- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

Markets Reprice Economic Fallout as Crude Spikes and Risk Appetite Weakens

Summary

• Markets have shifted focus from headlines to the economic fallout of the conflict

• Crude oil surge is driving higher inflation expectations and growth concerns

• Bonds and gold rally together, signalling defensive positioning and the risk to growth

• Equity markets weaken, with poor breadth and rising volatility hedging • March and April data will be critical in confirming economic impact

• Geopolitical risks intensify, with rising probability of US involvement and Houthi disruption

• Traders remain defensive, selling rallies and maintaining volatility hedges

Markets Shift Focus to Economic Fallout As diplomatic efforts build, with world leaders and mediators pushing for alignment and unity, the conflict is simultaneously escalating. Financial markets are making it clear where their focus lies, and it is firmly on the latter.

Friday’s session marked a shift in market thinking. The well-established cross-asset relationships began to break down, as traders moved beyond reacting to headlines and started pricing the economic consequences of the conflict. Higher short-term inflation expectations, volatility in rate markets, and concerns around supply shortages and inventory are now front and centre. Oil Surge Drives Inflation and Growth Concerns Crude futures surged to new cycle highs at 114.57, up 8.2% on the day, with prices reopening a further 3% higher. At the same time, US one- and two-year inflation swaps moved higher, reflecting rising price pressures.

Yet despite this inflation impulse, US Treasury bonds rallied, yields fell, and gold attracted renewed buying interest. This shift in the market’s reaction function is telling. It signals a growing focus on downside growth risks and the broader economic fallout from sustained higher energy prices, particularly the ability for businesses to source and afford energy inputs.

Bond Flows and Positioning Turn Defensive

Flows into US two-year Treasuries, alongside activity in interest rate futures and swaps, reinforce this shift. Positioning has turned more defensive, with traders better to buy and options flows skewed towards calls, signalling expectations for lower yields. If bonds continue to rally, options-related flows could amplify the move, with dealers needing to buy the underlying to rebalance delta. This dynamic highlights a market increasingly positioned for downside risk.

Equity Markets Show Signs of Stress

Equity markets reflect this deterioration in sentiment. The VIX closed at 31.1%, with a clear skew towards downside hedging. The technical backdrop in the S&P 500 has weakened materially.

The break of 6,500 in S&P 500 futures was significant, with both cash and futures markets closing near their lows. Market breadth has deteriorated sharply, with just 20% of stocks trading above their 50-day moving average. Five of the Magnificent Seven now sit below their 200-day moving averages, leaving the broader market vulnerable and lacking organic buyers.

US Dollar Holds Safe Haven Status

In FX markets, the US dollar remains the relative safe haven within G10. Attention now turns to whether the dollar index can break above 100.50.

Earlier in the conflict, dollar strength was driven by rising Treasury yields. That relationship may now evolve, with the dollar increasingly trading as a pure safe haven and relative growth proxy.

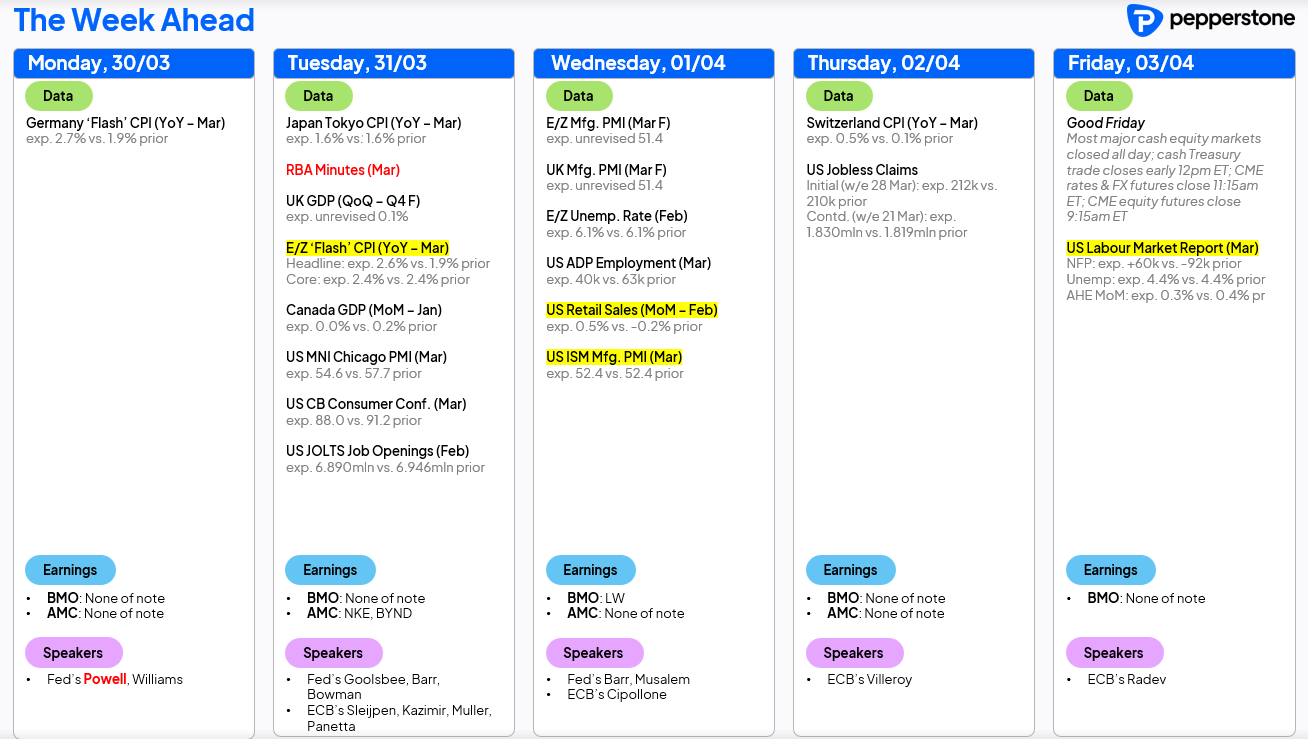

Data Focus Shifts to the March and April Series

Attention now turns to incoming economic data, although markets will be highly selective. February data is likely to be viewed as stale, as it predates the surge in energy prices and inflation expectations.

The focus shifts to data capturing March conditions and beyond. US ISM manufacturing, particularly the prices paid component, will be key. European inflation is expected to rise from 1.9% to 2.6%, while US payrolls will again command attention.

Markets are far more sensitive to downside surprises, especially if unemployment trends towards 4.5% or higher. US JOLTS and weekly jobless claims will also play an important role in shaping the narrative.

Geopolitical Risks Intensify

Geopolitics remains the dominant driver. Weekend developments have increased expectations of US involvement, with prediction markets pricing a 44% probability of US forces entering Iran by 31 March, rising to 70% by April.

The involvement of the Houthis adds a new layer of complexity. While partially priced on Friday, confirmation came after market close, leading to crude futures rising 3.8% on reopen, while S&P 500 futures fell 0.5%.

The key risk lies in potential disruption to shipping through the Bab al-Mandab Strait, which accounts for roughly 12% of global trade. Any disruption, combined with higher insurance costs, could drive another leg higher in crude and further weigh on risk assets.

This also has implications for regional players, particularly Saudi Arabia, where early signals suggest a shift from a cautious stance towards more direct support for a US-led coalition.

Market Uncertainty Remains Elevated

What stands out is how quickly probabilities have shifted. Only weeks ago, US boots on the ground in Iran was viewed as a low-probability outcome. That has clearly changed, reinforcing the need for markets to remain open-minded. The key risk now is that the March, and importantly the April economic data begins to reflect the economic impact of the conflict. This will likely be reinforced by CEO commentary during the upcoming US earnings season.

Trading Playbook: Defensive Positioning

In this environment, traders remain defensive. The prevailing strategy is to sell rallies in risk assets and maintain volatility hedges. The key shift has been higher crude prices, which have brought bonds back into favour as a defensive asset, while gold could rally despite a stronger US dollar.

Outlook: News Flow Will Drive Markets

The week ahead will be driven by news flow. It remains heavy, fast-moving, and highly influential on price action.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.