector will also be in focus. NVIDIA’s GTC conference begins today, where leaders across the AI ecosystem will discuss the latest developments, trends, product releases, and the pipeline ahead. Historically, this event has been a catalyst for volatility and positive returns across many AI-linked stocks, so the sector could again become a focal point for trading activity.

China will also release a series of high-frequency economic data this week, which may influence sentiment around global growth and commodity demand.

Last week’s dominant trades were clear: selling banks, selling rallies in equity indices, being long the US dollar, long volatility, and long crude oil. The key question for markets now is whether that positioning remains intact through the event-heavy week ahead.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.