- Italiano

- English

- Español

- Français

The FOMC’s Financial Conditions Conundrum

While something of an abstract concept, financial conditions are generally measured via some combination of Treasury yields, equity market performance, credit developments, and the value of the USD. Goldman’s proprietary index measuring such relentlessly headed higher through the summer months, largely a function of surging long-end Treasury yields, though has rolled over since the end of October.

There appear to be a handful of catalysts behind the recent loosening, not least the fact that policymakers have increasingly acknowledged that financial conditions should be taken into account to a greater extent in upcoming decisions. Other factors at play include the recent pullback in Treasury yields amid cooling supply worries after a lower than expected quarterly refunding announcement; a dovish interpretation of the November FOMC meeting, with markets now seeing the hiking cycle as ‘done and dusted’; continued disinflation, particularly on core (ex-food & energy) metrics; plus, a cooler than expected October jobs report, where nonfarm payrolls rose by a sub-consensus 150k, and unemployment ticked higher to 3.9%.

This loosening in financial conditions is likely to be of concern to policymakers. As has been noted on numerous occasions, there remains a long way to go to bring inflation back to target, with both headline and core US CPI continuing to hover around the 4% handle. If sustained, this is likely to become a greater concern for the FOMC, particularly if it were to put the swift achievement of a return to the 2% inflation objective under threat.

Logically, it follows that if such concern were to mount, Fedspeak would likely take on an increasingly hawkish bent. That is, in fact, what has been seen this week, with FOMC speakers seemingly following a collective script. A plethora of policymakers have been in front of microphones, most of whom have made remarks broadly in line with the theme that it is not clear how financial conditions are feeding into the real economy, and that further hikes remain on the table, depending on incoming economic data.

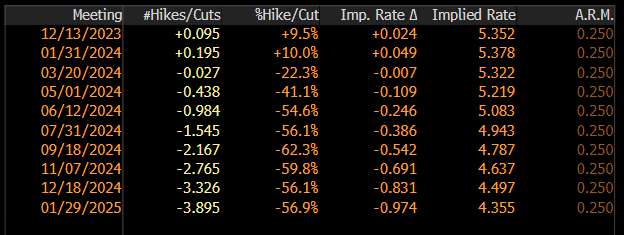

Markets, however, aren’t buying what the Fed are selling. OIS prices less than 5bp of tightening by January 2024, while also continuing to price the first 25bp cut in June 2024, while also pricing as much as 100bp of cuts to the fed funds rate by January 2025. The paradox seems to be that the more the FOMC acknowledge tighter financial conditions lessening the need for further hikes, the more markets will loosen said conditions, by pricing sooner policy easing, allowing both equities and bonds to rally.

It appears that the FOMC and financial markets are engaged in a game of bluff and double-bluff at this stage – markets are ignoring policymakers touting hikes in the belief that the tightening cycle is done and dusted, while policymakers are aware they’re being ignored, and are probably relatively comfortable with the current situation, so long as any easing in conditions is modest and slow in nature.

In terms of market implications, given the aforementioned game of bluff, and the market’s continued desire to hear only what it wants from the FOMC, dollar bulls may have to look away from policy for a source of further upside for the buck. While the DXY remains relatively rangebound for now, the 50-day moving average, currently 105.80, appears to be capping upside, with the bulls needing a break north of that level to wrestle back near-term control.

A resumption of the prior uptrend, perhaps towards a renewed test of the prior 107.20 highs, likely needs either renewed optimism towards the ‘US exceptionalism’ theme, which recent data has started to put under the microscope, and/or renewed haven demand as geopolitical tensions continue to linger.

_D_2023-11-09_15-15-35.jpg)

In the absence of either, the near-term path of least resistance seems to point to the downside for the buck. The opposite appears true for equities, with the S&P 500 now trading comfortably back above both the 50- and 200-day moving averages.

Related articles

Pepperstone non dichiara che il materiale qui fornito sia accurato, attuale o completo e pertanto non dovrebbe essere considerato tale. Le informazioni, sia da terze parti o meno, non devono essere considerate come una raccomandazione, un'offerta di acquisto o vendita, la sollecitazione di un'offerta di acquisto o vendita di qualsiasi titolo, prodotto finanziario o strumento, o per partecipare a una particolare strategia di trading. Non tiene conto della situazione finanziaria o degli obiettivi di investimento dei lettori. Consigliamo a tutti i lettori di questo contenuto di cercare il proprio parere. Senza l'approvazione di Pepperstone, la riproduzione o la ridistribuzione di queste informazioni non è consentita.