- English (UK)

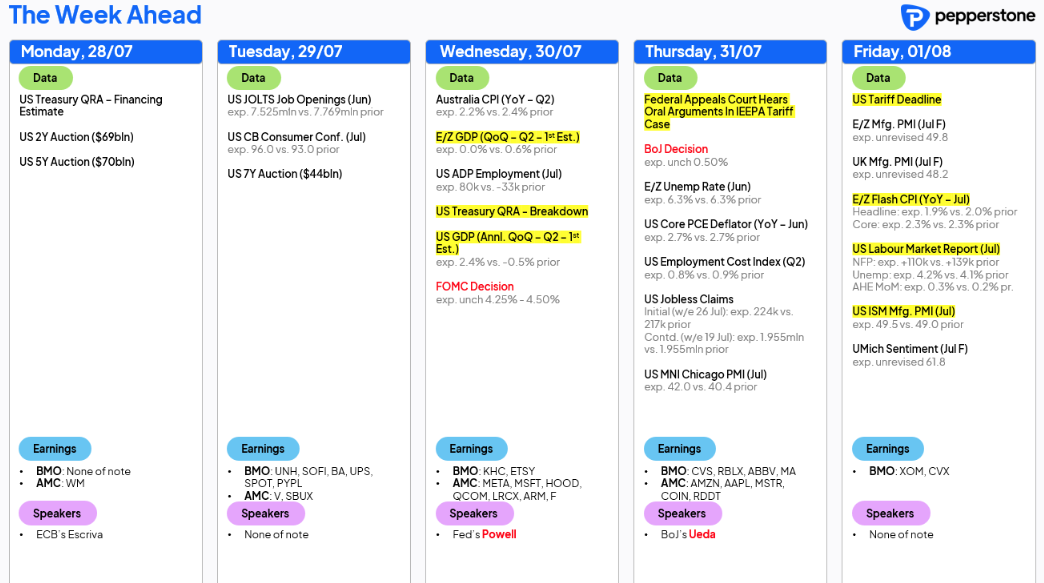

Markets on Alert: Fed Fractures, Tariff Progress, and the Big Jobs Report Loom

Tariff news set to come in heavy, but will it impact markets?

Tariff-related headlines seen through Sunday have been meaningful, with the US-China tariff pause being extended by a further 90 days, and the US-EU forging an agreement that follows a similar model to that of last week's US-Japan deal. EU exporters will now face a 15% tariff rate to its US buyers, a far more friendly rate than the 30% rate they were facing – in exchange, the EU has committed to purchasing $750b in US energy products and some $600b in other investments.

The news flow from both the extension with China and the agreement with the EU is clearly market-friendly, and should put further upside potential into the EUR, where the single currency is already finding the love from FX players, and should also put renewed upside into EU equities.

Importantly, for those nations still looking to achieve a last-minute floor tariff rate (on US exports) of 15%, it’s all too clear from the case studies with Indonesia and Japan is that the most important factor is committing to massive levels of investment spend. Trump will now sell this hard to the US voters as a huge win for the US - so expect Trump to address the nation in a presser shortly.

A lasting US-China deal remains a more complex issue, and while trade imbalances remain a major consideration, at the heart of any potential full agreement, we’re likely going to see a commitment from China to massive investment spending.

China/HK equity leading the gains through July

For the China market watchers, the 24-member Politburo will gather to formulate plans for the balance of 2025. Market expectations for any new impactful policy initiatives are low, and the Chinese authorities will be quietly content to maintain the status quo, perhaps massaging around the edges, with its growth metrics tracking above its policy objectives. China and HK equity markets have been the star performers in July, so perhaps policymakers will see that as the market voting on increased confidence in China’s economic trajectory.

Central banks in focus this week

We navigate G10 central bank meetings in the US (hold), Canada (hold) and Japan (hold), as well as in the LATAM/EM space, with policy decisions in South Africa (25bp cut expected), Chile (25bp cut expected), Columbia (25bp cut expected), and Brazil (no change).

Dissent within the Fed’s ranks

While the BoJ meeting could be quite informative for JPY & NKY225 traders, it will likely be the FOMC meeting on Wednesday that gets the headlines, even if this is shaping up to be a low-impact event for US markets. Expect dissent from Chris Waller and Michelle Bowman, who should both vote for a 25bp cut at this meeting - a symbolic development, as the once galvanised and cohesive committee appears increasingly fractured and almost… dare I say it, politicised…

Dissent aside, Chair Powell will continue to guide that the board will take in the incoming data “over the summer” – with traders seeing a cut in the September FOMC meeting as more likely than not, the two nonfarm payrolls prints (31 July & 5 Sept) and two CPI prints (12 Aug & 11 Sept) that hit us in the lead up to the September FOMC meeting now take on additional significance.

A deluge of US and EU corporate earnings on the docket

It’s the big week of the US corporate earnings season, with 38% of the S&P500 market cap set to report numbers for the quarter – the lineup includes Apple, Meta, Amazon and Microsoft, but we also hear from some of the retail trader favoured names, including Coinbase and Roblox. Traders look for these names to build on what has been a solid Q2 earnings season so far, a factor which has offered increasing tailwinds to the grind higher and consecutive ATHs in the S&P500 and NAS100 seen resulted in levels of cross asset volatility crushed.

Running the numbers, we see that a third of S&P500 companies have now reported earnings, with around 40% raising guidance, an outcome that is well above the levels seen in the Q1 reporting season. 83% of S&P 500 companies have beaten analysts’ consensus expectations on EPS, with those beating doing so by an average of 6.9%.

It’s also a big week on the European corporate earnings calendar, with c20% of the Euro Stoxx companies set to report.

US nonfarm payrolls are the main event of the week

The flow of economic data also comes in hot, with the labour market getting close inspection. US nonfarm payrolls (NFP) is the main event risk of the week, with the market modelling a central case of 109k jobs created in July, with the range of estimates (from economists) seen between 170k and zero. The prospect of downward revisions to the prior two NFP prints is high, but likely a secondary consideration for rates and FX traders. The unemployment rate is expected to tick up to 4.2%, with the average hourly earnings metric eyed at 3.8% (from 3.7%).

US interest rate swaps imply a 25bp cut in the September FOMC meeting at 64% probability – a sub-100k NFP, with prior NFP prints revised lower and a 4.2% U/E would probably be enough to see swaps pricing move towards 70% implied for a cut in September. The USD will take its direction from the US 2-year Treasury yield, which is most impacted by changes in Fed rate cut expectations. The S&P500 and NAS100 will be content to see payrolls coming in around 100-120k, as the combination of reasonable job growth and increased Fed cut expectations would feed the goldilocks investment backdrop.

While the NFP report takes centre stage, staying Stateside, traders also navigate the US JOLTS (job openings) report, weekly jobless claims and the Q2 employment cost index. The US Q2 GDP print and ISM manufacturing report may also get some attention.

Australia Q2 CPI set to guide expectations for a cut in August

In Australia, Q2 trimmed mean CPI (due on Wednesday) is expected to come in at 0.7% q/q / 2.7%, which if realised would continue to portray a moderation in price pressures – however, that outcome would also be a touch above the RBA’s own central forecast of 2.6% y/y, and while Aussie interest rate swaps once again price a 25bp cut on 12 August as a done deal, it feels as though we'd need to see a trimmed mean print at or above 3% to derail a cut in the markets eyes.

In Europe, the preliminary July CPI release (due on Friday) may be one to keep an eye on for those holding EUR exposures - after the ECB last week suggested the bar to cut rates again in the near-term has been sufficiently raised, we’d likely need to see a strong downside surprise to the consensus call of 1.9% y/y to see the September ECB as a live event in the markets thinking.

Good luck to all.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.