- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

The Six Bank Stocks to watch now

Create a live account to trade banks now

Bank shares have certainly had an interesting time in the past while. The rise in inflation and the subsequent tightening of US interest rates have been some of the most unrelenting and brutal ones in memory - and traditionally, hawkish times can serve banks well. On the other hand, recession and the banking crisis including the collapse of Silicon Valley Bank (SVB) introduced a lot of uncertainty over the banking sector, and whether it could lead to a rapid pull-back in the supply of credit into the real economy.

But while uncertainty is the bane of investors, it can be a golden opportunity for traders. We break down some of the most interesting banks to watch in the wake of recent months.

Why are banking stocks so popular?

In the stock market, banks can be a key indicator on economic activity, and represent a more cyclical investment, backed by the ‘safety’ of the rigorous nature of financial services regulations in most countries. Commercial banking services - especially the G-SIB (Global Systemically Important Banks institutions) must comply with certain levels of liquidity, financial stability and a host of other rules that other businesses don’t need to follow. This can represent a lot less risk and ‘fly by night’ actors than in other sectors.

Banks offer diversification to investors who have been heavily exposed to growth too. Their revenue streams offer diversification as they typically make money by borrowing at very short-term rates and lending at longer-term maturities rates. This is why, historically, banks share prices have held a strong relationship with the steepening or flattening of the yield curve. And, because banks also make money off of clients’ deposits, and invest that money by buying Treasuries and other bonds or lending to households or businesses’ loans, the banking sector are the stocks who are often most uniquely affected when lending rates change.

Another reason bank shares are so popular is that they historically do well in environments that many other equities perform badly in. Take for example hawkish times of substantial interest rate hikes. Let’s look at an example: if banks can borrow (source funding) at 4% and make loans at 5.5% then they can make money.

However, it’s important to mention that this isn’t always the case. In recent times, the rapid rise in interest rates has also called into question the future demand for loans, the asset quality of financial institutions and the costs in acquiring deposits. With this in mind, one could argue they are an even stronger bellwether of economic activity and could dictate broad market sentiment.

Add to this the fact that commercial banks are a need, not a want, for just about everybody - even when times are tough, most people won’t be cutting up their credit cards when they cut out ‘luxury items’ - and you have an extremely compelling case for many traders and investors around the world.

Lastly, many of the U.S. banks (including smaller and regional ones) enjoy direct exposure to one of the biggest, most lucrative growth opportunities of the past few decades. FinTech - the cutting-edge of how technology is revolutionising money and payments - has raked in big bucks in the past. And a lot of that economic growth went to banks.

The most popular times to trade on bank shares

Financial sector stocks are often in demand. Traders will generally be particularly interested in banking share prices at times of volatility, heightened interest in the banking industry and during certain stages of the economic cycle. These include:

- During a banking crisis or in the event of a bank failure, such as the Silicon Valley Bank collapse

- In earnings season, on the dates when the largest banks release their most recent financial results - and US banks commence the quarterly US earnings

- During a recession, economic downturn, financial crisis or some other period of uncertainty, when there is often higher volatility in the stock market, it's in this environment that traders may seek to be more active with banking stocks, taking short and long positions on them

- During a hawkish period when central banks are raising interest rates - making the interest that they earn more valuable (this goes for investment banks and those that offer financial services like wealth management, mortgages and insurance in particular)

- In particular, on the day of an influential central bank announcement such as the U.S. Federal Reserve

- In an environment where there’s rising unemployment, and people see lower demand for loans or more non-performing loans. In these climates, concerns often arise around banks’ balance sheets, which may present an opportunity for some traders

The top 5 banking-related stocks to watch now

- JPMorgan Chase & Co.

- Bank of America Corporation

- Wells Fargo

- UBS Group

- Deutsche Bank

- S&P regional bank ETF and regional U.S. banks

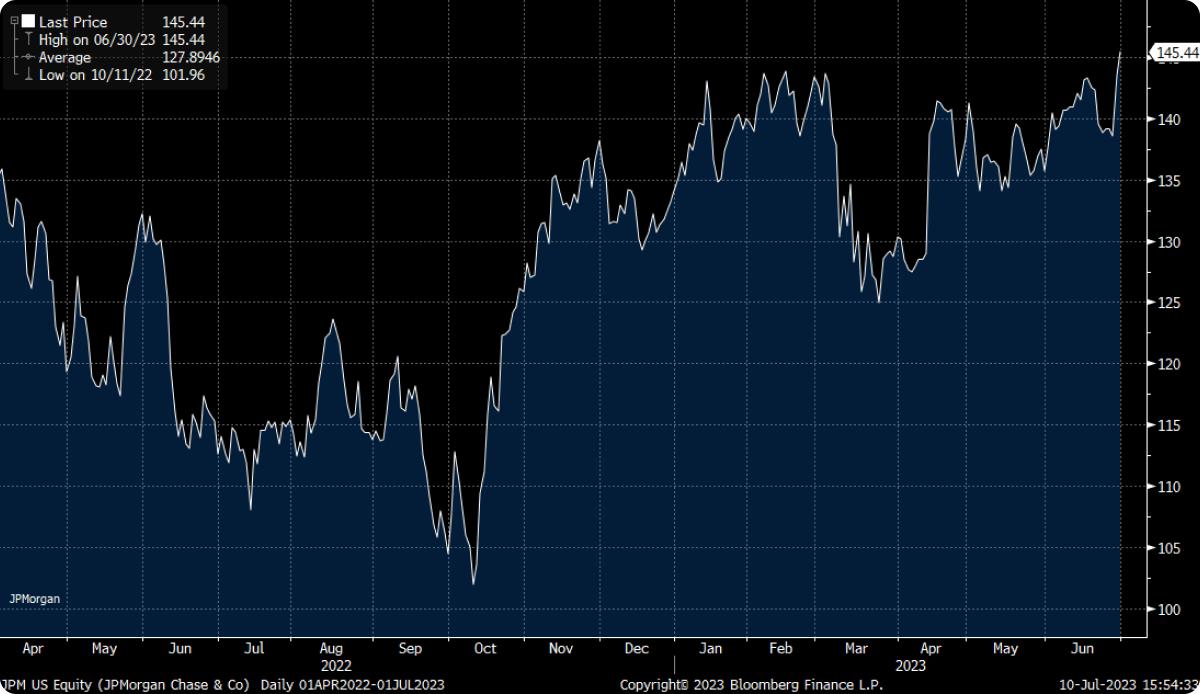

1. JPMorgan Chase & Co.

It would be impossible to mention types of banks to watch without naming JPMorgan Chase first- they are seen as the premium financial institution. The American banking industry titan has had a good 2023 so far, to say the least: it announced its highest quarterly revenue ever in Q1 FY2023. Its net income was $244 million, compared with a net loss of $856 million in the year before.

Much, if not all, of this impressive profit is due to the soaring interest rates that have defined the previous year. Now that the Fed may be softening interest rate hikes soon (when is anyone's guess), traders and investors alike will be watching to see if JPMorgan can keep this up.

July 2023 will also be the company's first earnings season since their acquisition of most of the assets of First Republic after its highly publicised bank failure in the first half of 2023.

Another important thing to note about JPMorgan Chase, which may have slipped under the radar: the U.S. Federal Reserve is launching an instant payments consumer banking system, called FedNow, towards the end of July 2023. With JPMorgan as FedNow's most high-profile guinea pig (it has been trialling the new payments system for some time), the bank is ideally positioned to benefit from FedNow from day one, and there could be interesting innovations ahead for the bank.

2. Bank of America

Another major player reaping the rewards of the hawkish environment is the Bank of America Corporation (BoA), the group which owns American banking giant Merrill (previously Merrill Lynch).

Similarly to JPMorgan, BoA reported a strong set of results in April 2023. The bank's net interest income climbed 25%, while net income rose 15% from $0.80 earnings per share in Q1 2022 to $0.90.1

Of course, banks may not have such an easy a time of it going forward, with recession likely to loom over the next few quarters. In the BoA Q1 FY 2023 earnings conference call, CEO Brian Moynihan predicted that the upcoming recession would be “mild”, likely causing a few raised eyebrows on the banking clients’ end. BoA in particular has a significant amount of focus in the U.S. mortgage and commercial loans market - both of which could get quite a shake-up if the economic climate turns harsher than Moynihan’s prediction. Either way, with BoA a literal representation of American banks in the minds of many, this will be a closely-watched banking stock.

3. Wells Fargo

Arguably the second biggest winner of the American banks, when it comes to the Q1 FY2023 results, is Wells Fargo. The bank reported a 34% increase in its net income year-on-year in Q1 of FY2023, as well as announcing that net interest income had climbed a whopping 45%.

It's also been particularly popular with its investors, by increasing its dividend by 17% in this period, significantly more than most other retail banks' dividend yields. Earnings per share were hiked from $0.90 to $1.23 in Q1 FY2023 - a significant amount.

However, just like JPMorgan, eyes will be on whether the bank can maintain its winning streak after interest rate hikes calm down.

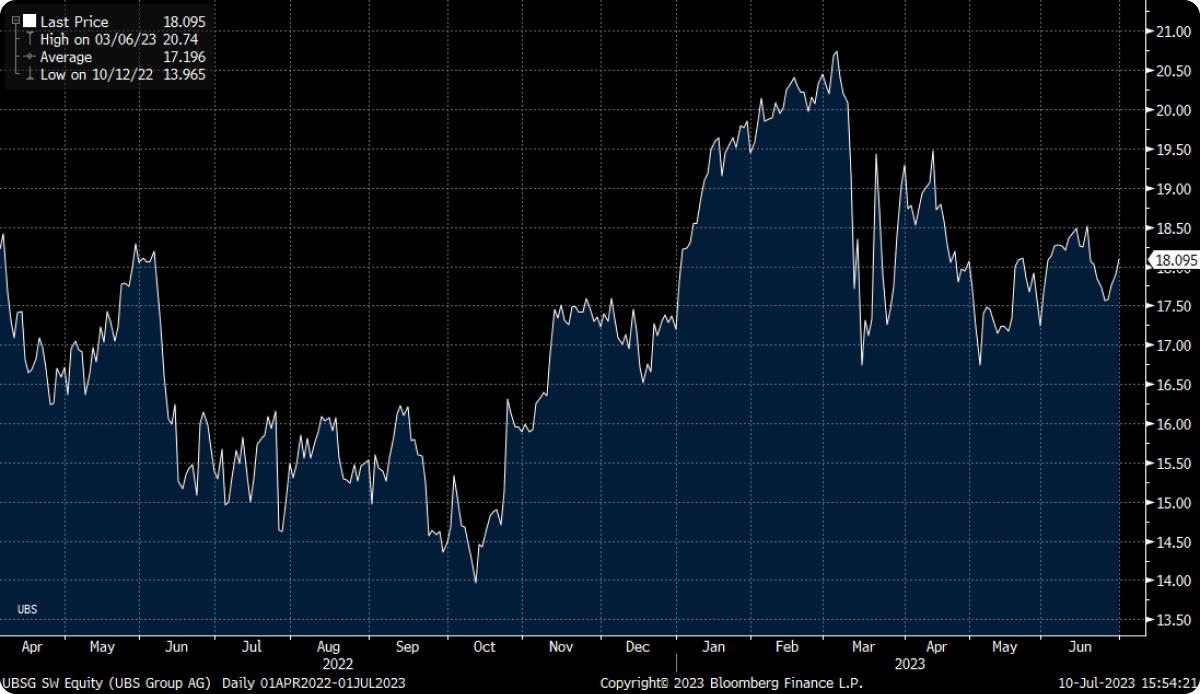

4. UBS Group

Interest in Switzerland's UBS Group AG will be heightened in the coming weeks. In March 2023, following the SVB-led banking crisis, the group bought Credit Suisse in one of the biggest investment banking acquisitions in recent history.

Its first earnings season post this enormous merger was arguably even more interesting, reflecting a European financial backdrop fraught with 2023 financial pressures. UBS reported that total revenues had decreased 7% YoY, even as annual expenses increased by 9%. Perhaps most memorably for the investors, net profit attributable to shareholders decreased 52% to $1,029 million in Q1 FY2023.

It will be very interesting to see what the UBS stock price does next, in the midst of class action protesting its Credit Suisse acquisition. In the face of this public pressure, the Swiss group may well announce that it won't make use of any government backstops to help financially support its buying of Credit Suisse - which may affect its August 2023 results even further.

5. Deutsche Bank

Meanwhile, Deutsche Bank is singing a very different tune in Europe. The German banking stalwart's boat has also been lifted by the ongoing tide of ECB interest rate hikes. In its Q1 2023 earnings season, it reported profits before tax of €1.9 billion YoY - its most profitable quarter since 2013. Similarly, net revenues in Q1 2023 were at their highest since 2016, at €7.7 billion.

Those in the know have been watching Deutsche Bank closely since mid-March 2023, when the Credit Suisse crash saw panicked U.S. customers withdrawing hefty amounts from the German bank as well. However, with a string of new high-profile hires and an uneventful recent integration of its Postbank IT acquisition, the bank seems to be running like Swiss - that is, German - clockwork. An earnings season release showing more returns on equity and a healthy balance sheet should boost this bank for even more strong growth.

6. Regional U.S. banks and the KRE ETF (S&P regional bank ETF)

This is not a single stock per se, but it is a vital portion of the banking sector to keep an eye on. While big, international banks like JPMorgan and Wells Fargo are required by regulation to have huge capital reserves to weather both short-term volatility and recessions, regional banks are not. It's the United States regional banks that will suffer the most scrutiny if there are concerns about the asset quality of banks as US Treasury yields move higher - just as they did after the banking crisis in April.

“Many of the smaller and regional banks have already had to go use the Federal Reserve’s liquidity facilities that were rolled out in March to address their liquidity needs,” adds Peppertone’s Head of Research Chris Weston. If this were to happen again, so soon after the SVB saga, it could be an interesting opportunity for traders.

“We’re also concerned that the demand for loans will fall as mortgage rates push well above 7% and the cost of capital is ballooning,” Weston adds. If this hurts the bottom line of regional banks, it too may serve traders looking to short bank stocks and otherwise take advantage of near-term volatility.

The S&P Regional banking ETF (known as the KRE ETF for short) is one way to trade on a broad range of regional U.S. banks with a single position. The ETF, which tracks American banks like New York Community Bancorp and Regions Financial Corporation, is a well-known bellwether for a more grassroots take on how the American banking sector is doing apart from the big players.

How to trade on bank stocks with us

Pepperstone is proud to offer some of the largest bank stocks in the world, which you can trade on the MetaTrader 5 platform. Here's how:

- Open a demo account to practise and finetune your bank stocks trading strategy

- Create a live Pepperstone account and fund it to get started

- Download the MT5 platform, following the prompts, via our secure client area

- Once the platform has loaded, input your account number, password and server name to connect MT5 with your trading account

- Study the markets and find the bank stock, or banking sector ETF, you want to trade. With us, you'll trade using CFDs

- Open your first trade on MT5 by clicking 'buy' (to go long) or 'sell' (to go short) in the deal ticket

- CFDs are complex instruments, so consider setting up stop loss and take profit orders to maximise your risk management

- Monitor the markets and close your trade when ready

The TL:DR Summary

- Traditionally, bank stocks have been popular with many traders and investors because of the raft of regulations policing banks, as well as the fact that bank stocks typically respond differently to other equities in hawkish times.

- The banking sector has also seen plenty of ‘interesting times’ recently, with banking crises, including the failure of Silicon Valley Bank, and aggressive interest rate hikes.

- Going into this next quarter, many traders will be on the lookout for banking sector volatility to trade.

- We think that, in particular, eyes may be on JPMorgan, Bank of America Corp, Wells Fargo, UBS Group, Deutsche Bank and regional U.S. banks

- You can trade on many bank stocks, as well as banking ETFs such as the KRE ETF, with Pepperstone on the MT5 platform.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.