- Español

- English

- 简体中文

- 繁体中文

- Tiếng Việt

- ไทย

- Português

- لغة عربية

- Español

- English

- 简体中文

- 繁体中文

- Tiếng Việt

- ไทย

- Português

- لغة عربية

Analisis

We look back at the big themes that have driven cross-asset volatility and the conditions through which we’ve all had to adapt our trading –these include persistently high inflation, a worrying spike in the cost of living and aggressive rate hikes – yet resilient growth. We can also look at more regional-focused issues – a UK gilt tantrum driven by the Truss govt’s unfunded mini-budget, the invasion of Ukraine, the MOF/BoJ intervening to buy JPY and China’s Covid Zero policy.

The culmination of these factors created huge cross-asset volatility, decade-long market regime changes and lasting trending conditions.

Looking into 2023

Markets live in the future, and we look forward to the key themes that could cause volatility throughout 2023 – what’s important is not just to fully note these macro factors, but to understand the trigger points that offer a higher conviction of when to express the themes – taking this further, knowing the markets/instruments and strategies to express the theme is obviously advantageous.

These themes could alter market volatility, range expansion and market structure - so regardless of whether you’re purely automated or discretionary, it can pay to be aware.

While there are many more, these are five potential themes that I am looking at closely for 2023 that if triggered would affect the markets we trade.

1 - High inflation worries morph into growth concerns and a higher probability of a recession

US and global inflation in decline

- Market pricing (i.e. the inflation ‘fixings’ market) of future inflation shows US CPI inflation expected to fall to around 3% by year-end

- US M2 money supply has fallen from 26% to 1.3% - US headline CPI typically lags by 16 months

- Manufacturing PMI delivery-lead times and supply chain data suggest inflation falls hard in 2023

- Unit labour costs falling to 2.1%

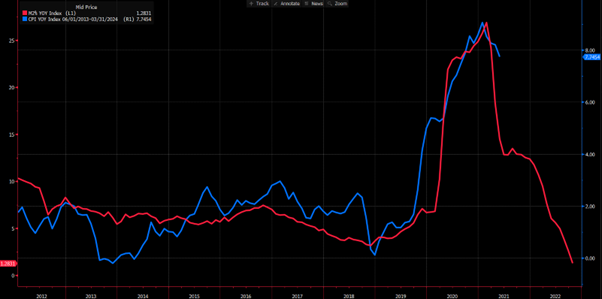

US CPI (blue) vs M2 money supply leading by 16 months

Growth – while the consensus from economists is that the US economy narrowly avoids a recession, and EPS expectations have not been revised down to reflect recessionary conditions - the markets see a higher probability of this outcome – I back the markets, where we see:

- All parts of the US yield curve are inverted – US 2s vs 10s are the most inverted since 1981

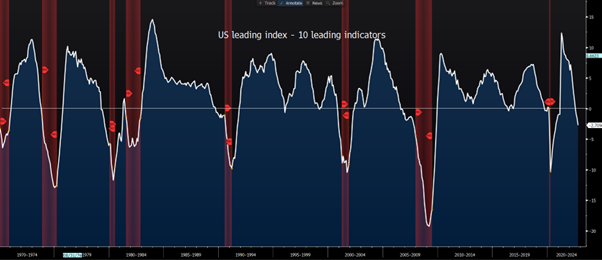

- The US leading index (measures 10 key economic indicators) has turned negative and falling fast – this has an exemplary record of predicting US recessions

- Comments from the CEOs of Goldman Sachs and BoA warning of tougher times ahead

US leading index – red areas represent a US recession

Themes to trade as we price in a recession

- Consensus EPS expectations are cut by around 20% (from the highs), in turn, lifting PE multiples – traders will assess the trade-off between earnings downgrades vs a lower discount rate

- Steeper yield curves are a trigger – while now is not the time to put on curve steepeners, when short-dated US Treasury bond yields do fall/outperform, we’ll see a steeper yield curve – this could be the trigger for a sharp equity rally, led by financials

- As the US data deteriorates, we will likely see equity market drawdown, US treasury buying and selling of risk FX - it’s when central bankers acknowledge that growth is a greater concern the market will feel validated in its pricing of rate cuts – it’s here we see a risk rebound, broad USD selling and housing + lumber outperforming

- As bond yields fall, we should see solid outperformance from the JPY and CHF and EM assets

- USD initially works selectively vs global FX, but then reverses as conviction of the Fed cutting impacts and traders look ahead to a trough in the global growth slowdown

- Gold and silver rally hard as a hedge vs recession risk

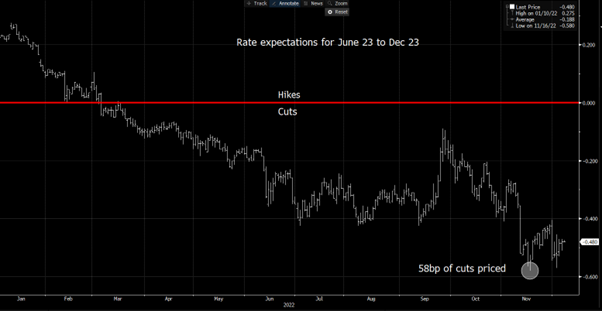

2 - Central bank policy – assessing the potential for rate cuts

Rates pricing from June 23 to Dec 23

3 - China reopening and China's market outperformance

We’ve already seen a plethora of measures announced and Chinese markets have rallied hard – China is the elephant in the room when it comes to the global growth outlook for 2023 – a weak 1H23 seems likely but this will then followed by far stronger growth in 2H23 – after a poor 2022, Chinese assets could really outperform in 2023

- Long HK50 / short NAS100 could be a trade to look at if markets de-risk on a higher probability of a US recession

4 - BoJ policy recalibration – time for the JPY to fly

BoJ chief Kuroda steps down in April but there are already plans for a review of BoJ policy – it feels inevitable that we’ll see a 25bp lift to the BoJ’s YCC target to 50bp – we’ve already seen signs that Japanese banks/pension funds are moving capital back to Japan to get a more compelling return in the JGB market – but could a major policy change cause tremors in global bond markets and promote significant inflows into the JPY?

5 - Politics & Geopolitics – great for volatility, bad for humanity

Obviously one of the most important issues in 2022, not just for markets but humanity - always a hard one for traders to price risk around

Related articles

Pepperstone no representa que el material proporcionado aquí sea exacto, actual o completo y por lo tanto no debe ser considerado como tal. La información aquí proporcionada, ya sea por un tercero o no, no debe interpretarse como una recomendación, una oferta de compra o venta, la solicitud de una oferta de compra o venta de cualquier valor, producto o instrumento financiero o la recomendación de participar en una estrategia de trading en particular. Recomendamos que todos los lectores de este contenido se informen de forma independiente. La reproducción o redistribución de esta información no está permitida sin la aprobación de Pepperstone.