- English (UK)

- English (UK)

Analysis

Perhaps things had gone too far with NY Fed President John Williams stepping in on Friday and pushing back, detailing it was “premature” to think about rate cuts right now. In a world where communication with markets is critically important, these comments seem highly orchestrated and designed purely to stop financial conditions from getting too euphoric.

Fine, the market is convinced inflation is moving towards target in 2024, but the last thing any central bank want now is to destabilise inflation and growth expectations and see demand rise ahead of a cutting cycle, amid a renewed wealth effect. That would not be in the market script for 2024.

With US 2yr Treasury bond yields falling close to 30bp on the week, and DM rates rallying in a similar fashion – the USD falling 1.3%, and US growth expectations being revised higher (the Atlanta Fed Nowcast model has US Q4 GDP running at 2.61%), this is goldilocks at its finest.

The wash-up was the US500 gaining for 7 straight weeks, and we question if we can see an 8th. The US2000 gained an impressive 5.6% wow, with the NAS100 and US30 closing at ATHs. The ASX 200 even came onto the momentum radar, recording a weekly rise of 3.4%. It’s rare to see the Aussie equity market get such a working out from momentum accounts, but the index is in beast mode and recorded its second-best week of the year.

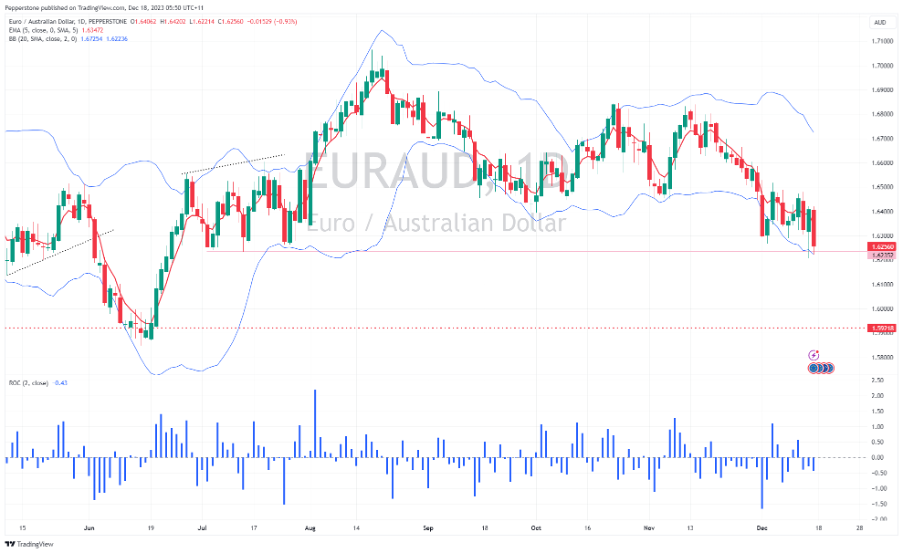

In the FX world, the NOK shone bright after the surprise 25bps hike from the Norges Bank, gaining 4.3% vs the USD - NOKSEK longs (or EURNOK shorts) look compelling, having printed a solid bullish outside week. With EUR PMIs reinforcing the headwinds faced in Europe, I am also skewed short of EURAUD, and while the RBA minutes this week should reinforce a relatively hawkish RBA, the AUD needs follow-through gains in Chinese equities.

As we look at the event risk this week, we see the BoJ meeting, US core PCE inflation and UK CPI as the big-ticket items for traders to navigate. On balance, unless the BoJ really surprises the market, it feels a stretch to see these derail the risk story in any great capacity - so the question will be whether traders start to close their books, reduce exposures and lock in returns. Or is there one last push left in risky assets?

John Williams’s comments have modestly dampened spirits and may be enough for a short-term reprieve to the bullish flow. We shall see.

Have the risk bulls had their fun for the year or is there one last hoorah?

Good luck to all.

The marquee event risks for the week ahead:

BoJ meeting (19 Dec – no set time) – after recent comments from BoJ Deputy Gov Himino that an exit from its ultra-loose policy can offer benefits to the economy, the market has formed a view the BoJ monetary policy could shift. Last week’s TANKAN report gave that call additional legs, with Japanese corps seeing inflation above the BoJ’s target of 2% in 5 years’ time for the 6th straight quarter. Despite recent moves in JPY assets, the market is not looking for a change in rates, and a move from negative interest rates at this meeting, although they could guide for change at the January meeting. That said, a surprise policy change – either to its rates setting or YCC - can’t be ruled out, so watch JPY and JPN225 exposures here.

RBA December minutes (19 Dec 11:30 AEDT) – after keeping rates on hold at the December meeting and refraining from altering the statement to any large degree the minutes shouldn’t trouble AUD traders too intently. Tactually biased short EURAUD for 1.5900/20.

EU (final) CPI (19 Dec 21:00 AEDT) – given this is a final print, and the market is not looking for a change in the previously reported headline CPI numbers from 2.4% yoy and core CPI yoy at 3.6%, this should be a low volatility event. It should, however, remind traders of the steep decline in EU inflationary pressures that reinforces an optimism of a March rate cut from the ECB.

China 1- & 5-year Prime Loan Rate (20 Dec 12:15 AEDT) – the market expected the prime rate to remain unchanged for the 1-year and 5-year rate at 3.45% and 4.2% respectively. While a cut to the prime rate seems a low risk, there are risks of a near-term cut to banks' reserve ratio requirements, although they are unlikely to come at this meeting.

UK CPI inflation (20 Dec 18:00 AEDT) – the market looks for UK headline CPI to print 0.1% mom / 4.3% yoy (from 4.6%), and core CPI at 5.6% (5.7%). The market prices a 20% chance that the BoE cut in the March BoE meeting, with a full 25bp priced for June. The UK CPI print could impact that pricing and by extension the GBP.

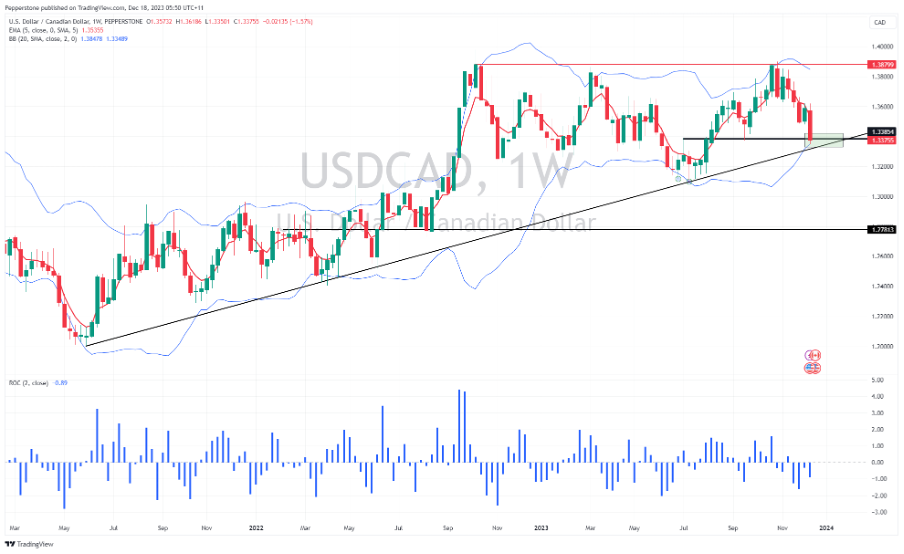

Canada CPI inflation (20 Dec 00:30 AEDT) – the market looks for headline CPI to come in at -0.2% mom / 2.8% yoy (from 3.1%), and core CPI at 3.3% (3.6%). The market prices a 72% chance of a cut from the BoC in March, so the CPI print could impact that pricing. USDCAD eyes support into 1.3325 – the rising trend drawn from the May 2021 low.

US consumer confidence (21 Dec 02:00 AEDT) – the median estimate is for an improvement in confidence with the index eyed at 104.0 (from 102.0). Upside in this data series could support risky assets.

Japan national CPI (22 Dec 10:30 AEDT) – the consensus is for headline inflation to moderate to 2.8% yoy (from 3.3%) and core CPI at 3.8% (4%). Unlikely a vol event for the JPY, but worth keeping an eye on if running JPY exposures over the data.

US core PCE inflation (23 Dec 00:30 AEDT) – after reviewing the recent US CPI and PPI prints, the market looks headline PCE inflation to come in at 0.00% mom / 2.8% yoy (from 3%), and core PCE at 0.2% mom / 3.3% yoy (3.5%). The trajectory of inflation is a key reason for the market pricing such an elevated risk of a March rate cut - so a below consensus print could solidify that call and weigh on the USD.

EM

Columbia central bank meeting (20 Dec 05:00 AEDT) – the consensus is for a 25bp cut to 13%, with risks of a hold. USDCOP looks heavy, so modest downside risk portrayed in the set-up with an out-of-consensus hold a potential trigger – a break below 3960 suggests new YTD lows.

Chile central bank meeting (20 Dec 08:00 AEDT) – the median call is the benchmark rate is cut by 75bp to 8.25% (from 9%) but given the recent inflation report, there is an elevated risk of a smaller 50bp cut to 8.5%. USDCLP needs a catalyst as the market seems happy to range trade this pair between 890 to 860.

Mexico bi-weekly CPI (21 Dec 23:00 AEDT) – the market eyes 4.36% yoy (from 4.33%). USDMXN tracks a range of 17.57 to 17.05 – and needs a catalyst to promote a momentum move.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.