- Italiano

- English

- Español

- Français

Week Ahead Playbook: Rally Rolls On As Pivot To Policy Normalisation Continues

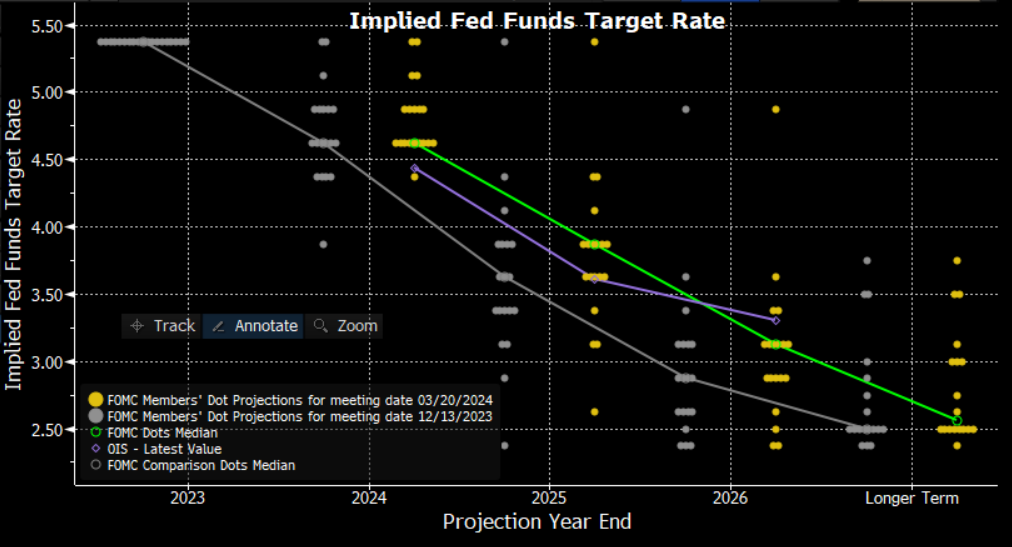

Of course, Wednesday’s FOMC decision was the week’s main event, though in many respects it was one of the most predictable, and even dull, FOMC meetings in recent times. The target range for the fed funds rate was, naturally, kept unchanged at 5.25% - 5.50%, while the accompanying policy statement was also an almost exact carbon copy of that issued after the January decision, confirming that policymakers remain data-dependent, continuing to seek confidence that inflation is returning towards the 2% target before delivering the first rate cut.

That rate cut is still on its way, with the latest ‘dot plot’ again pointing to a median expectation for 75bp of easing being delivered this year, albeit while portraying a much tighter dispersion in the dots than the prior iteration. At the same time, and something perhaps overlooked by markets thus far, the 2025, 2026, and longer-run median dots were all revised marginally higher, perhaps an indication that the easing cycle will be a tad shallower than markets presently price.

Nevertheless, the core message from the FOMC remains the same, despite three straight hotter-than-expected headline CPI prints, and an upward revision to the Committee’s inflation forecasts in the early part of the projection horizon.

That message is that policy normalisation remains the primary focus, with the first rate cut still likely to be delivered in June, following a further pivot in the statement at the May meeting. Hence, with policy still set to ease as the year progresses, and the flexible Fed put remaining alive and well, with larger cuts and/or significant liquidity injections on the table if conditions were to sour significantly enough to require them.

The focus for risk, in particular, remains what the Fed can do, not necessarily what the Fed will do; and, with the battle against inflation all-but-over, what the Fed can do is to provide as much policy support as deemed necessary. This, then, should continue to keep a lid on equity vol for the time being, and leave the ‘path of least resistance’ leading to the upside. Incidentally, the S&P is set to close the week with a gain of around 4%, the index’s best week since last November. Further upside seems plausible over both the short- and medium-run.

Away from the FOMC, other G10 central banks sung from a relatively similar hymn sheet.

The BoE, while keeping rates unchanged, took a modest further dovish step, with the two hawkish dissenters from February falling back in line with the majority of the MPC in preferring to keep Bank Rate on hold, while Governor Bailey noted that market bets on rate cuts, with GBP OIS fully pricing three 25bp reductions by year-end, are “reasonable”. A BoE cut in June, after headline CPI hits the 2% target in spring, seems reasonable.

Elsewhere, the ‘summer of easing’ theme was also reiterated by the Norges Bank, who see rates “gradually moving down” as the year progresses, having also maintained rates this week, and by the RBA, who ditched the tightening bias from the March policy statement.

The Swiss National Bank (SNB), meanwhile, went one step further, delivering a surprise 25bp rate cut, and becoming the first G10 central bank to ease this cycle, after inflation sunk to the bottom of the SNB’s target band. Quarterly cuts, to keep pace with the ECB, seem likely from here on in, as focus remains on preventing real CHF appreciation. Unsurprisingly, given the unexpected policy action, the Swissie is set to end the week at the foot of the G10 leaderboard, with EUR/CHF having popped to its highest since last July.

This easing bias, however, is not shared by all G10 central banks, even if this year is set to see – globally – the most synchronised policy easing cycle since the GFC.

It is, of course, the Bank of Japan who continue to buck this trend, with this week seeing the BoJ finally exit almost a decade of negative rates, bringing the global NIRP experiment to an end, delivering a 10bp rate hike, the first since 2007, after strong earnings growth gave policymakers confidence that inflation is once more becoming embedded within the economy. The BoJ also ceased yield curve control (YCC), while also bringing to en end ETF and J-REIT purchases, drawing a line under decades of ultra-loose monetary policy.

These steps, though, should be viewed more as a ‘one and done’ move towards normalisation, and likely do not represent the beginning of a prolonged, or aggressive, tightening cycle. While further hikes are plausible, particularly if inflation continues to tick higher, said hikes are likely to be very limited in their extent. Thus, any hope of JPY appreciation by virtue of the BoJ being a hawkish outlier among G10 central banks seem somewhat misplaced, with the JPY set to continue trading as a proxy for Treasuries for some time to come.

BoJ aside, and as alluded to earlier, the ‘week that was’ has confirmed the broader direction of travel that monetary policy is set to take over the remainder of the year. While, as noted, this should continue to be a fillip for risk, and keep equity vol subdued, it also simultaneously raises the prospect of some life being breathed back into both the FX and FI arenas.

This is by virtue of the policy divergences that will open as policy is eased at a varying pace, and to differing degrees, across developed markets. Said divergences have already become clear this week – with the SNB’s surprise cut a prime example – and will likely become wider, and more obvious, as time progresses.

Risks, at this juncture, appear biased towards the ECB, and BoE, delivering a greater degree of easing than markets presently price, while pointing in the opposite direction for the FOMC, with a more hawkish outlook distinctly possible, potentially pushing the first cut back into the summer, particularly if the present labour market tightness persists, and services inflation remains stubbornly high.

In such an environment, the dollar should continue to gain ground, particularly against lower-yielders, with dips in the buck set to be relatively shallow, and well-bought.

_D_2024-03-22_11-38-58.jpg)

Turning to the week ahead, which is holiday-shortened owing to Good Friday, and the economic calendar is substantially quieter, with few notable event risks for markets to navigate.

The standout release comes on Friday, with the latest US PCE figures, as the core PCE deflator – the FOMC’s preferred gauge of inflationary pressures – is seen remaining unchanged at 2.8% YoY. Of note, the PCE figures are unlikely to be as significantly skewed by rent and shelter costs as the CPI metric, somewhat lessening the risk of an upside surprise. In any case, the report should show a continuation of the relatively bumpy disinflationary trend underway within the US economy, and is unlikely to be a game-changer from a policy point of view.

Other noteworthy releases are relatively thin on the ground. A handful of Fed speakers, including Chair Powell, are due, though rhetoric here is highly unlikely to deviate from the script laid out at Wednesday’s post-meeting press conference, and fresh policy hints are likely to be lacking.

Sticking with the policy front, the Riksbank are due to announce their latest rate decision. Though no changes are expected, the world’s oldest central bank is likely to follow G10 peers in pointing to easing in the months ahead, with markets pricing a 6-in-10 chance that the first 25bp cut is delivered in May.

More broadly, market participants are likely looking further ahead to the next significant risks on the radar – namely, the next US jobs report on 5th April, CPI on 10th April, and the beginning of Q1 earnings season the following week. Until then, with data-flow set to be relatively limited, markets should continue to take the path of least resistance, which continues to lead higher for both the greenback, and global equities.

Related articles

Pepperstone non dichiara che il materiale qui fornito sia accurato, attuale o completo e pertanto non dovrebbe essere considerato tale. Le informazioni, sia da terze parti o meno, non devono essere considerate come una raccomandazione, un'offerta di acquisto o vendita, la sollecitazione di un'offerta di acquisto o vendita di qualsiasi titolo, prodotto finanziario o strumento, o per partecipare a una particolare strategia di trading. Non tiene conto della situazione finanziaria o degli obiettivi di investimento dei lettori. Consigliamo a tutti i lettori di questo contenuto di cercare il proprio parere. Senza l'approvazione di Pepperstone, la riproduzione o la ridistribuzione di queste informazioni non è consentita.