- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

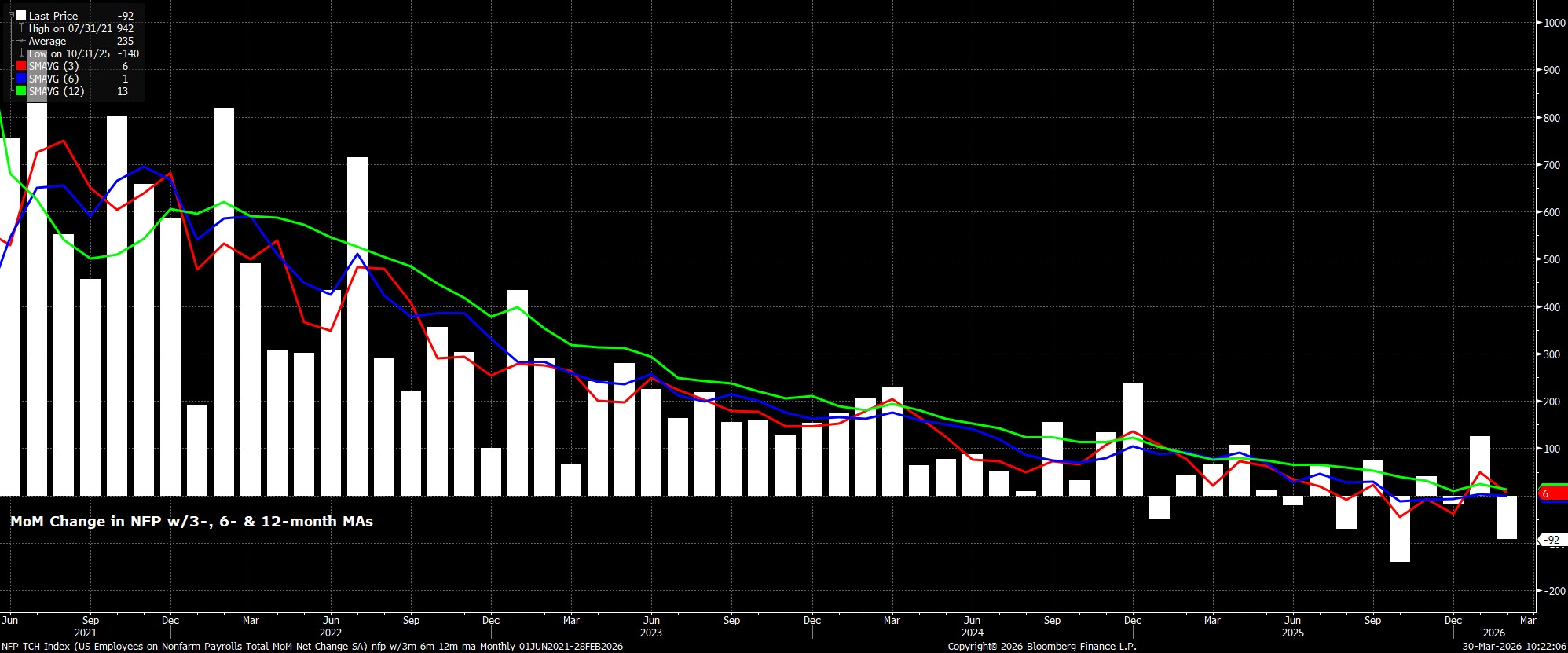

Headline Payrolls To Rebound

Headline nonfarm payrolls are set to have risen by +60k last month, roughly in line with the breakeven pace of job growth, and a notable rebound from the -92k February print.

As ever, though, the range of estimates for the payrolls print remains wide, from +15k to +125k at the time of writing, while there are still lingering concerns that the headline print is overstating actual job creation, potentially by as much as 60k, per Fed estimates.

Factors Driving The Rebound

By and large, the likely drivers of a rebound in jobs growth in March is set to be a reversal of those factors which dragged payrolls surprisingly lower in February. These include significantly warmer weather in the survey week this time around, which should result in the addition of approx. 30k lost jobs in weather-sensitive sectors such as construction, while the end of strikes in the healthcare sector should add another 30k or so.

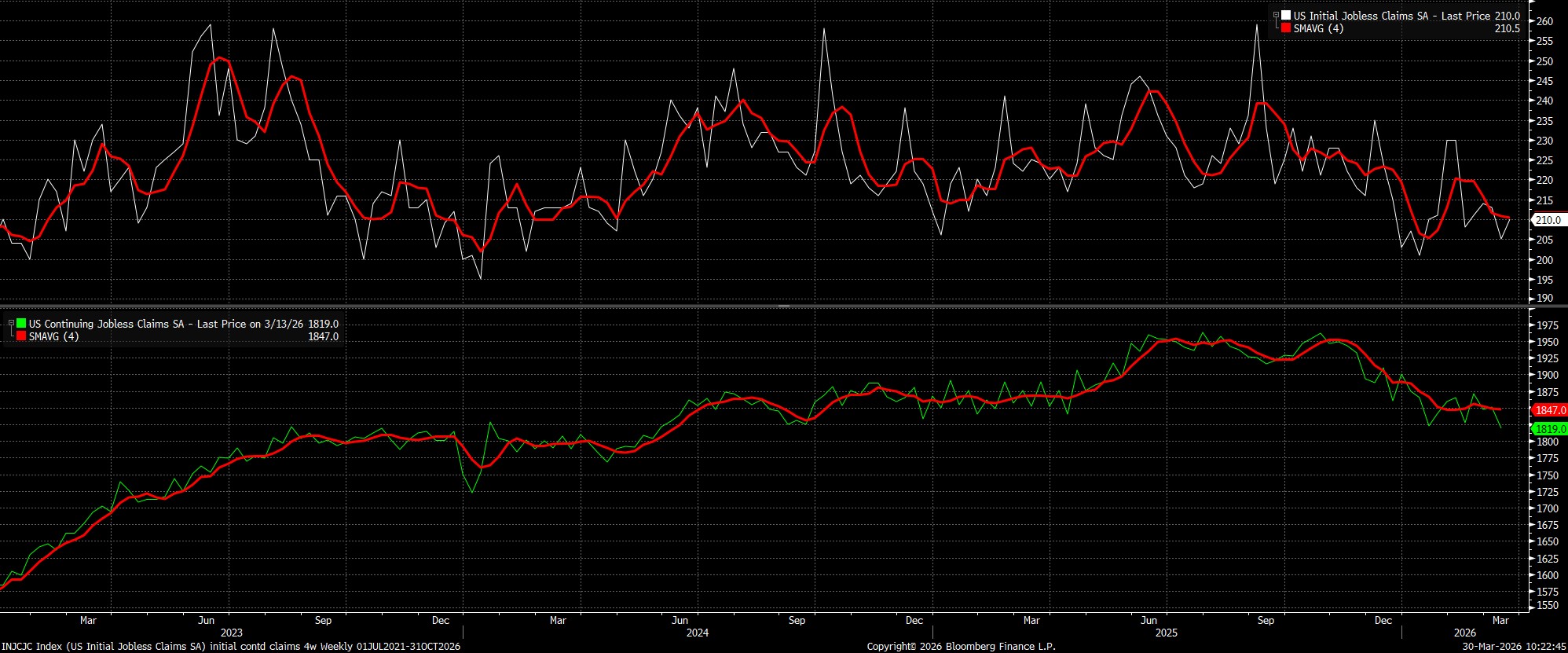

More broadly, the survey week for the March payrolls print likely came much too early to gauge any impact of ongoing conflict in the Middle East, or the subsequent surge in energy prices. That said, both initial and continuing jobless claims have been steady in recent weeks, implying that there has not yet been a material detrimental labour market impact from recent events.

Leading Indicators Also Point To A Rebound

On the subject of other labour market data, leading indicators for the March payrolls print also suggest that a rebound could be on the cards.

As noted, both initial and continuing claims have held steady in recent weeks, while the weekly ADP report pointed to a job gain of roughly 40k, albeit in the week prior to the BLS survey. Elsewhere, at the time of writing, neither of the ISM surveys has yet been released, though the ‘flash’ S&P Global PMI pointed to employment having fallen for the first time since February 2025, even if the drop in question was relatively modest. Lastly, the NFIB hiring intentions survey points to a further pick-up in jobs growth, using the usual 3-month lead vs. NFP, though it’s plausible that at least some of those hiring plans may have been put on ice given ongoing uncertainty.

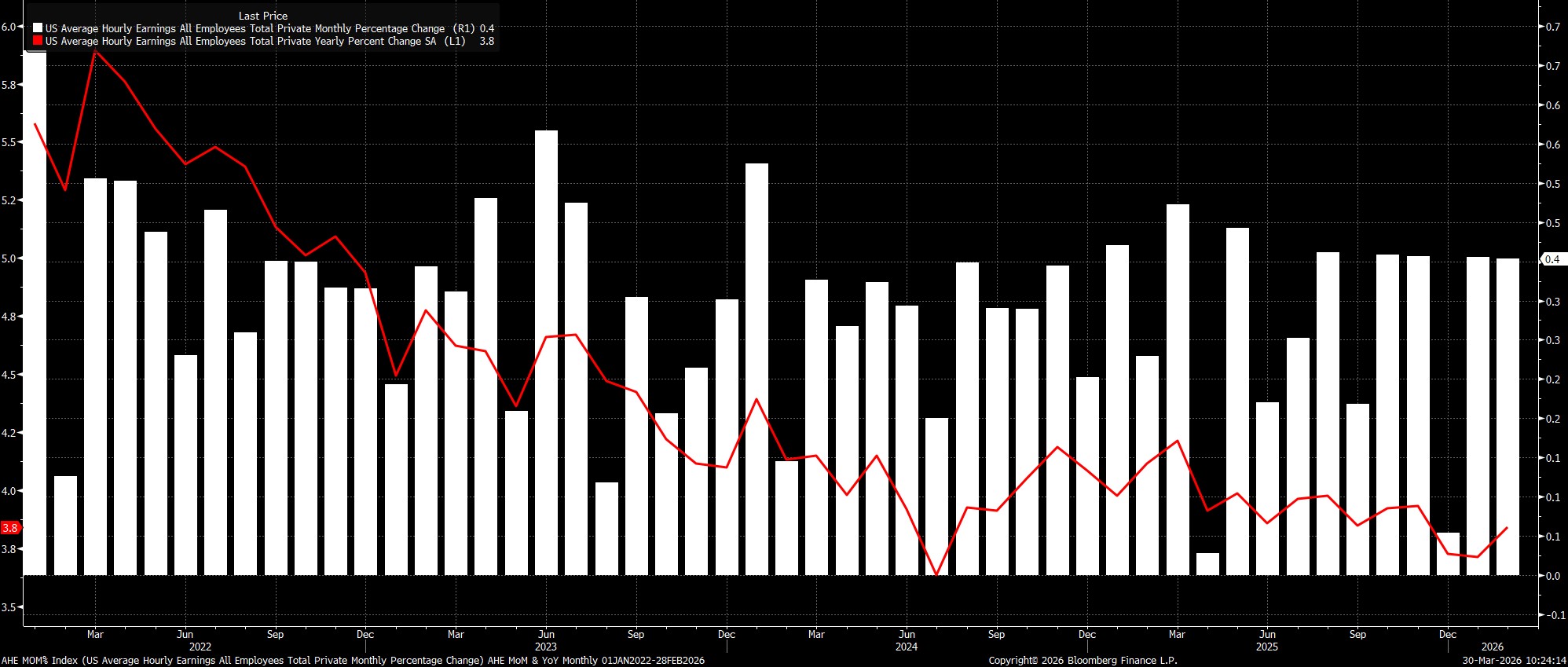

Earnings Pressures To Remain Subdued

Remaining with the establishment survey, the report should again show that earnings pressures remain relatively contained, with average hourly earnings set to have risen by 0.3% MoM/3.7% YoY, both of those rates being 0.1pp slower than that seen in February.

This would suggest that earnings growth continues to run at roughly target-consistent levels, and that there is little risk of sustained inflationary pressure emanating from the labour market. While this is important when considering the likelihood, or otherwise, of second-round effects materialising from the energy price shock, it still won’t prevent a substantial rise in spot inflation over coming months, as higher commodity prices make their way through the economy.

Household Survey Poses Risks

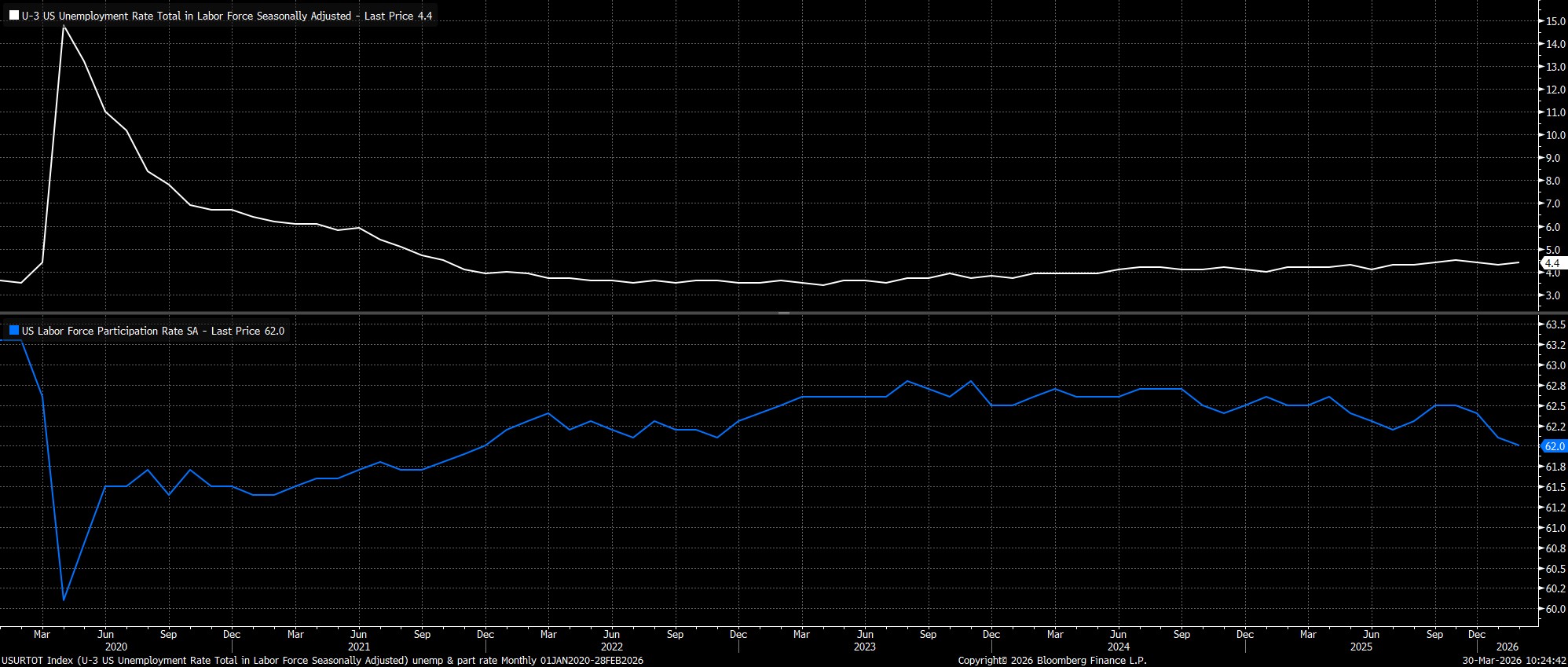

Turning to the household survey, headline unemployment is set to have held steady at 4.4% last month, though as always extrapolating from stable jobless claims into the U-3 rate is far from an exact science.

In fact, risks to that consensus estimate tilt to the downside, in a couple of ways. Firstly, on an unrounded basis, U-3 printed 4.441% in February, leaving a very low bar indeed for the headline figure to round up to a cycle high 4.5%. Secondly, labour force participation is set to have ticked higher, to 62.1%, which could also drive an increase in headline unemployment, assuming that those new entrants to the labour force were unable to immediately find work.

A Note Of Caution On Markets

For financial markets, some degree of caution is likely to be needed surrounding the labour market report, given the timing of the release.

Unusually, the BLS have scheduled the jobs data for Good Friday, when not only the vast majority of markets will be closed, but public holidays across the western world mean that many market participants shan’t be at their desks. Consequently, volumes are likely to be considerably lighter than typically seen on ‘Jobs Day’, while liquidity is also likely to be much thinner than usual. Altogether, this suggests the potential for a choppy market reaction to the data, and potentially an outsized reaction in the event of a significant deviation from consensus.

Limited Fed Policy Implications

Zooming out, the March jobs report is unlikely to materially shift the near-term Fed policy outlook, with the FOMC having shifted firmly to a ‘wait and see’ approach at the March confab, in light of the increasingly uncertain economic outlook, as well as the near-term upside inflation, and downside growth risks posed by ongoing conflict.

That said, a weak jobs report, following a sub-par February print, would doubtless spur further concern over the potential for a ‘stagflationary’ backdrop to develop, where each of the dual mandate objectives may begin to come into conflict. In such a scenario, it seems plausible that the Fed would focus on ensuring that inflation expectations remain well-anchored, at the cost of further labour market slack developing.

Still, on the assumption that the rise in energy prices does indeed prove to be solely a temporary ‘hump’ in price pressures, further easing is likely to remain on the cards as the year progresses, and after Chair designate Warsh has taken the helm, with the ‘no hire, no fire’ labour market being one that could still use further help from a less restrictive monetary stance.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.