- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

Inflation Jumps

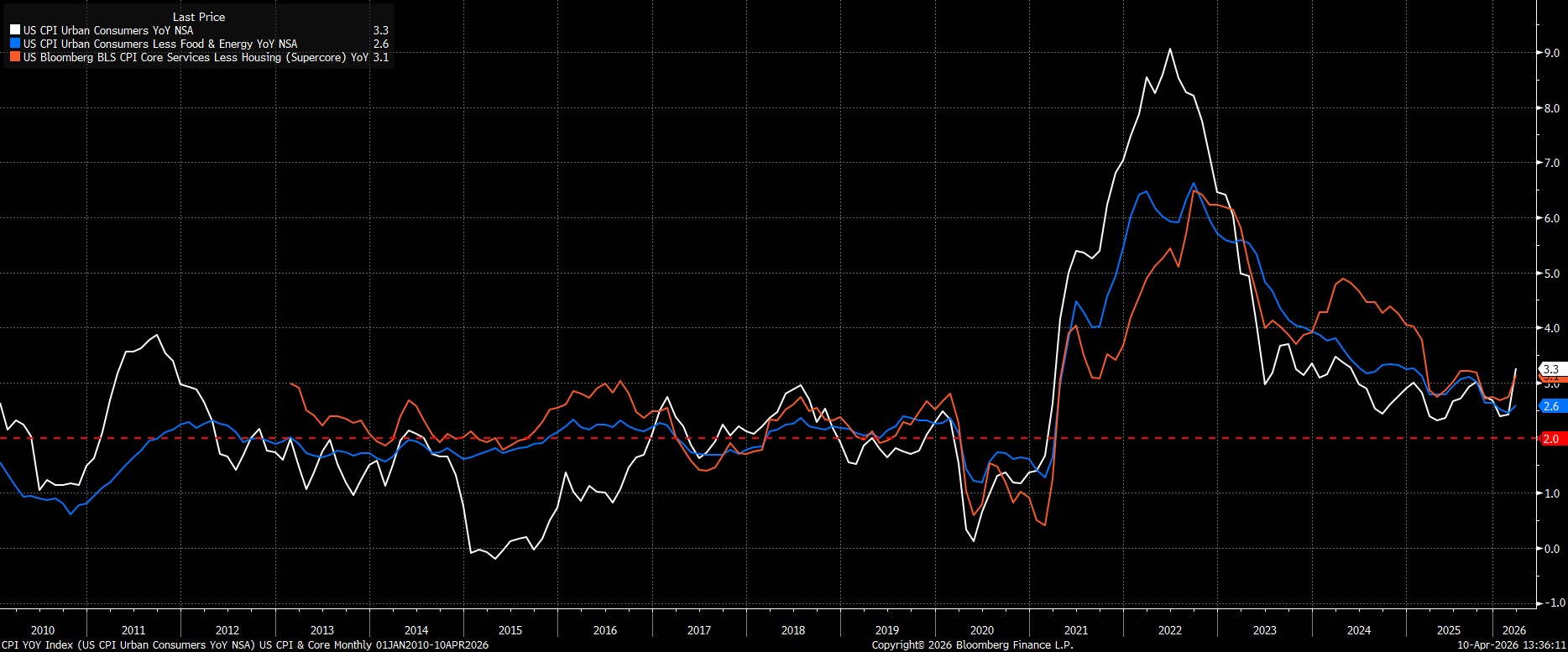

Headline CPI rose 3.3% YoY last month, a touch below consensus estimates for a 3.4% YoY increase, and the fastest annual rate of inflation since May 2024. Of course, almost all of that jump came as a result of higher energy prices, stemming from the interruption of normal commodity flows due to conflict in the Middle East.

Consequently, it is considerable more instructive to examine measures of underlying price pressures to obtain a ‘truer’ read on the inflationary backdrop. Here, core CPI (ex-food & energy) rose 2.6% YoY, the fastest pace since the back end of last year, while so-called ‘supercore’ CPI (core services ex-housing) rose 3.1% YoY.

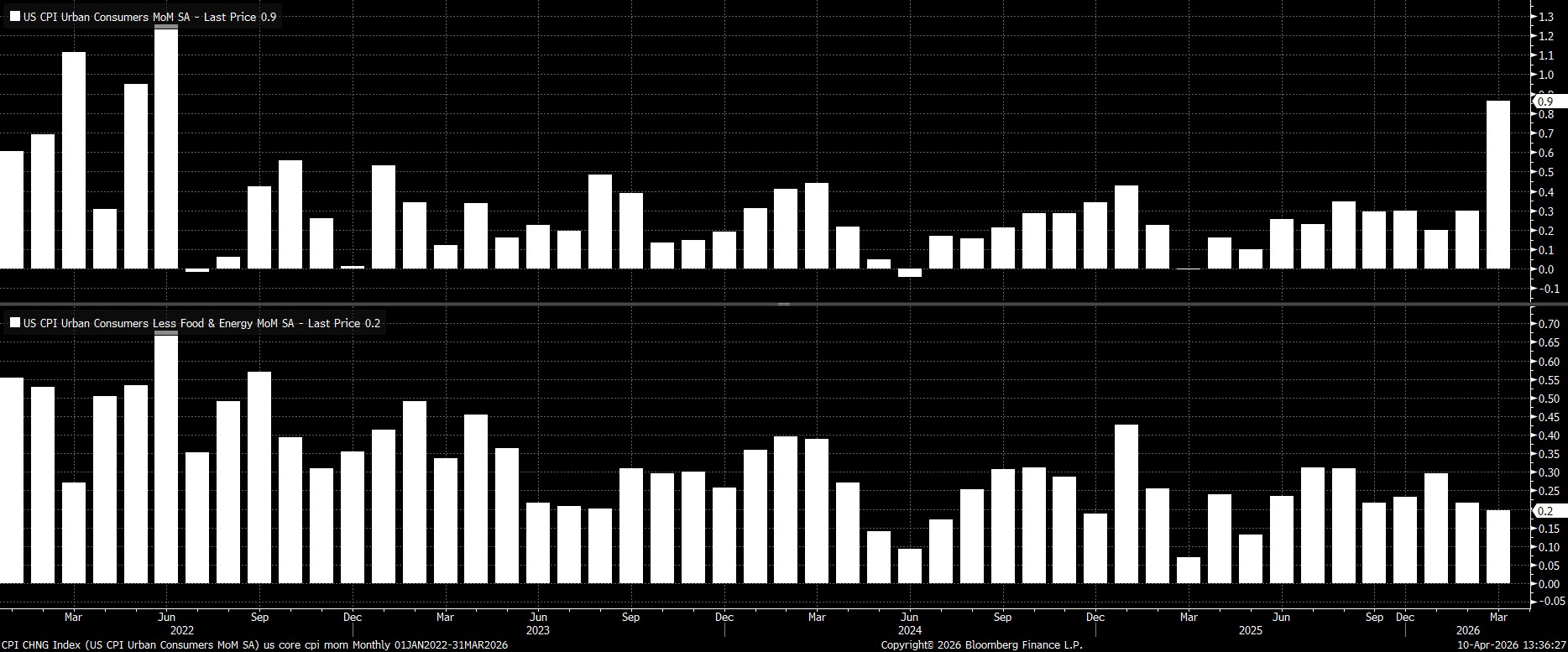

Meanwhile, on a month-over-month basis, the impact of the energy price surge is even more dramatic. Headline CPI rose 0.9% MoM in March, the biggest one-month increase since June 2022 which, incidentally, was another month when a surge in energy prices was the principal contributor to a jump in headline inflation. In any case, the monthly rise in core CPI in March was, unsurprisingly, more modest, at 0.2% MoM, unchanged from the pace seen in February.

Of course, one can annualise this MoM data in an attempt to build a clearer picture of near-term inflationary trends. However, as the below data shows, the headline metrics here are also skewed significantly higher as a result of higher energy costs:

- 3-month annualised CPI: 5.3% (prior 3.0%)

- 6-month annualised CPI: 3.8% (prior 2.6%)

- 3-month annualised core CPI: 2.9% (prior 3.0%)

- 6-month annualised core CPI: 2.3% (prior 2.3%)

Details Are Pivotal

Digging into the report, it is unsurprising to learn that energy proved the main reason for the surge in CPI seen last month, having contributed 79bp to the 3.3% YoY headline figure, and with energy prices having risen by 10.9% MoM/12.5% YoY in March alone.

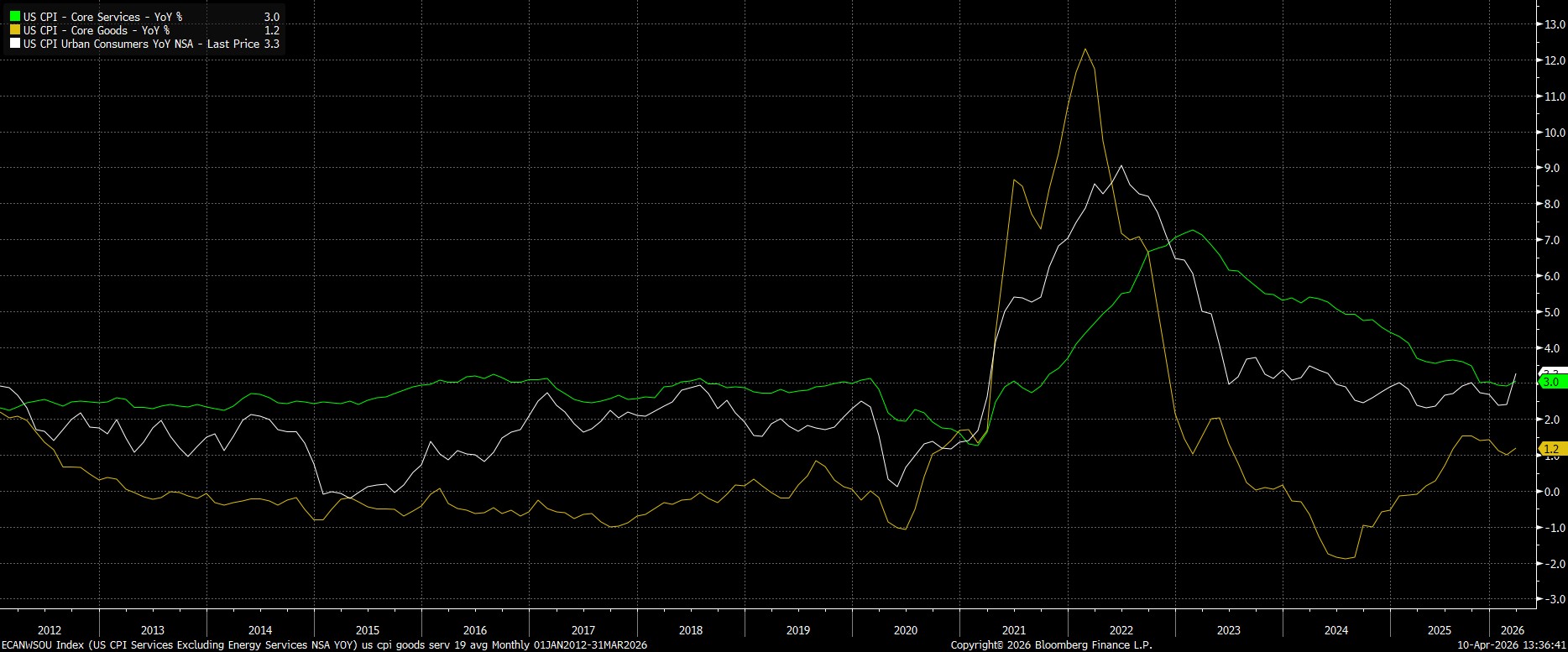

Stepping away from energy prices for a moment, the report also showed core goods prices having risen 1.2% YoY, 0.2pp above the pace seen in Feb, while core services prices rose by 3.0% YoY, unchanged from last time out. Although energy prices will grab most of the attention, and understandably so, these figures do nonetheless bear watching closely, not only as we continue to gauge whether the bulk of tariff pass-through has now been and gone, but also as the potential for second-round inflation effects, and more persistent price pressures, remains the key determinant of the near-term monetary policy outlook.

Money Markets Reprice A Touch Dovishly

In reaction to the data, money markets repriced very modestly in a dovish direction, on the back of the cool-ish core figures, with swaps now discounting around 10bp of easing by year-end, vs. 7bp pre-release.

.png)

Conclusion

By and large, the CPI report tells us what we already knew - namely, that higher energy prices lead to higher spot headline inflation.

This, in many ways, matters little for the FOMC, whose focus is not on spot inflation, but on where inflation is likely to be over the next 18-24 months. As such, policymakers are likely to place much greater weight on inflation expectations remaining anchored close to the 2% target and earnings growth running at target-consistent levels, than the data received today, given that both imply limited potential for 'second round' inflationary effects. Core inflation will also be examined closely, for any signs that higher headline inflation is creating more broad-based price pressures.

That said, the agreement of a fragile ceasefire in the Middle East, coupled with a modest retracement in energy futures, as well as the increased potential for a durable peace deal to be made, may at the margin given policymakers further confidence that any energy-induced rise in inflation will prove to be 'temporary' in nature though, of course, concrete evidence of an end to the conflict, and resumption of normal commodity flows, will be needed before that can become an assumption on which policy is made.

On the whole, though, the base case remains that the FOMC will 'look through' any hump in headline inflation that we see over the coming months, providing that second-round effects don't emerge. In turn, there remains a path for a couple of rate cuts to be delivered in the second half of the year, not least considering the fragile nature of the labour market, where recent data points to continued weakness under the surface, suggesting that a less restrictive policy stance is likely to be appropriate.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.