- Español

- English

- 简体中文

- 繁体中文

- Tiếng Việt

- ไทย

- Português

- لغة عربية

- Español

- English

- 简体中文

- 繁体中文

- Tiếng Việt

- ไทย

- Português

- لغة عربية

Analisis

One can assume that the BoJ are also one step closer to moving away from Yield Curve Control (YCC), and logically one could argue that the BoJ would like to be able to lift rates and remove YCC concurrently.

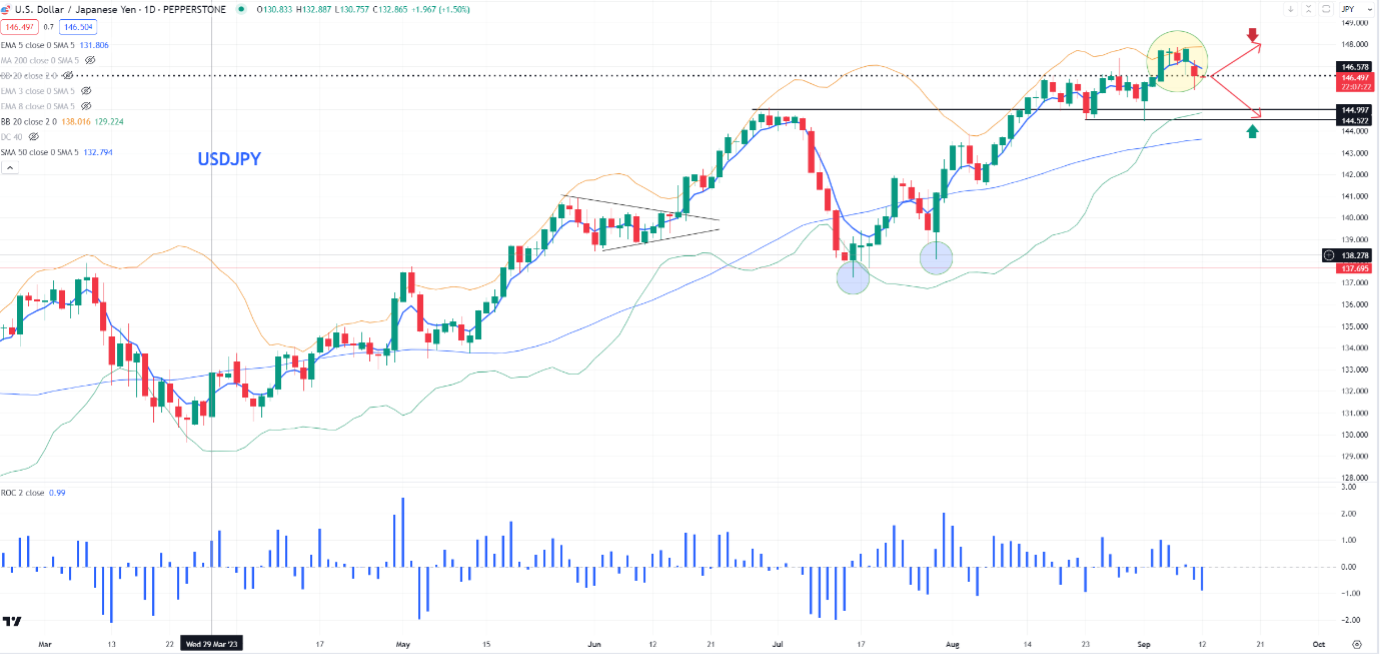

The result of Gov Ueda’s comments was an intense move higher in Japanese swaps and govt bond yields (Japan govt 5yr bonds closed +6bp at 28bp). The move in yields compelled the BoJ to intervene and limit the selling. USDJPY reacted, trading into 145.90 but has found buyers below the figure, and at the time of writing oscillates around the former breakout highs of 146.56.

Our client skew is fairly nuanced and while net long JPY, remains unconvinced on a more pronounced downside move, with 59% of open positions in USDJPY held short. This fits well with reported JPY positioning held by fast-money leveraged institutional funds.

While Ueda’s interview is certainly constructive for JPY longs, I refrain from getting too excited at this stage by what we’ve heard, where the actions are more of a medium-term issue. Wages are the core consideration for the BoJ, but we won’t get the outcome of the spring wage negotiations until April 2024, with November a potential date when we could see early estimates coming through. So realistically, the big catalyst won’t be seen for a while, and any changes in rate setting won’t happen for about six months, although the market lives in the future and will front-run these expectations.

USDJPY daily chart

The case for FX funds to support USDJPY pullbacks

Near-term levels of statistical and implied volatility are still very low, and equity markets are supported, which continues to support a JPY-funded carry trade. The market is debating if the Fed hike in November and we navigate the US CPI print (Wed 22:30 AEST), which could influence expectations of another Fed hike and impact the USD. One could also argue that a further move higher in JGB yields isn’t going to cause a significant repatriation and reweighting from Japanese pension/insurance funds into Japanese bonds, given that 10-year JGBs (Japan govt bonds) already hold a 212bp (basis point) premium over US 10yr Treasurys on a currency-hedged basis.

Trading USDJPY – Play the range

With that in mind, tactically, I feel it most probable that traders will look to trade a range in the near-term, selling rallies above 148, while supporting and buying into pullbacks at the range lows of 144.50. Supporting this, USDJPY 1-week implied volatility trades at 9.07%, which equates to a 152-pip move (up or down) over the week. One can re-assess this view if US CPI is a significant blowout/miss to consensus, but for now, playing a range seems the most likely path.

Related articles

_(1).jpg?height=420)

Pepperstone no representa que el material proporcionado aquí sea exacto, actual o completo y por lo tanto no debe ser considerado como tal. La información aquí proporcionada, ya sea por un tercero o no, no debe interpretarse como una recomendación, una oferta de compra o venta, la solicitud de una oferta de compra o venta de cualquier valor, producto o instrumento financiero o la recomendación de participar en una estrategia de trading en particular. Recomendamos que todos los lectores de este contenido se informen de forma independiente. La reproducción o redistribución de esta información no está permitida sin la aprobación de Pepperstone.