- 繁体中文

- 简体中文

- English

- Español

- Tiếng Việt

- Português

- لغة عربية

- ไทย

- Equity risk to navigate

- Moving past US payrolls and firmly onto inflation

- The FOMC meeting holds hawkish risk for the USD

- BoJ focus - USDJPY moving back to intervention levels

- Aussie jobs a risk for AUD exposures

- GBP traders looking at jobs and political developments

We move on from a week where political events (Mexico, India, and South Africa) caused significant market gyrations. Notably in USDMXN, with the pair gaining a staggering 8.1% w/w - the biggest weekly gain since March 2020 – with sizeable volatility across EM FX.

We also move past US nonfarm payrolls, which produced fireworks in the US Treasury market on Friday, promoting broad USD strength and a sizeable liquidation in gold and silver long positioning. We’ve also seen indecision in the S&P500 weekly chart which needs to reconcile itself, and the stage is set for a huge week ahead of tier 1 event risk. A trading week that has it all and traders will need to be nimble and well prepared.

Equity risk to navigate

At a stock level, Apple’s Worldwide Developer Conference (WWDC) will get attention on Monday – this being the stage for Apple to officially unveil its highly anticipated AI strategy and integration and given many of the features have been heavily reported on, we may need to hear something unexpected to inspire new money into the stock or there is a risk of a ‘sell on fact’ scenario playing out. For now, the market is long and strong, and a break of $200 would be a win for the bulls.

We also see Nvidia trading in the 100s after the 10-1 split, and we look to see if the stock can hold $120 and build. On Thursday Tesla hold its AGM, where a contentious vote on Elon Musk’s $56b pay package will be the central focus – a factor that if voted down could impact the perception of Musk’s close involvement and influence in the business going forward.

GameStop won’t be far from the headlines and after the share price was essentially cut in half on Friday, on the decision to issue an additional 75m shares just before Keith Gill’s ‘convenient’ live steam, we’ll see if traders look to buy the dilution dip. GME is one for the bravest of souls, and for those who understand that GME is purely a flow-based punter's vehicle, meaning position sizing relative to the volatility is critical if one is to stay in the game.

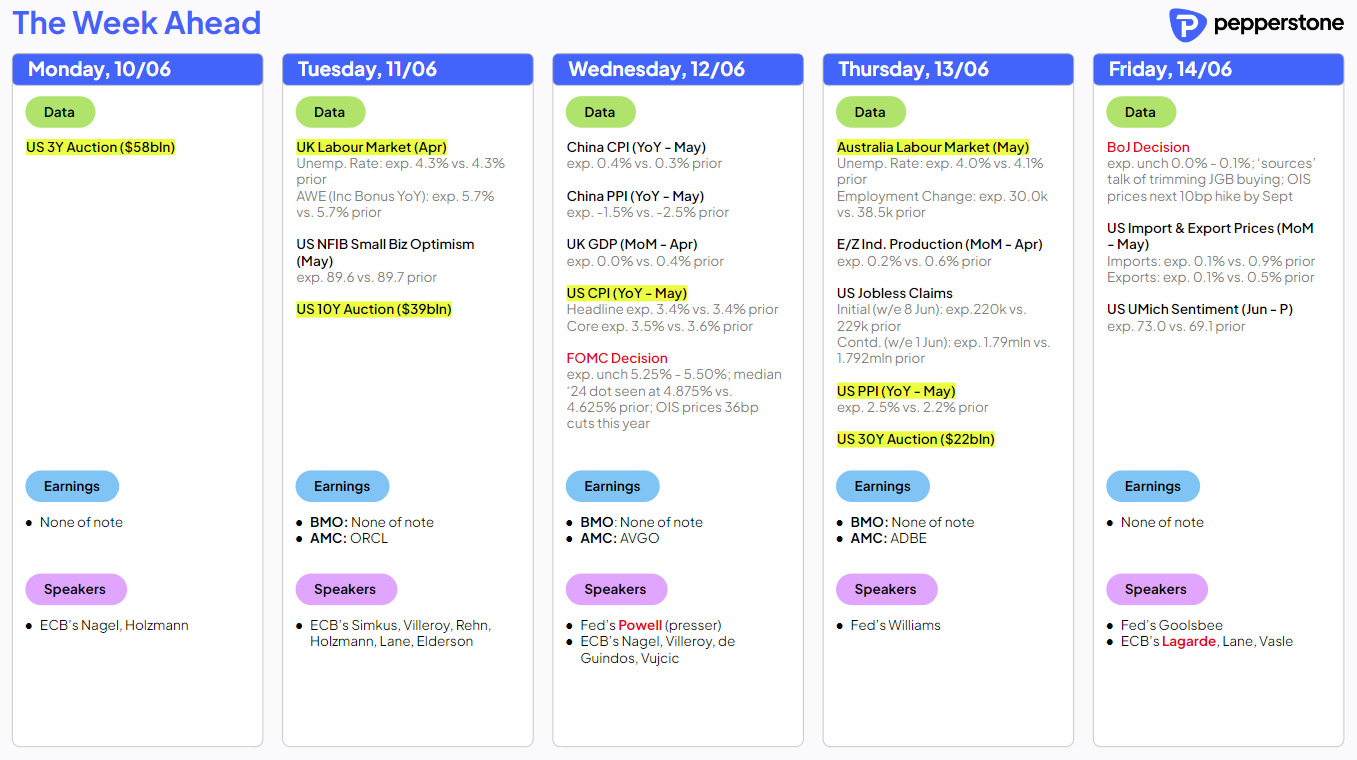

Landmines galore on the macro side

On the macro side, US CPI, PPI, and the FOMC meeting are the highlights for the week ahead, with the BoJ meeting, and UK and Aussie employment report also getting some real focus.

Friday’s US nonfarm payrolls report saw 272k jobs created in the BLS Establishment survey - a massive 4 standard deviation beat to consensus and the bigger influence on market movement over the 408k job loss in the BLS’s Household survey, the factor that pushed the US unemployment rate to 4%. The wash-up on NFPs was a 16bp rise in the US 2-year Treasury yield, with US swaps pricing out 10bp of cuts by December, and we go into the new week with 36bp of cuts now cumulatively priced for the end of the year. This sets us up nicely for Wednesday’s US CPI print, where the market sees core CPI at 0.3% m/m (3.5% y/y) and headline CPI at 0.1% m/m (3.4% y/y).

US CPI the elephant in the room

Simplistically, a US core CPI print that rounds down to 0.2% m/m (i.e. below 0.25% m/m) should offer relief to US and global equity markets and gold and would hit the USD. Conversely, a print that rounds up to 0.4% m/m would see the US swaps market move closer to price just one 25bp rate cut this year and see US 2yr Treasury yields rise towards 5% - in turn, the US dollar index (DXY) would follow and test the recent trading range highs of 105.20, with EURUSD breaking the 30 May lows of 1.0788, with the major moving average (50-, 100- and 200-day) situated between 1.0807 to 1.0778.

We can assess the breakdown in the components of inflation, with the market looking most closely at core services inflation, which is expected to moderate a touch to 0.38% m/m (from 0.41% m/m).

We also see the PPI inflation print on Thursday, and that, along with select components from the CPI basket, should allow economist’s conviction to model US core PCE inflation (due 28 June). The Fed will naturally be assessing the CPI print closely, although, it would take a true outlier print for any voting Fed member to shift their stance on future policy changes.

FOMC meeting offering hawkish risk to markets

The risk for markets from the FOMC meeting is skewed towards a hawkish outcome (i.e. US bond yields and the USD higher) and while the market will react to the tone of the statement, we could see some movement across markets depending on the revisions to the banks economic and fed funds forecasts (i.e. the ‘dots’).

We should see the ‘dots’ show a central tendency for two 25bp rate cuts (from three) this year, but there is a small chance they move to one cut – an outcome that would rock markets. Their core PCE inflation forecast is expected to be revised up to 2.8% (from 2.6%) for 2024 and the unemployment forecast to 4.1% (4%), so a revision in core PCE to 2.9% or above would be seen as a hawkish outcome.

Fed Chair Jay Powell faces the usual grilling from the press 30 minutes after the FOMC statement drops. The core message we should hear from his commentary will remain one of patience and that policy remains restrictive enough for inflation to moderate to target over time.

USDJPY should also follow US rates pricing, and the US 2yr Treasury yield, where USDJPY longs will be wanting a break of the 29 May high (157.71). A break of this trading high, notably if accompanied by a higher rate of change, will likely be met by BoJ/MoF JPY jawboning and intervention headlines. Friday’s BoJ meeting will see the bank leave rates unchanged, with the market pricing the next 10bp hike for the 31 July meeting – all the talk though has been around tweaking the bank's pace of bond buying, potentially even ending the program, but whether that impacts the JPY is debatable.

Aussie jobs a risk for AUD positions

In Australia, Thursday’s jobs report gets the focus, and while interest rate futures see no change in RBA policy this year, the RBA has made it clear that the labour market is the key variable in their thought process. The consensus call is for the unemployment rate to tick down to 4% (from 4.1%), with 30k net jobs expected to have been filled in May, so the participation rate will be key here. AUDUSD trades heavy after Friday’s 1.3% fall (the 3rd worst day of the year), with price breaking the range lows of 0.6590. On the week I’d be playing a 0.6660 to 0.6510 range and fading moves into these levels accordingly.

UK jobs/wages due amid increasing election focus

In the UK, wage and employment data could influence BoE policy expectations, with interest rate markets pricing a 55% chance of a 25bp cut in September, and 33bp of cumulative cuts priced through to December. GBP has worked well of late and has been best traded from the long side, notably against the EUR, CAD, and AUD.

The UK election gets increasing market focus, with Rishi Sunak seemingly unable to do anything right, and a landslide victory for Labour beckons. The Labour Party will release its party manifesto on Thursday, so we’ll see if there are any policies that surprise and cause unease in the GBP (or FTSE100), but the headlines for now suggest Keir Starmer is going to go hard convincing the voting public that they will not hike income tax, national insurance, or VAT. Some market participants are even questioning whether a landslide win for Labour has the potential to improve the UK’s ties to Europe - One school of thought as to why EURGBP is breaking to the weakest levels since August 2022.

Good luck to all.

Related articles

Pepperstone不代表這裡提供的材料是準確、及時或完整的,因此不應依賴於此。這些資訊,無論來自第三方與否,不應被視為建議;或者買賣的提議;或者購買或出售任何證券、金融產品或工具的招攬;或參與任何特定的交易策略。它不考慮讀者的財務狀況或投資目標。我們建議閱讀此內容的讀者尋求自己的建議。未經Pepperstone的批准,不允許複製或重新分發此信息。