- English (UK)

- English (UK)

I could have dedicated a full note writing about the GBP, as vols (i.e. the risk premium) have picked up and it’s another week of debating the UKs Internal Markets Bill (starting today). Which has raised, but not ruined the risk of a full no-deal Brexit again. I could have focused on the US election, as the market has hedged much of the late October or early November risk. Whether I’m looking at rates, FX or equity implied volatility the market is positioned for great movement and I question if the extent of the vol becomes reality. The idea that we may not get a full result for days, if not weeks, given the level of postal voting is the real talking points. Not to mention how ugly scenes could get if the results are contested.

We have Quadruple Witching on Friday, which can often lead to some shenanigans in markets. This is when there is much focus on the multi-year megaphone pattern and the 55-day MA holding up play of the US500. We have the LDP party election in Japan today, where Chief Cabinet Secretary Yoshihide Suga looks to replace Abe, but shouldn’t cause too many wobbles in the JPN225 the JPY. While in Oz we get the August jobs report on Thursday, with 40k jobs expected to be lost (the u/e rate eyed at 7.7% from 7.5%). US-China relations are also there given the deadline for merger talks with TikTok end tomorrow. All at the backdrop of China’s industrial production, retail sales, and fixed-asset investment (tomorrow 12:00 AEST).

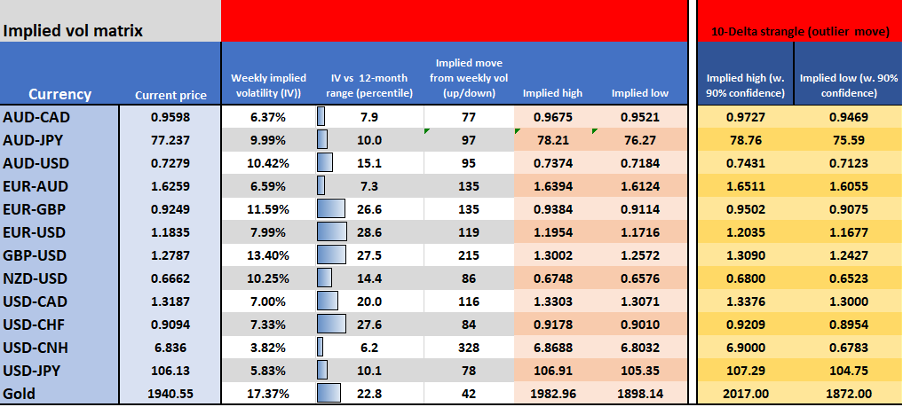

Implied volatility matrix (Friday’s closing levels). We can look at the options market and assess the extent of the movement expected and portray a range, with a corresponding degree of statistical confidence.

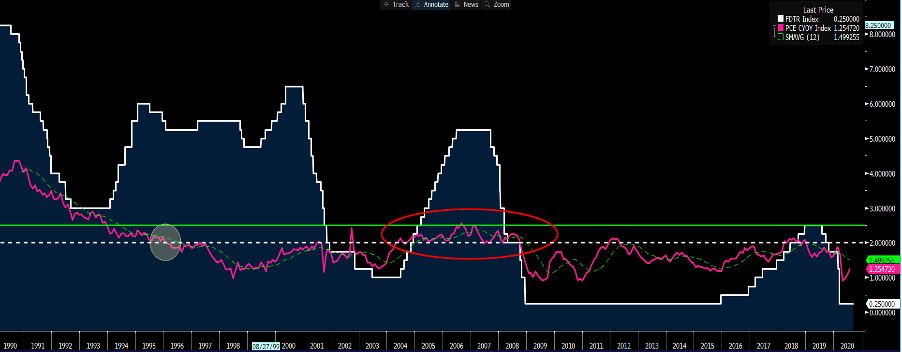

This is the playbook portrayed onto the USDJPY chart. As a picture tells a far clearer understanding for our risk and for those into mean reversion. An unashamed plug I have started putting up ideas on Trading View, so do follow me and share the banter.

Why this FOMC meeting could see significant volatility in markets

Two weeks ago, the Federal Reserve moved to a new monetary policy regime called ‘Average Inflation Targeting’ (AIT).

The aim of this is to proactively push inflation (in the US) above its long-held target of 2%. When above this threshold, inflation would then be tolerated on a sustained basis.

This is widely different from years gone by when the Fed would signal rate hikes were coming well before inflation hit 2%.

So, the Fed’s reaction function has essentially changed, which means they will be far slower to hike. Even well into the future when the economy is growing above trend and the labour market is strong.

(White - the fed funds rate, pink - core inflation)

(Source: Bloomberg)

The Fed moving to AIT and letting the economy run hot is absolutely the right policy. But, if the Fed’s going to drive inflation to 2%, aside from base effects, we need to know how on earth they’re going to do this.

That’s why this Wednesday’s (Thursday 4am AEST) FOMC meeting is so undeniably critical. There could be fireworks in the market, even if vols don’t reflect it.

Consider that aside from a brief period in 2006/07, the Fed is going to execute on something they have simply failed to do since 1995.

This is an institution that has failed miserably to meet its inflation forecasts time and time again.

It’s easy to be cynical, but if the Fed is to be seen as credible, gaining the market's respect is key above all else. So, we want answers and they need to come next week. Waiting just won't cut it.

So how do they do it?

The Fed needs to change behaviours. They need to convince the public that prices are going up. This isn’t just by pumping up financial markets and making credit or loan repayments insanely cheap. The public needs to believe everyday items that feed into the inflation calculation are going up. By altering the perception of future prices, it manifests into actual inflation.

This is incredibly difficult, but it’s the only way. Inflation expectations breed inflation. By lifting inflation expectations and putting in measures to keep bond yields anchored, ‘real’ bond yields will move even deeper into the negative, the USD will weaken, and asset prices will push higher.

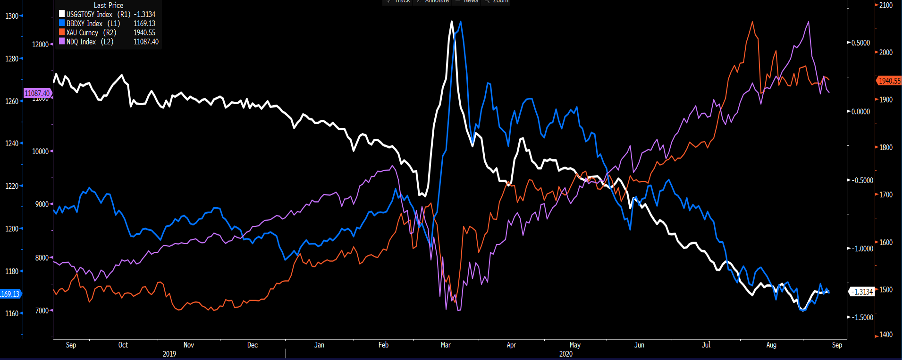

Correlation central - White – 5yr real Treasury yields, blue – USD, purple – NAS100, orange – gold)

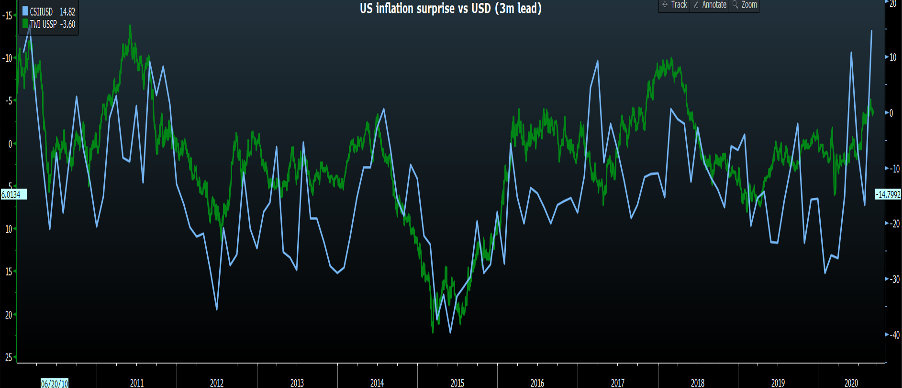

A weaker USD is critical in driving higher inflation. Although a one-way move in the USD will increase talk of currency wars and a race to the bottom, which is why gold is so attractive in this environment.

Green – trade-weighted USD (YoY % chance – inverted), blue – US inflation surprise index

The Fed would dearly like more stimulus at a fiscal level, but that’s out of their hands. But if they’re going to gain the credibility they crave from the market, they simply must go sooner and bring out the big guns.

If they get it right? We’ll see equities and gold trade higher, with real Treasury yields and the USD lower.

However, if they don’t offer us clarity, urgency and a clear plan, the market will take its pound of flesh and the USD will rally.

What’s your position?

If they’re going to do what they have failed to do for so many years, they simply need to make it happen next week and show the world they mean business. Credibility is everything.

Related articles

Ready to trade?

It's quick and easy to get started. Apply in minutes with our online application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.