- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

Bitcoin Tests $70,000: High-Beta Behavior Persists, Institutional Funds Remain Key

.jpg?height=93&quality=100)

Bitcoin has recently made another push toward the $70,000 mark, approaching the upper boundary of its February range at $71,900, indicating potential for a short-term breakout.

Against the backdrop of heightened cross-market volatility driven by geopolitical tensions, traders are closely watching whether Bitcoin will act more like a safe-haven asset or a risk-on instrument in the near term, while also monitoring if it can establish a trend to guide their strategies.

Bitcoin Shows Strong Correlation with Risk Assets

Cross-asset correlation data since March 1 show that following the outbreak of geopolitical conflict, Bitcoin has moved closely in line with the Nasdaq 100 (NDX) and actively managed tech growth ETFs such as ARKK. This suggests that, in recent short-term fluctuations, Bitcoin behaves more like a high-beta risk asset rather than a safe haven.

_2026-03-12.png)

During this period, U.S. equities—especially tech stocks—have shown relative resilience. Lower dependence on energy imports provides the U.S. market with some buffer against geopolitical shocks, while the “Magnificent Seven” tech companies operate with relatively defensive business models, making them less sensitive than export-driven Asian tech or cyclical industrial and consumer sectors to macro volatility. Solid earnings reports and stable revenue guidance further bolster market confidence.

In this context, Bitcoin’s short-term alignment with U.S. equities reinforces bullish support, but from a price formation perspective, institutional inflows and market leverage structures are the more direct drivers.

Institutional Accumulation and Leverage Support Bitcoin

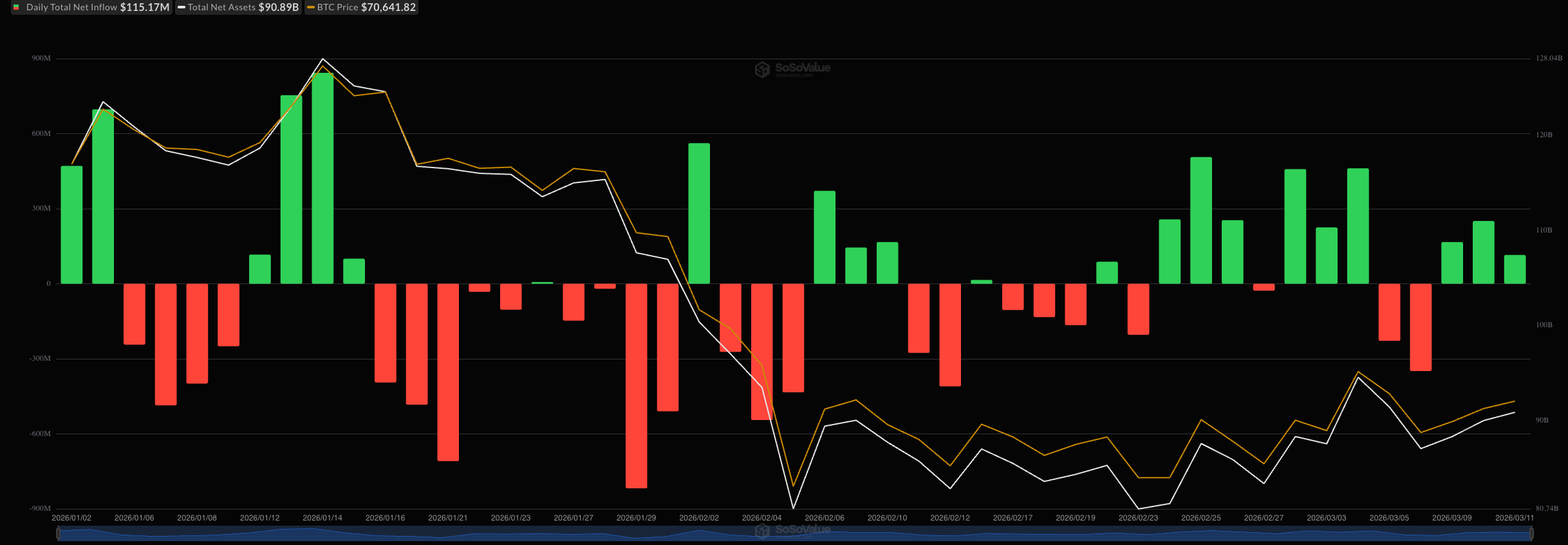

In early March, major corporate holder Strategy added 17,994 BTC at an average price of around $70,900. According to SoSoValue, spot Bitcoin ETFs have seen three consecutive weeks of net inflows following the year-start pullback, providing additional price support. In other words, large-scale institutional moves are driven by long-term allocation strategies rather than short-term macro factors.

Compared with traditional assets like gold and U.S. equities, Bitcoin’s price is more directly influenced by the leverage and positioning of futures and perpetual contracts.

Since peaking above $97,900 earlier this year, Bitcoin has been consolidating between $63,000 and $72,000. This consolidation is not solely a product of macro sentiment but a result of interplay between historical resistance above and institutional and long-term holder support below, highlighting Bitcoin’s price dynamics as an internal market game largely independent of traditional assets.

Is Bitcoin’s Uptrend Restarting? Market Cautiously Optimistic

Overall, Bitcoin’s current price action aligns more with a high-risk asset. Yet, with deeper institutional positioning, growing corporate balance sheet holdings, and increasing attention from governments, Bitcoin is gradually taking on a third role—an asset that neither fully depends on economic growth nor solely functions as a safe haven.

From a short-term technical perspective, a successful breakout above the $70,000–$72,000 range could open the way toward $79,400, expanding upside potential. Conversely, failure to break out may lead to renewed consolidation, with support likely near $65,800 and $63,000.

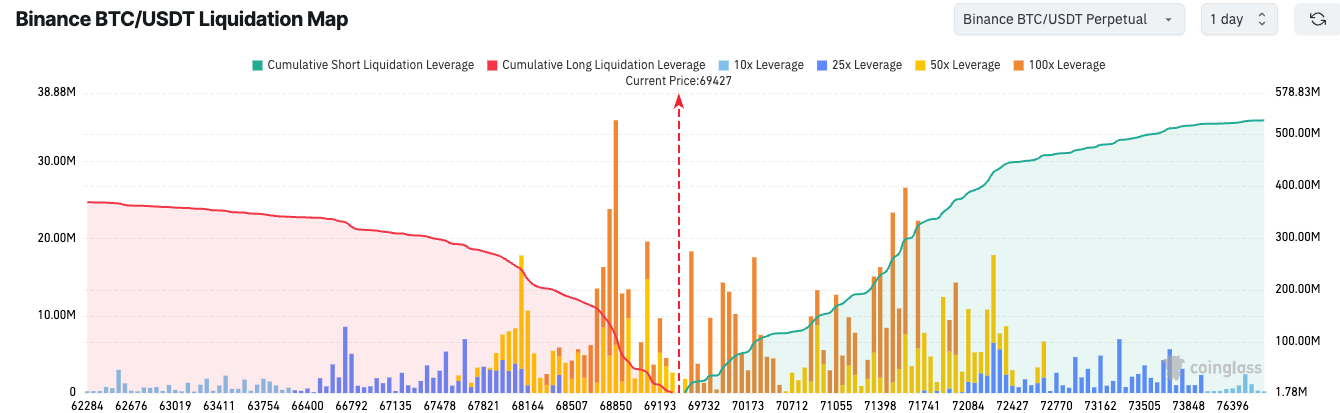

Coinglass data on Binance BTC/USDT liquidation map shows a relatively balanced battle between bulls and bears around $70,000. As the price extends toward both extremes, the upper-side short liquidation leverage exceeds lower-side long leverage, indicating limited near-term selling pressure and supporting cautious optimism in the market.

Watching Bitcoin’s Key Risks

In the medium to long term, as long as institutional and long-term capital continues flowing in, the current consolidation is more likely a structural accumulation rather than a trend reversal. Scarcity on the supply side persists, and clearer global crypto regulatory frameworks further support continued institutional participation.

However, three key risks remain:

- Ongoing miner selling: Over the past 30 days, miner addresses have net sold 123,000 BTC, the highest in six months. Losses from mining could trigger forced selling, adding pressure to the market;

- Geopolitical volatility: Any escalation in the Middle East could still disrupt risk asset liquidity;

- Regulatory setbacks: Delays in U.S. crypto legislation could reignite market uncertainty.

Given current price levels and macro conditions, traders are likely to favor range-bound strategies in the short term. Proper position management remains critical in such a highly volatile market.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.