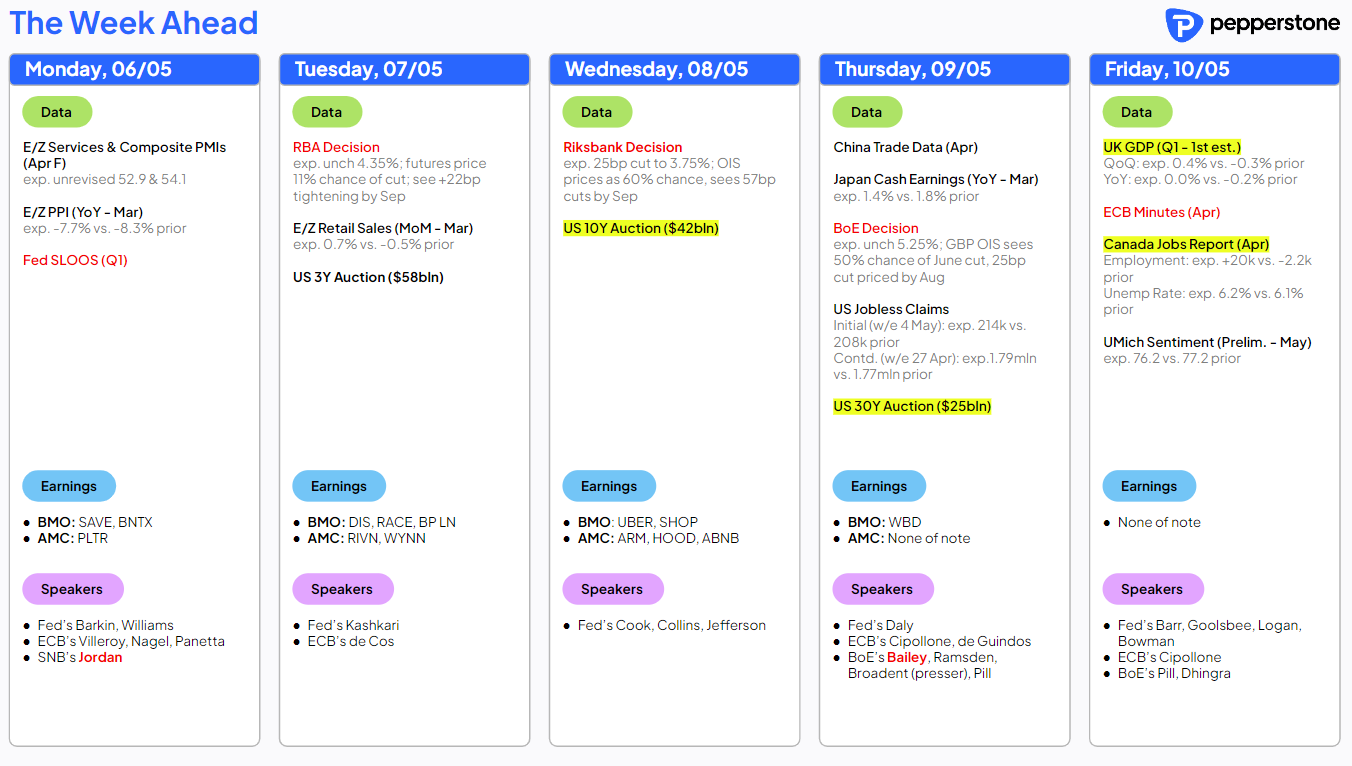

A Traders’ Week Ahead Playbook: The tables on risk have turned

Yet, despite these landmines, a gentle calm descends over financial markets – early last week the USD was threatening to trend higher, but now momentum shifts to the downside, with US Treasuries finding better buyers, US interest rate markets pricing close to two cuts by year-end, while the VIX index has pulled back to 13.5%, with the S&P500 closing above the 29 April high.

By way of significant movers - aside from a lazy 25% w/w fall in Cocoa and a 32% w/w gain in Nat Gas – where NG needs to be on the radar given the breakout and the growing potential for a bullish trend to materialise, we see solid movement in the HK50 (closing 6.9% wow), while Bitcoin has rallied 10% off its lows and is eyeing a move back to the 50-day MA at 65,890. In FX, CADJPY saw the biggest 5-day percentage change, falling 3.6% w/w.

The MAG7 equity names look to have regained their mojo, amid solid earnings and some lofty guidance for capex - suggesting growth and innovation remain at the core of their investment thesis, backed by renewed buybacks and some big names even rolling out dividends. China tech is also flying higher, where both Tencent and Alibaba have run hard of late and while overbought should be well supported into weakness.

How the tables have turned, and the reassuring view from Fed Chair Jay Powell that policy is still “sufficiently restrictive” and “it’s unlikely the next policy move will be a hike” has reinvigorated the risk bulls. Add in a weaker US ISM services print and a moderation in US nonfarm payrolls (NFP) and the market has gained greater confidence that the US economy is not indeed overheating. Conviction levels may still be low, but the platform is in place for risky assets to move higher this week, notably if truce talks in Gaza gain real traction.

Looking ahead and the landmines through which we navigate positions:

US data is thin on the ground this coming week, with the senior loan officer survey on bank lending practices really the only economic event risk to be concerned with – traders can trade the KRE ETF (US Regional bank ETF) here and react to markets interpretation of the survey. We also get 11 speeches from Fed members, but until we get the US (April) CPI report on 15 May, I suspect traders will not be too concerned with holding risk over their respective views.

It will be a lively week at a central bank level, with the RBA (on hold), BoE (on hold), Swedish Riksbank (skewed to cut), Banxico (cut) and Brazilian Central Bank (50bp cut) all meeting.

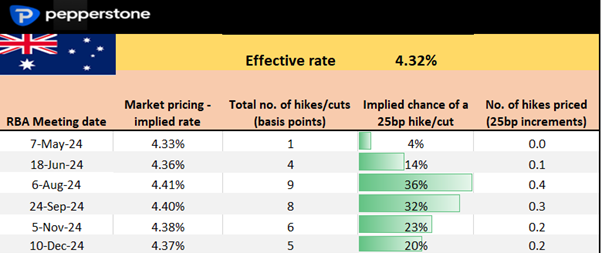

We should get a 25bp cut in Mexico, with a 50bp cut expected to the Brazilian Selic rate. The RBA meeting and Statement on Monetary policy will get big focus, and while the RBA will almost certainly keep rates at 4.35%, and continue to suggest “the board is not ruling anything in or out”, Aussie swaps price a near 40% chance of a hike by August (see pricing below), so many are expecting a modest shift in their commentary and a clearer roadmap to future hikes – if we don’t see that play out in the wording then we could see the AUD trade lower, notably vs the FX cross rates.

The GBP navigates Thursday’s BoE meeting, with the broad consensus expecting a dovish split in the voting and a statement that justifies the view priced into interest rate pricing, where the BoE is expected to embark on its first cut in August. We also get UK Q1 GDP, a speech by BoE Chief Economist Huw Pill and 1-year inflation expectations from the DMP (Decision Makers Panel), and that could be looked at by some in the market. GBPJPY and GBPAUD shorts, EURGBP longs, were the preferred plays last week, and I still favour these staying in these positions.

Wednesday’s Riksbank meeting puts the SEK (Swedish krona) firmly in play, with economists split on whether we see the Swedish central bank join the Swiss National Bank in starting its easing cycle. The SEK swaps market implies a 25bp cut at around 80% probability, so those holding SEK short positions will have some concern with that position over this event. The risk-to-reward trade-off favours short NOKSEK over the meeting, but a 25bp cut is a lineball call and as many will attest to, trading over news like this is more of an exercise in risk management, or for those running tactical or special situation strategies.

We also see inflation prints in Mexico, Norway, Columbia, Chile, Brazil, and China. Trade data (Thursday – no set time) from China will also get a focus, with imports expected to increase by 4%.

In Japan, I guess kudos go to the MoF/BoJ - they hit JPY shorts hard with two bouts on size intervention and as luck would have it, they’ve been given a helping hand from Jay Powell and the first below estimate NFP print since October 2023. Those using the JPY to fund a saturated carry position will almost certainly think twice about using the JPY tactically here in the near term, and until we see a better trend in the US data, or if we see a hotter US CPI print, USDJPY has scope for ¥150. Conversely, on the week, I’d be expecting the upside to be capped at ¥155 and would be selling rallies into ¥155.50.

As always, an open mind to market movement (as price will always go to where it wants to go), and a dynamic approach to react will serve you well in this market.

*24-hour US share trading – Announcing that Pepperstone recently launched 24-hour share CFD trading – a concept that allows clients the ability to trade the marquee US equities at any time of the day. When market-moving news break traders can capture the opportunity, or dynamically react and efficiently manage risk in the portfolio. Reach out for more information on the launch.

Aussie swaps pricing – we see little priced for this week’s RBA meeting, with a 1/3 chance of a 25bp hike for August.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.