- English (UK)

- English (UK)

Analysis

- A 30th all-time high for the S&P500 in 2024

- Placing a reason for the rally

- Tech and discretionary names leading the charge

- Asia equity opening calls looking constructive

- EUR and SEK lead us higher in FX

- Risks for the session ahead

After seeing a handful of red flags last week that suggested defence was the tactical approach to take this week, US equity indices have put on a show, with cash volumes 9% above the 30-day average, and for those that bought into the index move, they’ve been treated to the 30th new all-time high in the S&P500 in 2024.

The intraday tape has been upbeat, with the S&P500 cash opening near its lows, with buying pressure seen through the meat of the session to print a new high of 5488.5, before consolidating into the close.

Some have questioned the upbeat move, and why we have seen such bullish price action, while others have just gone about their business reacting to the trends. And, finding one smoking gun to point to is tough and unlikely offers any real edge to traders anyhow.

One factor that is getting some airtime is that US corporates have priced up $21.025b in corporate debt issuance this week – a decent clip, and while perhaps lower than originally estimated, it does suggest these firms have confidence in the market environment to get this issuance away.

One could also argue we’ve seen a slight settling of nerves around the French election which has offered the bulls a platform to progress. It's becoming clear that a hung parliament is the market’s base case, and calmer heads would argue that any government that does involve Le Pen’s RN party is unlikely to rock the fiscal boat too intently. Le Pen has a Presidential election to win in 2027, and that can only happen if the party win the respect of the bond market. The CAC40, for example, closed 0.9%, and we can see EURUSD rising to 1.0738, with EURUSD 1-month options implied volatility falling from 8% to 7.2%.

It’s also at times like this that we revisit the notion that it’s flow that really drives the market – whether this is down to retail investors dumping cash into stocks (as has been reported), dealer activity ahead of options expiry (OPEX) on Friday, as well as systematic players chasing the move higher, these flows are opaque but incredibly influential. This is why a healthy respect for price action, which incorporates all trading and investor activity, will serve short-term traders well.

Sector-wise, consumer discretionary has led the charge, where Tesla has been the talisman (+5.3%), with traders getting somewhat excited about Musk’s tweet that he is “Working on the Tesla Master Plan 4”. In tech, Nvidia has failed to follow through, but Apple pushed to a new closing high, and Microsoft, QCOM and Broadcom also continue to look beautiful on the dailies. Industrials have also worked well, while we see REITS, Health care and utilities at the bottom of the pile.

We’ve seen good selling in US Treasuries, with yields higher by 6bp across the curve and perhaps the equity market sees that as a bullish sign on US economics, but it certainly hasn’t weighed on risk. The lift in US yields hasn’t supported the USD either, and the flow in equity markets, and tightening in corporate credit spreads, seems to be the more pressing theme.

Our calls for Asian equity indices look constructive as a result of the moves in the S&P500 futures, which sit 0.9% higher from where the ASX200 cash closed yesterday (at 16:10 AEST). We will underperform this lead to an extent, with the ASX200 and Hang Seng cash both eyed +0.5%, while the NKY225 should open +0.9% higher. BHPs ADR suggests a flat open, so one suspects the banks should open stronger and put in the index points.

We can also see crude +2.4%, with spot coming into some big upside levels, with the 29 May swing high ($80.91) on the radar – either way, energy names should get tailwinds from this lead.

EURUSD remains well traded by clients, and while we continue to take a guide from the France-German 10yr yield spread, we also have German/EU ZEW survey expectations and EU CPI to contend with in the session ahead – given the EU CPI print is a final revision, unless we see a material deviation from the current pace of 2.6% in headline CPI / 2.9% in core CPI, then moves in French assets will be the dominant driver of EUR flows.

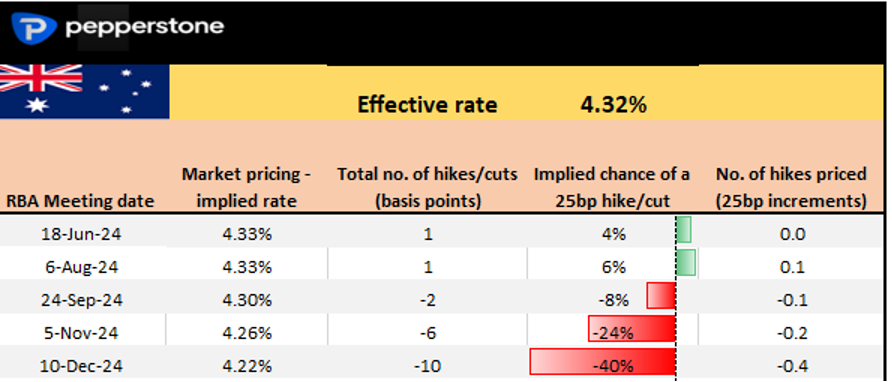

AUDUSD and the AUD crosses should get some attention today, with the RBA meeting in play at 14:30 AEST. Eyeing Aussie interest rates markets we see very little priced by way of RBA policy changes until December, when the market warms to the possibility of a cut. Essentially, the market sees very little change in the wording in the statement today, so in theory, it should be a low-vol affair for the AUD, although it is still a risk to manage. On the day I would see the upside capped at 0.6645/50, with the downside contained into 0.6580 – happy to fade moves into these levels on the day.

In the US, retail sales are due at 22:30 AEST, and these could impact if they divert from consensus of 0.3%m/m, and 0.5%m/m for the control group element. I’d say bad news is bad news for equity and the USD, where any downside surprise would increase worries about the consumer. Conversely, big numbers would be taken well by markets.

Good luck to all.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.