- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

US Q4 earnings preview - the catalyst for a leg higher in equities?

Fiscal stimulus, the roll out of a vaccine and central bank liquidity has all been core to the rise and rise of equity markets, with the market firmly of the belief that we are due to see a strong economic and earnings recovery in 2021. With that in mind, one questions whether the outlooks from CEO’s and CFO’s meet the vision the market has discounted? Conversely, is the consensus once again too low, where a more inspiring outlook accelerates the notion of a re-rating of earnings expectations, lowering valuation, pushing US equities even higher?

The signs are promising

Consider that around 17% of the S&P500 companies have pre-guided in the so-called ‘confession season’, with a punchy 51% having revised up its earnings guidance and 56% on sales – as we see from the Bloomberg chart this is about as healthy a ratio as we’ve seen for years.

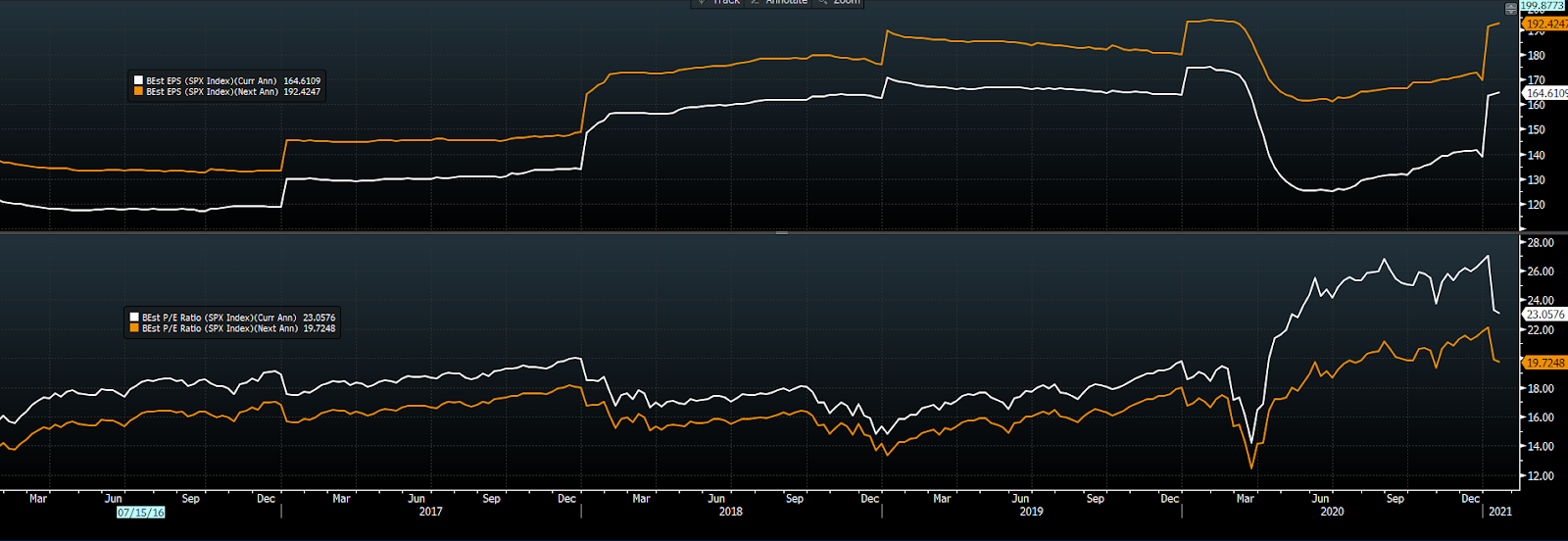

By way of expectations, analysts expect 2.3% earnings growth in Q4 (QoQ), which takes us to a second consecutive quarter of EPS (earnings-per-share) growth of 2.3% QoQ, after recording 4.1% in Q3. On a full-year calendar basis, 2020 EPS are expected to fall 11.6%, however, this should mark the trough in earnings and the start of the recovery phase – a fate the market is already betting on if you look at expected earnings for FY21 and FY22.

Top pane – current year EPS (white), 2022 (orange)

Lower pane - current year P/E ratio (white), 2022 PE ratio (orange)

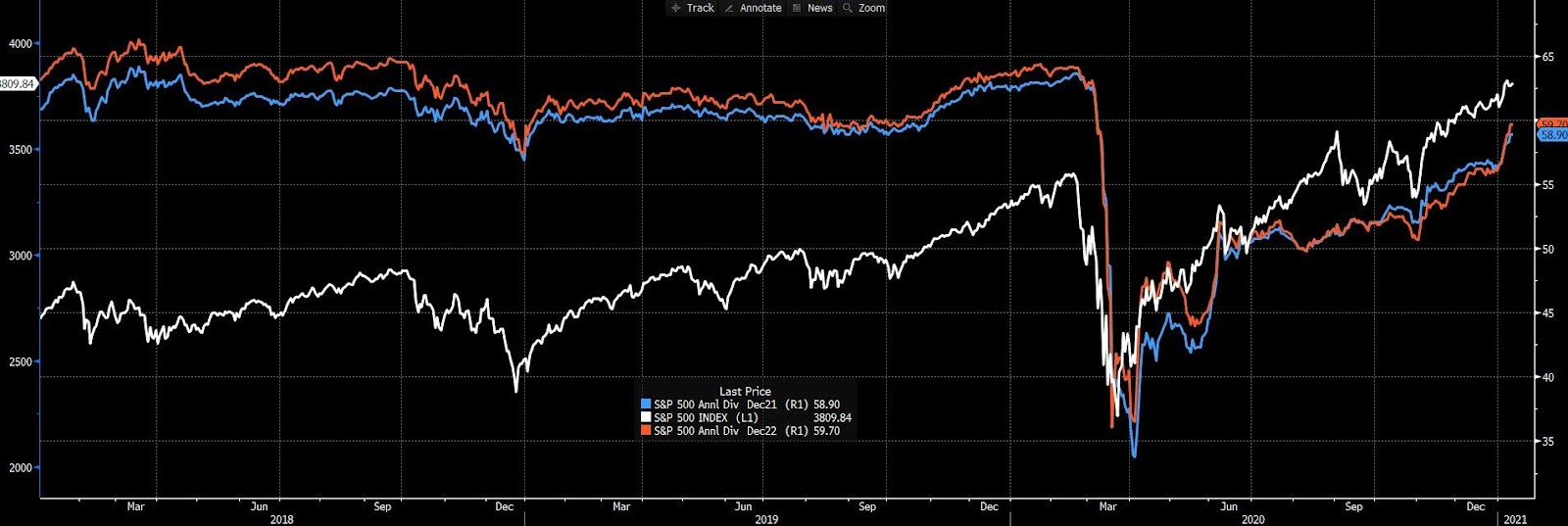

Traders can trade dividend futures through the CME, either as a vehicle to express a view or simply to hedge their investment through periods of extreme uncertainty. As we see below, expectations are nearly back to where they were pre-COVID.

(White – S&P500, blue – S&P500 dividend futures Dec 2021, orange - S&P500 dividend futures Dec 2021

It also would in no way surprise to see at least 75% of companies beating expectations on EPS and over 70% on sales, such has been the trend that analysts are typically lowball in their estimates. However, while investors may look at actual earnings relative to expectations, the reaction will come from the outlook. What will CEO’s and CFO’s say about uncertainty about a higher tax regime? Will there be signs of price pressures which could be considered inflationary - one of the core debate being had in the macro community right now? Will leaders suggest they are seeing encouraging signs of a demand returning, or at least how they will fare should pent-up demand, notably in the service sector, return in the period ahead?

Of course, there are many other debates investors want answers to and one questions if earnings season could be the catalyst for elevated forward PE ratios to head lower and normalize somewhat.

US Q4 earnings matrix

By way of a guide for traders, I have compiled a list of some of the trader favorites from the full universe of US stocks that Pepperstone offers and looked at their pedigree around quarterly earnings. I have also looked at the average moves, the implied movement (derived from options pricing), and other important variables that could offer an expectancy to hold positions over the earnings announcement.

Apple, for example, has incredible form when it comes to beating consensus expectations for sales and EPS, while also offering guidance for the quarter ahead. The implied move on the day of the announcement is 4.9%, so one suspects this will be well traded by clients. Intel is another which has seen an average move of 7.4% on the day of reporting over the past eight quarters and has an implied move of 6.5%, with a solid pedigree of beating the street. Tesla has a 9.1% implied move, but it’s not typically about the earnings but more the vision – again, another I expect clients to be heavily involved with and who knows we may see analysts revise their price targets closer to the current price.

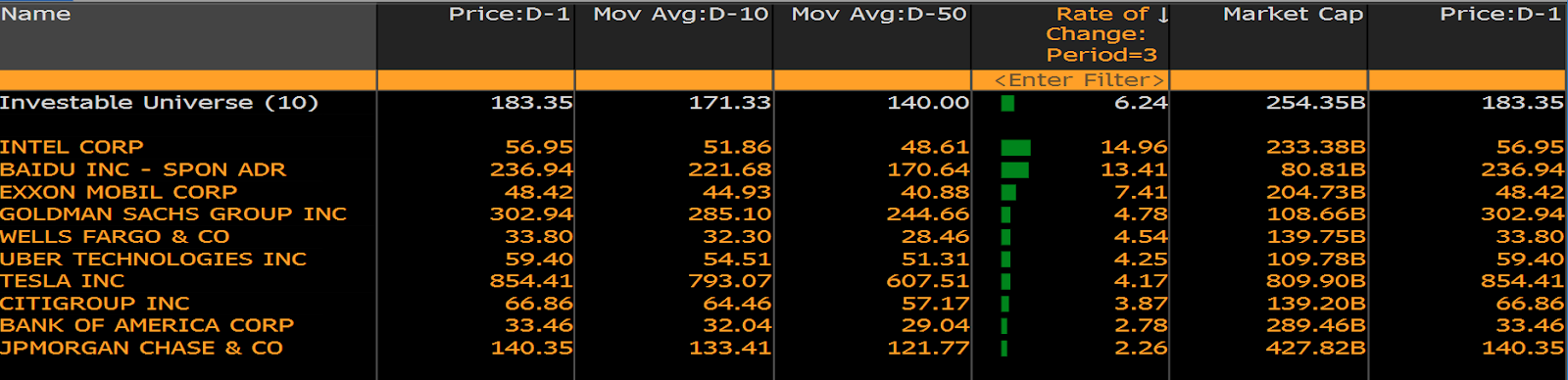

Another aspect is to see which stocks are being best bid into earnings, which could be a sign of a higher conviction of a positive outlook. Scanning our universe of stocks for underlying strength and momentum into earnings, using the variables accordingly:

- Rate of change > 2

- Price > 10-day MA

- Price 10% > 50-day MA

The stocks that are filtered on the scan are as follows. Will the markets confidence prove to be justified?

So, watching earnings season closely to see if it proves to new catalyst to drive the next leg higher in US equity markets. Conversely, could it prove to be a driver of market volatility if the outlooks don’t meet the mark?

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.