- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

Inflation Remains Just North Of Target

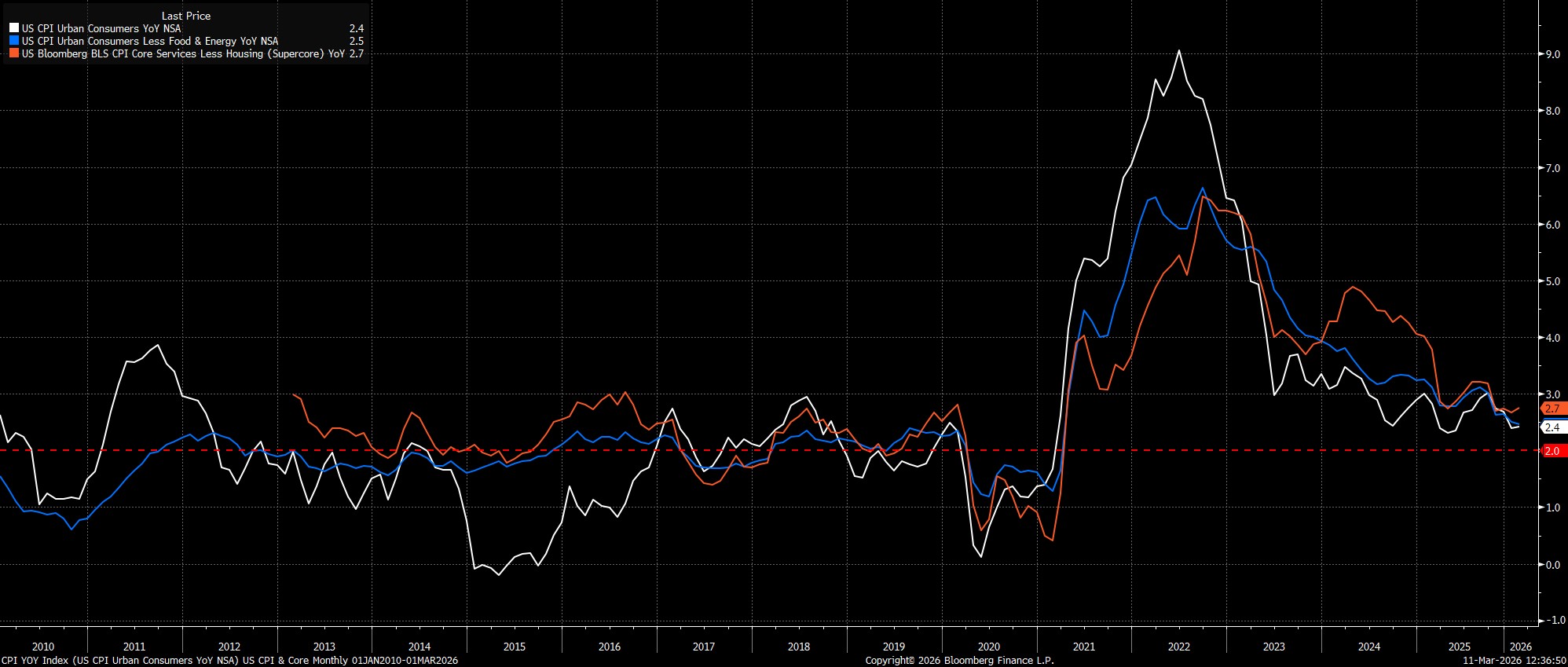

Headline CPI rose 2.4% YoY last month, bang in line with consensus expectations and unchanged from the pace seen in January. Meanwhile, underlying inflation metrics pointed to little change from last time out, with core CPI rising 2.5% YoY, and ‘supercore’ inflation (aka core services ex-housing) rising 2.7% YoY.

Importantly, with this being February data, the CPI figures do not take any account of the recent energy price shock, stemming from the outbreak of conflict in the Middle East, and the Strait of Hormuz subsequently becoming essentially impassable. This, clearly, tilts inflation risks to the upside in the near-term, with the duration of that energy shock set to determine the degree of any upwards inflation impulse that may make itself known in coming months.

In any case, returning to the February report, on a monthly basis, headline CPI rose 0.3% MoM, while core prices rose 0.2% MoM, both also in line with consensus expectations.

Annualising this MoM data helps to provide a clearer picture of underlying inflationary trends, albeit again with the caveat that said trends are now almost entirely dependent on the evolution of energy prices in the short-term:

- 3-month annualised CPI: 3.0% (prior 2.2%)

- 6-month annualised CPI: 2.6% (prior 2.8%)

- 3-month annualised core CPI: 3.0% (prior 1.7%)

- 6-month annualised core CPI: 2.3% (prior 2.5%)

Details In Focus

Drilling down into the report, participants continue to focus closely on the composition of price pressures, though from March onwards, almost all of those pressures are set to emanate from the energy sector.

In any case, last month, did see a further moderation in core goods prices, which rose 1.0% YoY, further implying that the bulk of any tariff pass-through is now in the rear view mirror. Furthermore, core services CPI rose 2.9% YoY for the second month running, likely further easing any lingering worries over the persistence of price pressures.

Next-To-No Policy Implications

All that said, the policy implications of the CPI data are essentially non-existent, taking into account both the data being backward-looking, and given how dramatically the economic outlook has shifted over the last fortnight, since conflict erupted in the Middle East.

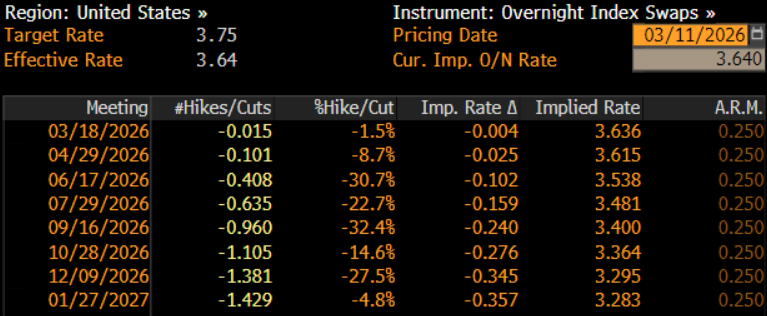

As a result, money markets continue to price the Fed as holding steady at the March meeting, with the next 25bp cut not fully discounted until the September meeting. By year-end, around 35bp of easing is priced, not too dissimilar from the 37bp priced pre-release.

Conclusion

Taking a step back, the February CPI report seems highly unlikely to materially alter the near-term FOMC policy outlook.

Having adopted a ‘wait and see’ stance at the January confab, amid signs of labour market stabilisation, the FOMC are now set to stick with such an approach for the time being, in light not only of the labour backdrop, but more importantly on the back of the upside inflation risks posed by ongoing conflict in the Middle East, and subsequent energy price shock.

Assuming that said shock does indeed prove short-lived, and that any second-round inflationary effects are limited, then further rate reductions remain on the cards, later in the year, likely under the Chairmanship of Kevin Warsh, once disinflationary progress has resumed. Policy action in the interim is unlikely, barring a significant and unexpected further deterioration in the employment backdrop.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.