- English (UK)

- English (UK)

We also saw German April net employment change gain a huge 373,000, while in the US, we saw US jobless claims at 3.83m (consensus 3.5m) and that re-focuses us on next week’s NFP, which is expected to show some 22m jobs lost in April (economist range of -30m to -840k), with the U/E rate rising to 16%.

The Fed announced an increase of its Main Street Lending program, initially set-up to support small to mid-sized businesses - we are yet to hear of a start date. However, the highlight of EU/US session was the ECB meeting, although it caused little fanfare and it wasn’t until a few hours later that we saw EURUSD moving higher from 1.0840 into 1.0972, with gains across the EUR crosses. We have to question how much of the move in FX was month-end related, especially when we see the Italian/German bund 10yr spread widen 9.8bp (typically a EUR negative).

We did see a new facility, called the Pandemic Emergency Longer-term Refinancing Operations (PELTRO), which offers more favourable terms for the TLTRO program and provides cheap rates for banks to get liquidity. But there was no increase to the PEPP program, which is what the market was sensitive too. Christine Lagarde, didn’t give away too much other than the ECB will hold a flexible approach and did her best not to upset the market – she detailed her ECB staff model a scenario where EU 2020 GDP could fall between 5% and 12%, which is a decent spread - the market consensus is -5.3%, with a range of -1.1% and -13%.

Maybe it was the whole month-end malaise, or maybe they just need to hear something new and impactful, and that we’re ultimately seeing buying fatigue. However, European equities weren’t overly pleased, with the DAX closing -2.2% and the EU Stoxx 50 -2.3% on decent volumes. The FTSE 100 fell 3.5% on volume 23% above the 30-day average, but again it was month-end.

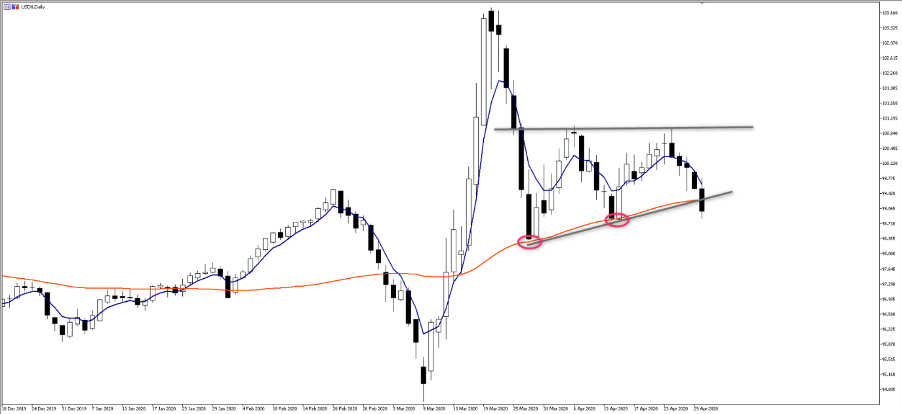

EURUSD pushed up 0.7%, taking the USDX through the 55-day MA and trend support. One to watch.

As I mentioned in the USD report sent on Wednesday, I can’t see a collapse in the USD and the fact EURUSD 1-week implied vol has dropped 0.56 vols on the day to stand at 6.32% tells me the market isn’t expecting a rapid move either, with 1-week put vol trading a modest premium to calls. See the volatility matrix below.

EURAUD moved just shy of the 200-day MA, which was the level I had been eyeing, and I moved to the sidelines on this idea. We’ve seen good buying in GBPUSD, with the pair finding the 200-day (1.2654) a tough nut to crack, and we see a double-top in the making – a break of the 14 April high mitigates that. GBPAUD has had a solid counter-trend short-covering rally, and has garnered good flow across the desk – can it continue? I guess equities will hold that answer, although I thought it of interest that the RBA bought no bonds yesterday as part of its QE program – when we talk about central bank divergence driving currencies, perhaps this is something driving the AUD of late.

AUD will, therefore, have its eyes on Asian equity markets today, and with the S&P 500 closing -0.9% (closing out the best monthly gain since 1987) and the Russell -3.6% - we’ve seen the VIX +2.9 vols into 34.1%, so equity vol has pushed higher as we roll into May – with the question, will we see ‘sell in May and go away’? Or will risk continue its liquidity fuelled march and we genuinely can consider new highs in the NAS and S&P 500.

Certainly, aside from a monster climb in crude, leads are not great for Asian markets, with Aussie SPI futures -2%. We have an eye on US equity futures, which are falling away quite aggressively as I type – Apple has hit us with decent numbers, but when they increase the div and buyback but refrain from offering guidance (first time in a decade) it all looks a touch messy. Amazon is down 4.5% too, after a solid cash session and that is impacting.

One aspect that is worth following is the blame game. Trump and Pompeo have certainly stepped up the rhetoric in the past two days, with headlines this morning that “he’s seen evidence that Wuhan lab origin of the virus”. This marries with the Washington Post article which hasn’t moved markets, but when we consider US-China relations were frayed going into the crisis, and we know there’s an election that Trump needs to gain some ground in the polls, then this becomes a growing macro issue.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our online application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.