Liquidité Profonde

Liquidité - une considération importante pour le trading

Peut-être la considération la plus importante, quel que soit le type de compte, est la liquidité des conditions au prix d'achat ou de vente affiché. La liquidité est la facilité avec laquelle un trader peut entrer et sortir d'une position au prix indiqué et sans avoir à descendre dans le carnet d'ordres pour obtenir un remplissage au prochain meilleur prix.

Obtenir un prix pire parce que le volume offert par un teneur de marché ou un fournisseur de liquidité pour effectuer la transaction au prix indiqué fait défaut est appelé 'slippage' et aboutira à ce que le trader paie un spread plus large.

Cela se produit beaucoup plus fréquemment que beaucoup ne le croiraient, surtout par de plus petits courtiers fonctionnant selon un modèle de zéro spread. Où les traders cherchant à remplir 0,1 d'un lot ou plus peuvent voir leur remplissage réel sur la transaction totalement différent du prix indiqué sur la plateforme.

Dans la plupart des cas, un trader ne conciliera pas la différence, mais ce slippage s'accumulera comme un coût sur le portefeuille, surtout pour les traders effectuant des transactions de taille, ce qui témoigne d'un manque de transparence dans la tarification et peut nuire à la confiance qu'un client a envers son courtier.

Un exemple de la différence chez Pepperstone

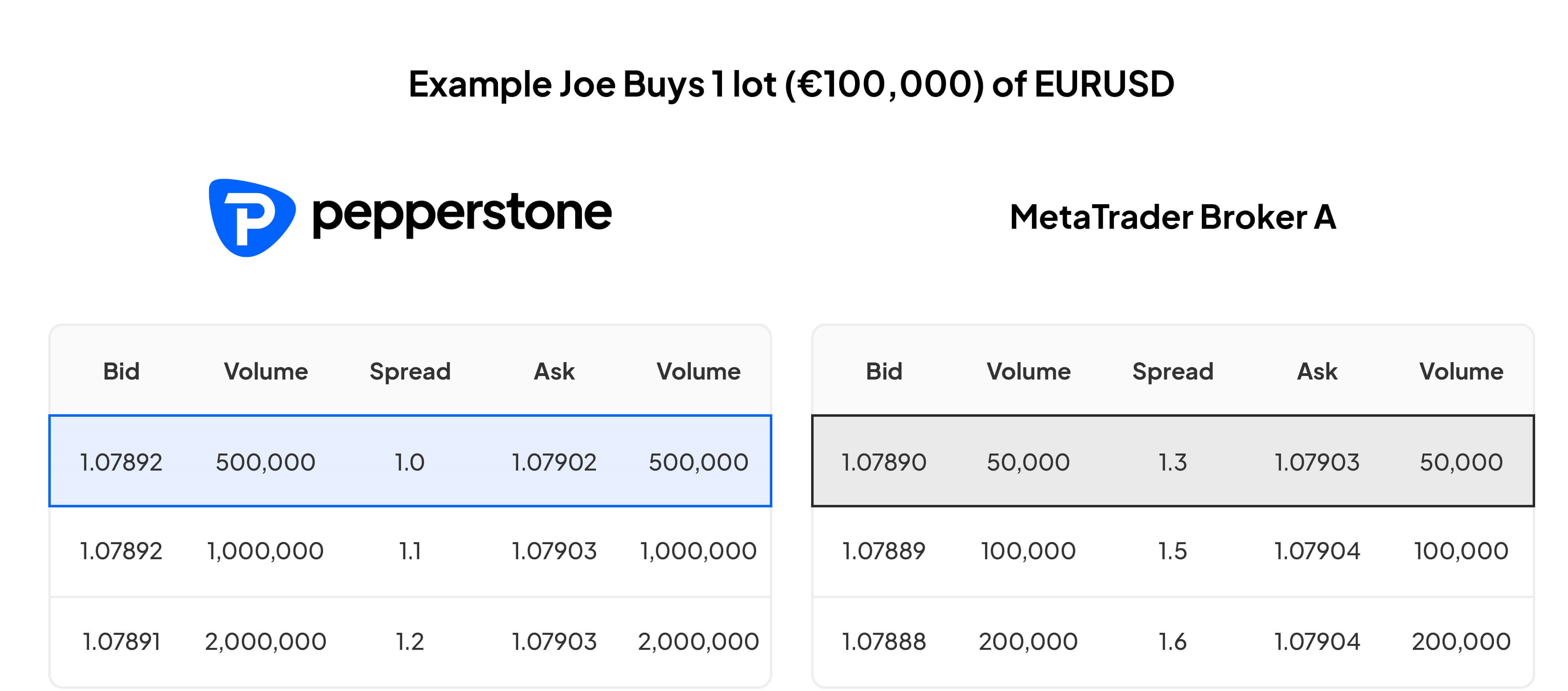

Disons que Joe veut acheter 1 lot (100 000 EUR) d'EURUSD. Avec Pepperstone, l'ordre de Joe est exécuté au prix indiqué de 1,07902. Mais avec Broker A, l'ordre est rempli au prix moyen pondéré par le volume (VWAP) de 1,07904, ce qui diffère du prix indiqué. Cela est dû au fait que Broker A a une liquidité faible, offrant seulement 50 000 au sommet du spread du carnet d'ordres. Comme Joe a acheté 1 lot (100 000 EUR), la partie restante de la transaction (50 000) passe à la deuxième couche de l'offre du carnet d'ordres offrant un volume de 100 000, et c'est le spread appliqué au volume de 50 000 échangé.

Avec Pepperstone, l'ordre d'1 lot est exécuté au prix indiqué de 1,07902. Cependant, avec Broker A, le volume n'est pas là pour faciliter la demande d'1 lot, donc l'ordre est rempli au prix moyen pondéré par le volume (VWAP) de 1,07904 au lieu du prix indiqué.

Cela peut sembler être une petite différence, mais cela met en évidence que le prix auquel Joe pensait avoir effectué la transaction et le remplissage de la transaction réel peuvent être différents compte tenu de la dynamique de liquidité.

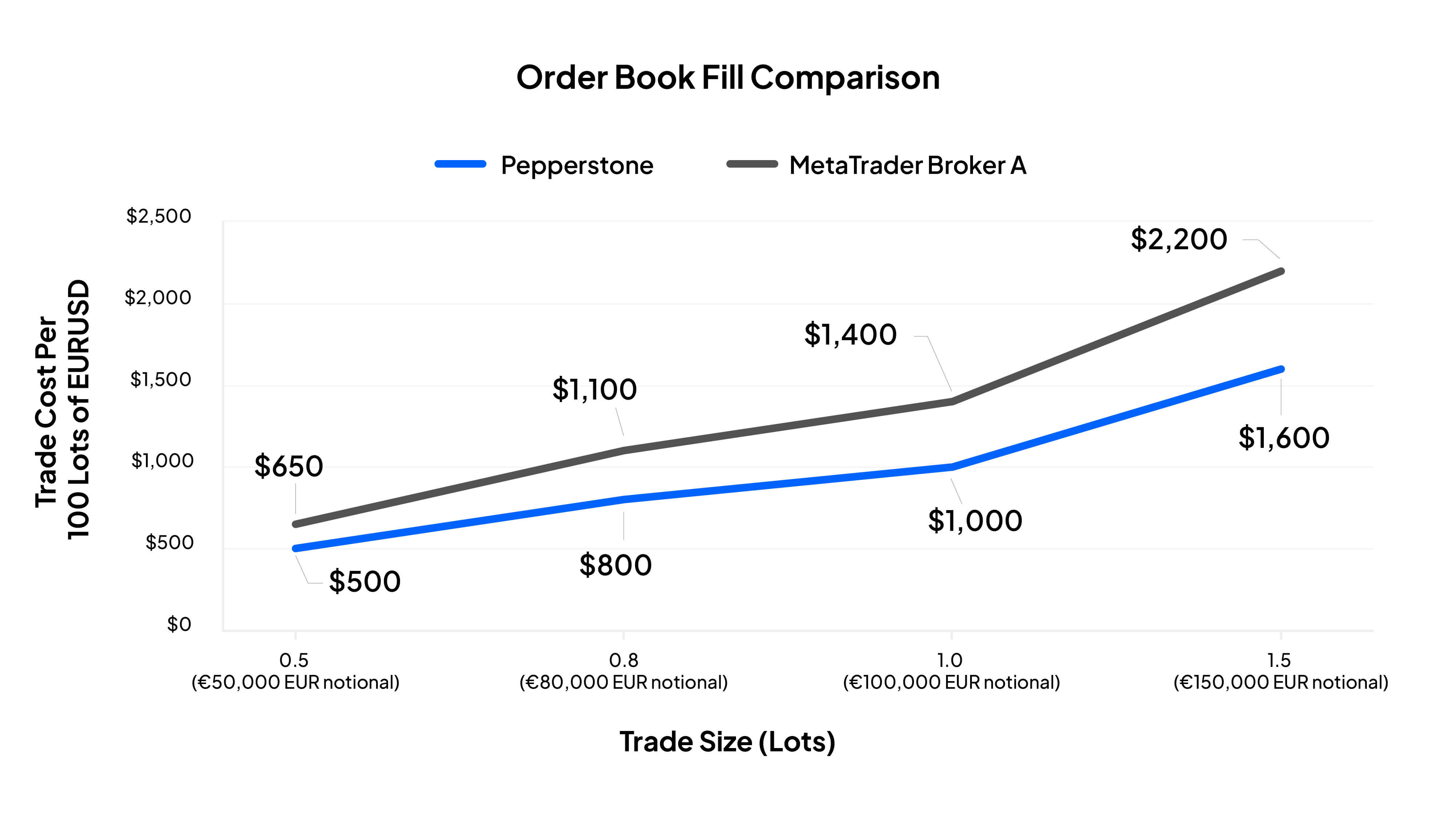

Considérez comment ce scénario se déroule sur 100 transactions. Alors que le prix et le spread bid-off fluctueront (de cet exemple), et la liquidité variera d'une transaction à l'autre, nous pouvons voir comment cela se joue dans le temps si nous extrapolons les paramètres de cet exemple.

Pepperstone offre une liquidité profonde au prix indiqué, ce qui est connu comme une liquidité en haut du carnet d'ordres. En général, si un trader souhaite effectuer une transaction de plus grande taille, il aura beaucoup plus de chances d'ouvrir et de fermer une transaction au prix qui lui a été indiqué, que de nombreux autres courtiers.