- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- Монгол хэл

April 2026 BoE Preview: The Old Lady Set To Stay On Hold

Summary

- Policy On Hold: Bank rate is set to be maintained at 3.75%, likely via a unanimous 9-0 vote

- Familiar Guidance: The MPC will again stress a desire to 'act as necessary' to return inflation to target over the medium-term, though again shan't provide an explicit bias as to the next policy move

- Forecasts In Focus: Updated projections are likely to point to higher near-term inflation, coupled with a higher peak in unemployment, and a slower pace of economic growth

Standing Pat On Policy

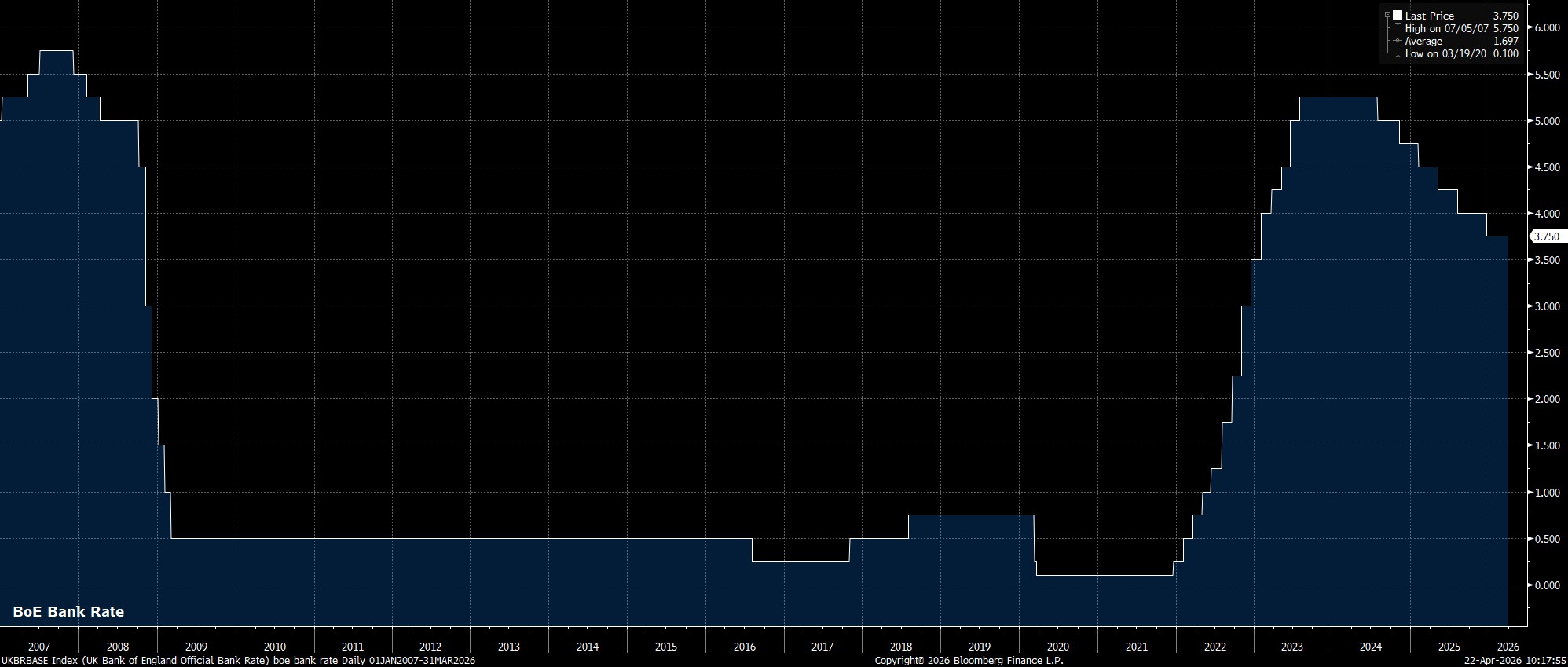

As noted, the MPC are set to stand pat at the April confab, holding Bank Rate steady at 3.75%, extending a pause which begun at the turn of the year, with policymakers having last delivered a 25bp cut at the final meeting of 2025.

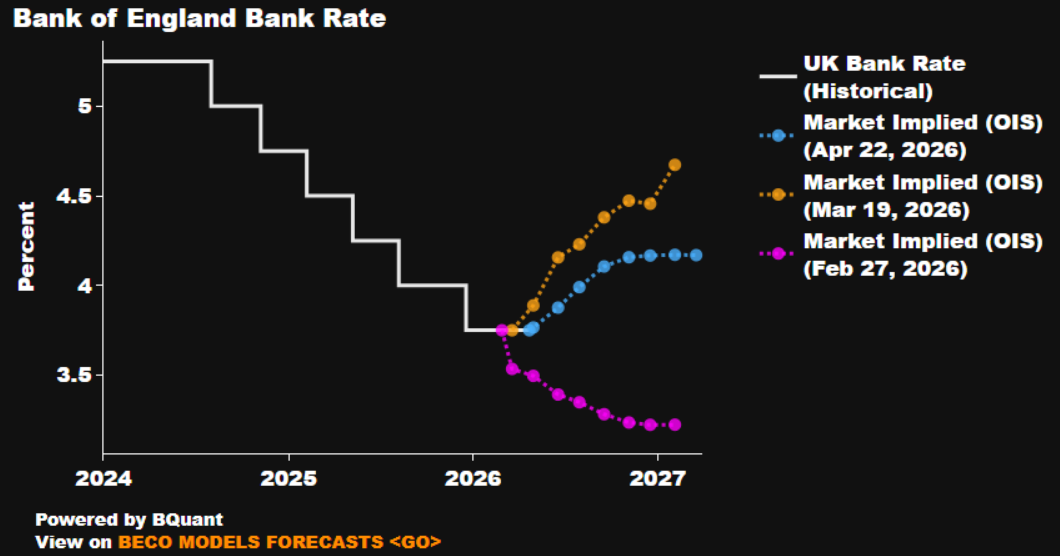

Money markets, per the GBP OIS curve, discount essentially no chance of any action this time out, though continue to foresee a gradual pace of tightening as 2026 progresses, with a 25bp hike fully discounted by July, and swaps also foreseeing around a 2-in-3 chance of a second such hike being delivered by year-end. This pricing, incidentally, has stuck, despite numerous comments from Governor Bailey in recent weeks, indicating that markets are getting ‘ahead of themselves’ with such a hawkish curve.

Committee Likely To Remain Unanimous

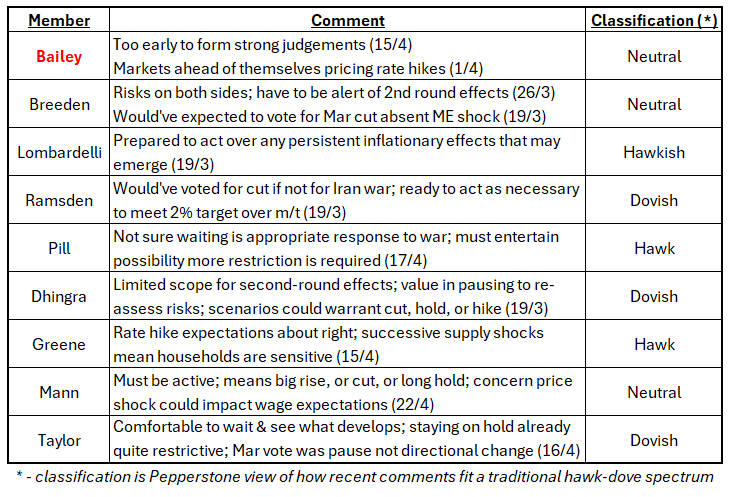

Turning to the vote split, the March meeting saw the MPC vote unanimously in favour of a policy decision, namely to hold Bank Rate steady, for the first time since all the way back in September 2021.

This time around, another unanimous decision seems likely, judging by recent comments from MPC members, as detailed in the table below. In fact, it’s noteworthy that we have heard considerably more from ratesetters in the period since the March meeting, than we did in the run-up to it, perhaps a sign that the MPC have learnt their lesson in that one of the main reasons for such a violent market reaction last month was that participants had had little-to-no indication of how policymakers were viewing the outlook in advance of the surprisingly hawkish policy statement being released.

In any case, for the April meeting, it seems unlikely that any of the MPC’s more dovish members have yet obtained sufficient data to swing back in favour of voting for rate reductions, given that both the magnitude, and duration, of the inflationary shock triggered by higher energy prices remains largely unknown.

In fact, the real question is whether the MPC’s hawks, namely Chief Economist Pill and external member Greene, are ready to vote for a rate hike at the current juncture, with both having made notably hawkish remarks in recent weeks. While, in my view, it is unlikely that recent developments would push either to ‘pull the trigger’ on policy tightening at the current juncture, particularly with both crude and natural gas futures some way off recent highs, comments from both in the accompanying meeting minutes will be worth parsing closely, to judge whether either may vote for such action in the coming months.

Policy Guidance To Be Maintained

Mercifully, the accompanying policy guidance is likely to be a somewhat more straightforward affair.

As such, the MPC are likely to repeat their preparedness to ‘act as necessary’ to ensure that inflation returns to target over the medium-term, while also repeating that CPI is likely to be higher in the ‘near-term’ as a result of conflict in the Middle East. It will, however, be interesting as to whether the MPC repeat their prior stance of being ‘alert to the increased risk of…second-round effects’, particularly given that the potential for said effects seems relatively remote for the time being.

In any case, it seems highly unlikely that the statement would adopt an explicitly more hawkish tone than that seen last time out, with policymakers again likely to omit any particular bias as to the next move in Bank Rate.

Forecasts In Focus

Meanwhile, the Bank’s updated economic forecasts will also be in focus, particularly considering that the prior round, produced in February, are now incredibly stale.

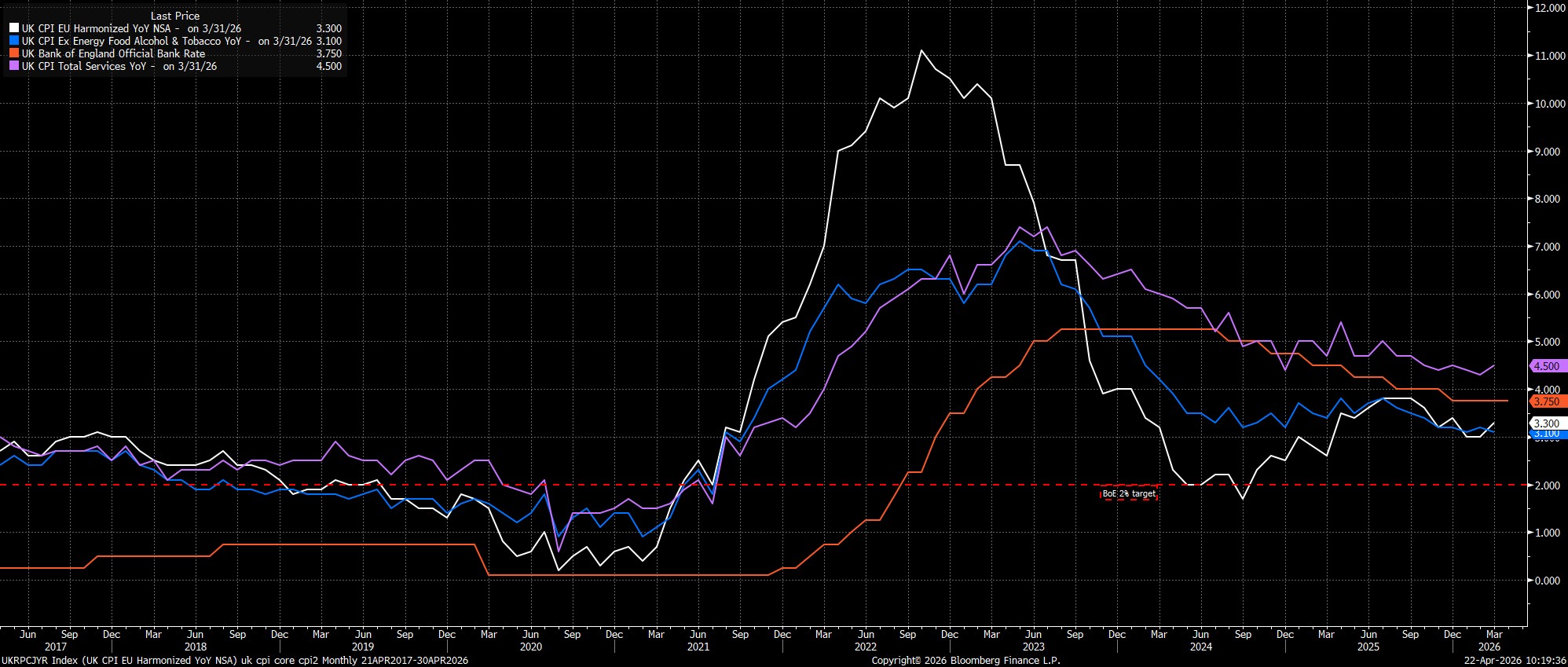

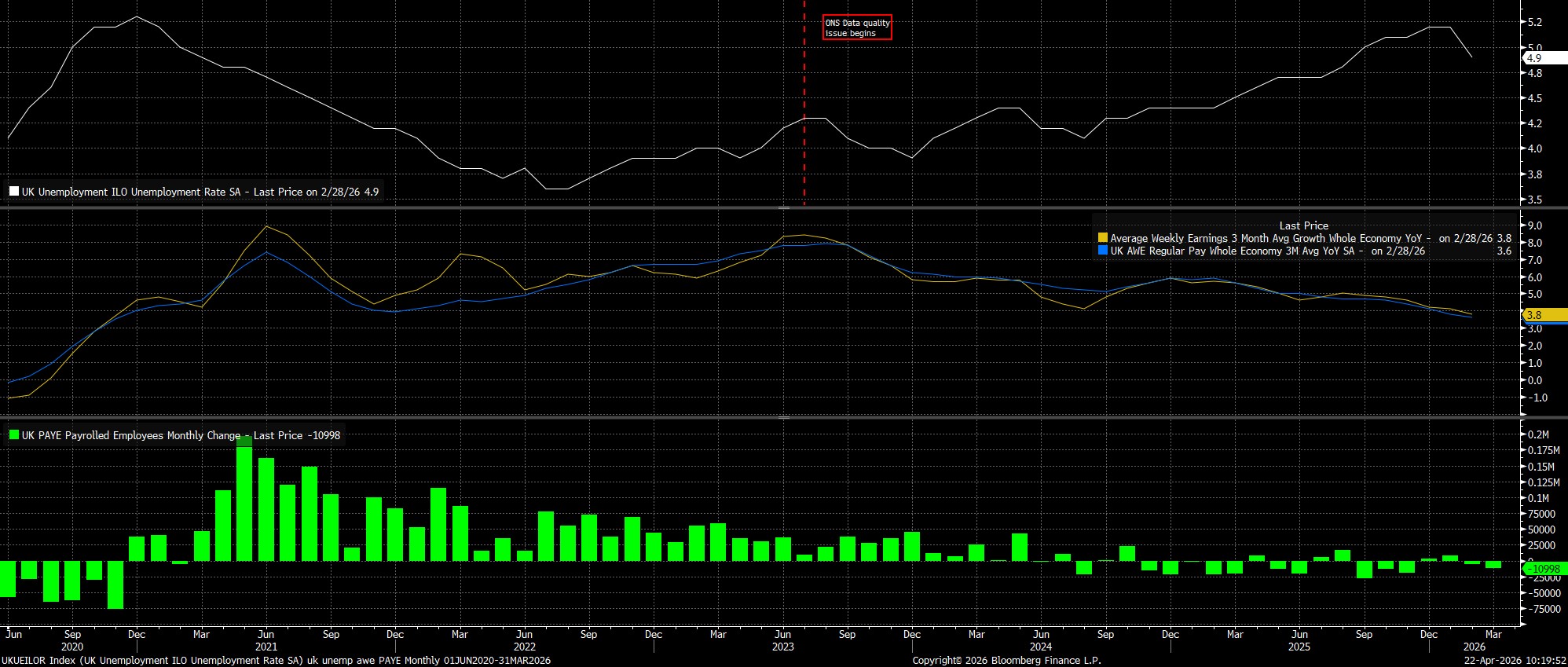

On the inflation front, headline CPI rose 3.3% YoY in February, roughly in line with the MPC’s expectations for a print ‘close to’ 3.5% YoY, though a further increase in headline inflation is likely in the months ahead, particularly in the summer, once Ofgem’s consumer price cap rises to account for the recent increase in energy prices. The key focus for market participants will not only be how high the Bank expect inflation to peak, likely just shy of 4% later this year, but also the length of time it will take for CPI to return to the 2% target, which in turn will inform the appropriate policy response.

It is overwhelming unlikely that any second-round inflation effects emerge, at this stage, given not only that inflation expectations remain well-anchored, but also that a greater margin of labour market slack continues to emerge.

On that note, the ‘Old Lady’ is likely to upwardly revise its prior expectation for unemployment to peak ‘around 5.25%’ in the second half of the year, reflecting the lacklustre nature of labour demand, which will only be worsened by the increasingly uncertain economic outlook, as well as both the increased cost of, and risk associated with, hiring, by virtue of various government policy changes.

Altogether, this is likely to result in at least a near-term downgrade to GDP growth expectations, reflecting the negative demand shock that higher commodity prices will ultimately cause.

Bailey To Repeat Recent Rhetoric

As for the post-meeting press conference, Governor Bailey is likely to, by and large, repeat his recent comments, in that it is ‘too early’ for the Bank to be making any concrete judgements as to the economic impact of developments in the Middle East. Bailey is also highly unlikely to endorse the present market path of rate hikes over the remainder of the year, and may even again offer explicit pushback on the idea of policy tightening, as markets continue to get rather over-excitable on that front.

Conclusion

Wrapping up, the MPC will likely continue to ‘play for time’ at the April meeting, seeking further clarity on the economic outlook, and seeking not to pre-commit to any policy action at this stage, with the current policy stance already restrictive.

Considering that the inflationary impulse from energy prices is likely to be a short-lived ‘hump’, which carries limited risks of proving persistent, there remains a path to one, or even two, rate reductions still being delivered in the second half of the year, potentially allowing the MPC to lean against the negative demand shock, as and when policymakers obtain sufficient confidence that higher headline inflation will indeed prove to be limited and temporary in nature.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.