- English (UK)

- English (UK)

BoE Playbook – Divided Decision As Hiking Cycle Draws To An End

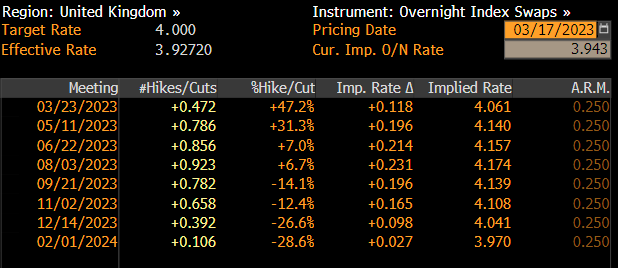

Consensus points towards a 25bps hike at Thursday’s meeting, and this is also where we lean; a decision which would take Bank Rate to 4.25%, the first time since mid-2008 that Bank Rate has eclipsed 4%. Although such a move is called for by the majority of the sell-side, markets view the meeting as much more of a coin-flip, pricing a roughly evens chance that the ‘Old Lady’ don’t pull the trigger on another hike.

Divided Decision

In any case, the decision is highly unlikely to be straightforward. Back in February, when the macro backdrop was significantly less uncertain than at present, the MPC already showed bitter divisions, with seven policymakers voting for a 50bps increase, while two of the more dovish members – Dhingra and Tenreyro – preferred leaving policy unchanged.

Said divisions are again likely to rear their head this week. Since the last meeting, not only have financial stability concerns risen amid the collapse of Silicon Valley Bank, and the bailout/forced merger saga engulfing Credit Suisse, but divisions on the MPC have also grown wider. While the dovish Tenreyro has been openly discussing how rates are too high, and she believes policy loosening may soon be prudent, the hawkish Catherine Mann has stated her desire to do more, rapidly, when it comes to raising rates. In the middle of this, the two most senior members of the MPC in terms of policymaking influence, Governor Bailey and Chief Economist Pill, have ‘sat on the fence’, and not yet taken a side in the debate.

Despite this, the balance of risks points toward a dovish revision to the BoE’s present guidance, which is already relatively woolly in stating only that “the MPC will adjust Bank Rate as necessary to return inflation to the 2% target”. As seen with the ECB last week, a dropping of this implicit tightening bias seems likely, meaning that the March hike will probably prove to be the last of the cycle. This is clearly what markets price, with no further rate increases priced beyond this month, and a slim chance of cuts priced into the back end of the year.

Macro Continues To Surprise

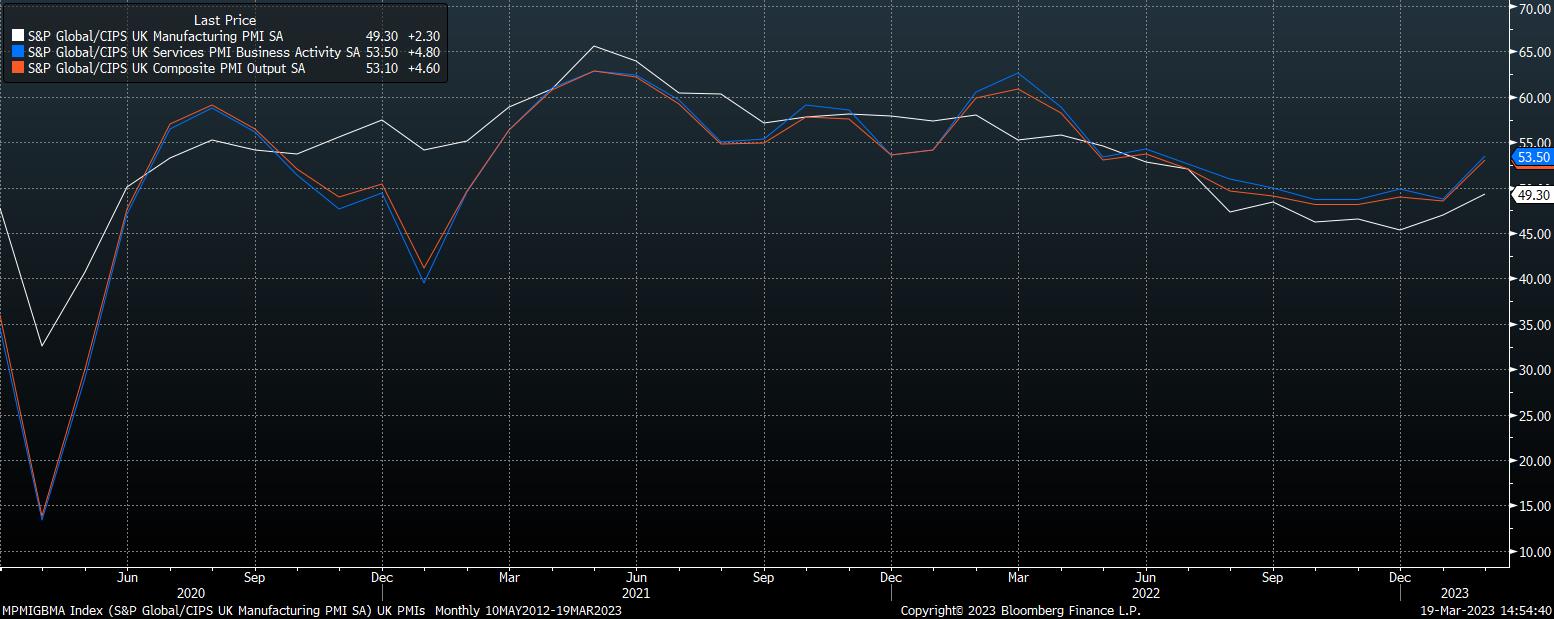

Although a continued dovish pivot is likely, the UK economy is, as surprising as it sounds, performing better than expected. GDP grew by 0.3% MoM in January, and the OBR has now pulled a forecasting U-turn and ditched their forecast of a recession taking place this year. Furthermore, the most recent PMI surveys also surprised to the upside, with output in the services sector rising at its fastest pace in 8 months, and a comparable gauge for the manufacturing industry hit a 9-month high.

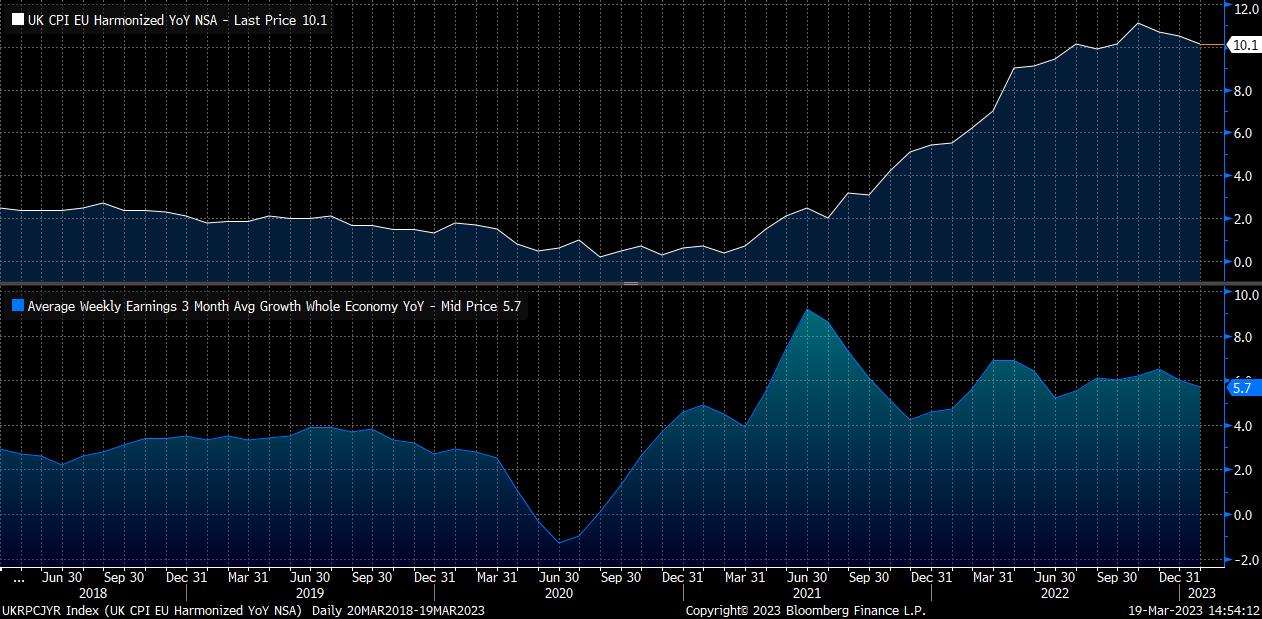

That said, inflation remains a significant issue, with CPI again printing north of 10% YoY in January, and expected to remain close to that mark in the February report, which is due a day before the BoE announce policy. Nevertheless, the continued decline in energy prices, coupled with the extension of the Government’s ‘Energy Price Guarantee’ for a further three months, should both ensure that the disinflationary process continues.

The labour market, however, does provide some cause for concern, with tightness persisting, and the unemployment rate remaining at 3.7% in the three months to January. Wage pressures, however, do appear to be abating, with regular pay growth having cooled to 6.5% YoY over the same period, and ongoing public sector wage negotiations appearing to be settled with increases that don’t run the risk of causing a wage-price spiral. This is likely to embolden the doves into pushing more aggressively for a pause after this meeting.

Market Outlook

Looking at the decision as a whole, particularly considering ongoing financial stability concerns in addition to the macroeconomic factors outlined above, the balance of risks appears to tilt towards a dovish surprise from the ‘Old Lady’. History, although not the best guide to future results, also supports this, given the Bank’s desire in recent times to avoid raising rates, or to stop hiking once a tightening cycle is underway.

With this in mind, risks stemming from the BoE appear to be tilted towards the downside for the pound; though, of course, one must also consider the impact of external factors and the ongoing fallout from concerns over the banking sectors’ health on the GBP.

_2023-03-19_14-53-04.jpg)

Through a purely technical lens, the bulls do have an element of control at present, with price having closed above the 50-day moving average on Friday, a level which has stiffly capped upside since the start of February. That said, the bulls arguably need a decisive break of the 1.22 handle to entice more longs into the market.

To the downside, initial support comes in the form of the aforementioned 50-DMA, with the 100-day moving average then lurking around a big figure below. Should losses continue, the 1.20 handle then comes into view, a level which has acted as something of a ‘tipping point’ in the tug-of-war between the bulls and the bears for some time now.

As for equities, the FTSE has had an incredibly poor time of things of late, not least due to the index’s 17% weighting towards financials. Nevertheless, and while the index’s sensitivity to BoE decisions has been rather low of late, it is notable how the index held above longstanding support at 7,300 last week, while also managing to reclaim the 200-day moving average in the process.

That now represents initial support, with resistance coming around 7600/25, a confluence of both the 100-day moving average, and the pre-pandemic high; how long ago that feels.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.