- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

JPY’s Direction Hinges On BoJ Governor Announcement

_2023-01-11_14-55-56.jpg)

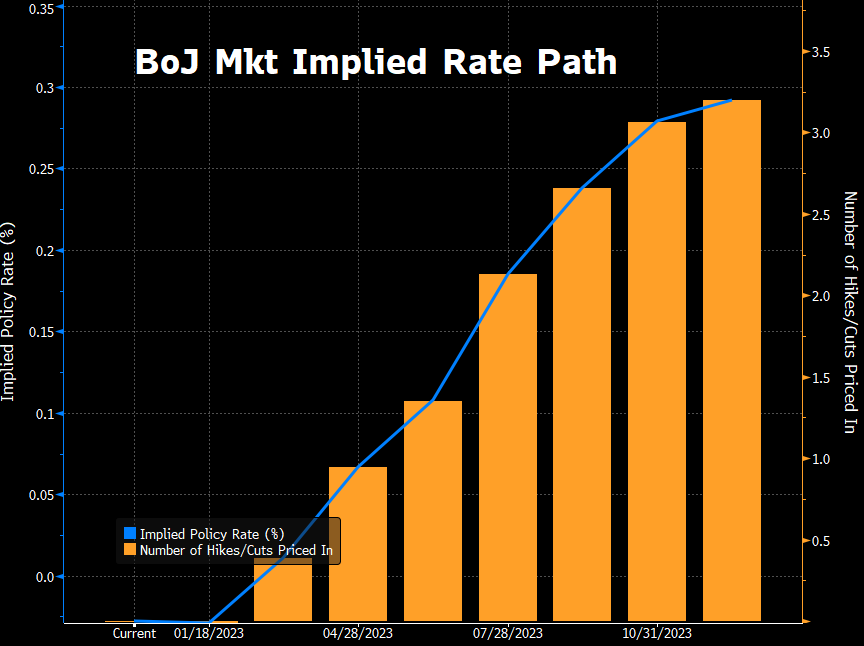

While the BoJ has already made a hawkish pivot, tweaking its YCC policy to allow 10-year JGBs to trade as high as 0.5%, it is widely expected that the appointment of a new Governor will herald a further hawkish shift in the Bank’s policy stance. Said further shift will likely lead to a rate hike in the second half of the year, bringing to a definitive end the era of ultra-easy monetary policy.

Despite such a move being broadly expected, and the JPY having already rallied significantly in recent months, confirmation of a hawk being installed as Governor is still likely to be a bullish catalyst. This is even more likely in an environment where long-end Treasury yields have become trapped in a range just over 40bps wide and show little sign of wanting to take another trip towards the cycle highs seen in Q4 22. In fact, if anything, the ‘path of least resistance’ seems to be for Treasuries to rally further, given that economic momentum will continue to wane, inflation looks to have peaked, and bets on Fed loosening are set to ramp up as the year progresses.

An announcement as to the next BoJ Governor is likely towards the tail end of January, or at the beginning of February. Current frontrunners for the role appear to be Hiroshi Nakaso, a former BoJ Board member prior to the GFC, and Masayoshi Amamiya, currently BoJ Deputy Governor.

Of the two, Nakaso is clearly the more hawkish, having been with the BoJ when it ended JGB purchases in 2006, and having also recently written a whitepaper outlining how a decade of ultra-loose policy could come to an end; abandoning the 10-year yield target, to focus instead on short-term maturities, before then raising rates.

Amamiya is significantly more dovish than his main competitor for the job, having been the mastermind behind Kuroda’s initial round of JGB purchases though, admittedly, his remarks have taken on a more hawkish bent of late, increasingly focusing on the exit from the present policy stance.

Nevertheless, and while other candidates are in the mix – including Chair of the Japanese Government Pension Fund Hirohide Yamaguchi and President of the Asian Development Bank Masatsugu Asakawa – markets are unlikely to focus on the nuance around such a decision. Instead, upon the new Governor’s unveiling, traders’ attention will immediately fall on the likelihood of the appointee delivering at least one 25bps rate hike before year end.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.