- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

September 2025 US CPI: Rate Cuts Remain On The Cards

Price Pressures Persist

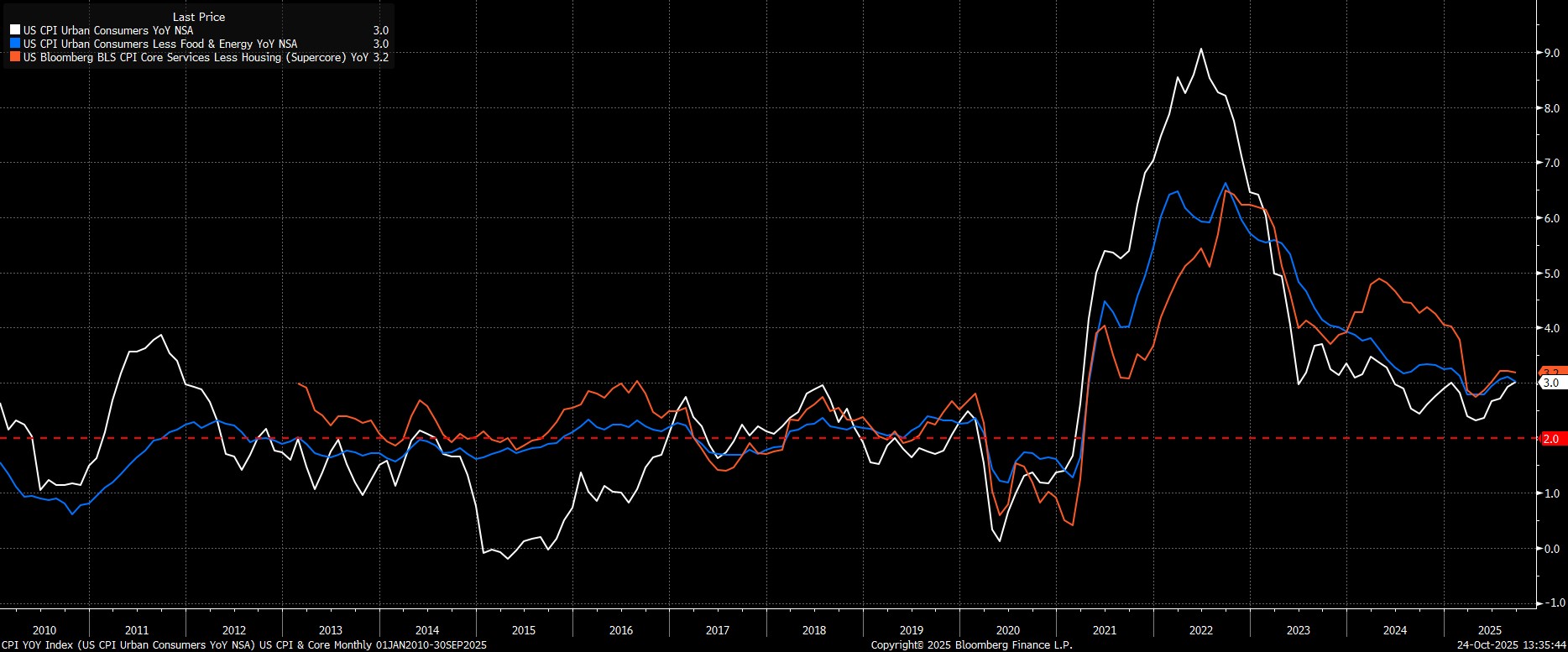

Headline CPI rose 3.0% YoY last month, cooler than consensus expectations for a 3.1% YoY increase, though inflation still touched the 3% mark for the first time since last June. Measures of underlying price pressures, however, pointed to some degree of moderation in price pressures, as core CPI rose 3.0% YoY, and the ‘supercore’ index (aka core services less housing) rose 3.2% YoY, unchanged from August.

Meanwhile, on an MoM basis, both headline and core CPI printed softer than expected, at 0.3% MoM and 0.2% MoM respectively, in what was also a surprise dip from a month prior.

As usual, annualising these figures helps to provide a clearer idea of the underlying inflationary trend:

- 3-month annualised CPI: 3.6% (prior 3.5%)

- 6-month annualised CPI: 3.0% (prior 2.3%)

- 3-month annualised core CPI: 3.6 % (prior 3.6%)

- 6-month annualised core CPI: 3.0 % (prior 2.7%)

Tariff Pass-Through Continues

As well as the above, the composition of the price pressures that continue to bubble away remains key, not least taking into account that the vast majority of upside inflation risk continues to stem from the Trump Administration’s tariff policies. While the FOMC are viewing these tariffs as a ‘one-time shift’ in the price level, the degree to which tariffs are being fully passed on in the form of higher consumer prices remains unclear.

In any case, core goods prices rose 1.5% YoY in September, unchanged from the pace seen in August, and perhaps suggesting that we may well be past the peak in terms of tariffs being passed through. Core services prices also sent an optimistic message, rising 3.5% YoY, a cycle low, and implying a lesser risk of inflation persistence.

Limited Fed Policy Implications

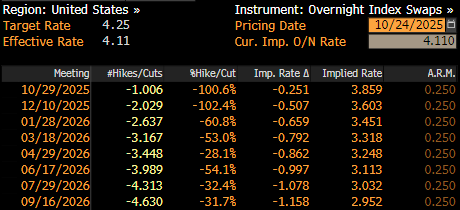

Despite inflation continuing to move away from the FOMC’s 2% target, the September CPI report did little to alter the market’s view of the near-term policy outlook, with the USD OIS curve continuing to fully discount a 25bp cut both next week, and in December.

Looking Ahead

Taking a step back, and as noted, it seems highly unlikely that today’s data will materially move the needle in terms of the FOMC outlook. Not only do policymakers remain prepared to look-through any tariff-induced price pressures for the time being, but most have also been very clear indeed that the reaction function now hinges primarily on the employment side of the dual mandate, with an easier policy stance necessary in an attempt to prop up a stalling US labour market.

Consequently, my base case remains that 25bp cuts will be delivered at both the October, and December meetings, with such a pace of easing likely to continue into the early part of next year as well, with policymakers continuing to adopt a ‘run it hot’ stance that in turn tilts risks to the US economy, and US assets, to the upside.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.