- English (UK)

Unless we see a more defined stance from the Federal Reserve, the combination of uncertainty towards pricing near term Fed policy, weaker US/China/German growth and the AI-related plays lacking a bullish catalyst, offers an elevated risk of further drawdown in growth-sensitive areas of the markets.

With the Fed now in a blackout period, unless a message is passed through the media, then we look for answers and clarity from this week’s US CPI print, the ECB meeting and China growth data – where, on balance, it seems unlikely we get the answers that the market is starting to demand.

Pricing risk has become a challenge

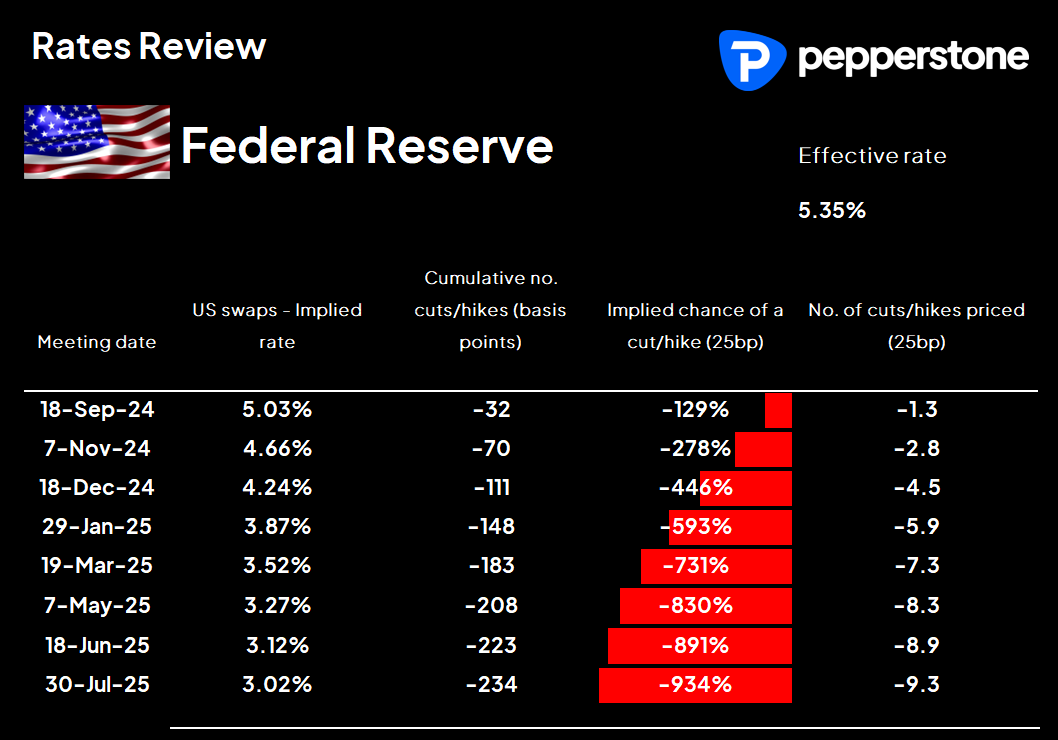

Market participants live in the future and attempt to price certainty of that future. When the future lacks sufficient clarity, we get a greater dispersion in views and the distribution of outcomes shifts. The result is typically higher volatility, de-risking of portfolios, higher correlation, and risk aversion. We are seeing this play out now. The US nonfarm payrolls lacked the clarity many craved Market players wanted to obtain clarity from the US nonfarm payrolls to help settle the 25bp or 50bp rate cut debate, as they did from Fed Gov Waller’s speech. Yet, while the employment data was weaker-than-feared and leans towards a 50bp rate cut at the September FOMC meeting, by way of best policy, it wasn’t sufficiently weak to convince the collective that a 50bp is coming - so the fact remains that we are no clearer in settling that argument.

Much ink has been spilt dissecting Friday’s US jobs report, but for me, the main factors to take away were the big revisions lower to the June and July NFP prints, and the fact that nearly all the job gains that drove a tick lower in the unemployment rate (to 4.2%) were part-time in nature. Another concern is the increase in workers who are part-time employees because they can’t get a full-time job.

We can mix in the recent fall in the ratio of job openings to unemployment, and we see evidence of a sufficient cooling of the labour market that suggests that the Fed could easily go 50bp as the policy path of least regret. Gov Waller even opined that he is an advocate of “front-loaded cuts”, but the totality of his speech was vague to the point that market players felt that the majority of the Fed voters would still vote for a 25bp cut in September.

With hindsight, the mix of weaker employment data and a non-committal Fed proved to be a toxic mix for risk, and economic-sensitive (cyclical) assets were punished. The volatility in US interest rate swaps and the US 2yr Treasury on Friday was extreme. Case in point, after Gov Waller spoke, US swaps initially priced 41bp of implied cuts (a 64% chance of a 50bp cut) for the September FOMC – however, this implied degree of easing didn’t hold, and the US swaps market settled the session with 32bp of implied cuts priced for September.

We start the week eyeing weak technical set-ups in risk

We’ve seen some sizeable technical damage to US equity indices with S&P500 futures closing on the session low and below the 100-day MA. With some punchy selloffs in Tesla, Nvidia, Broadcom, Alphabet and Amazon, NAS100 futures now eyes the 200-day MA (18,244), a marker that saw solid buying support on the 5 Aug liquidation move - should we see markets go after a more defined response from the Fed this week, I question if that support holds this time around.

The JPY remains in high demand

In FX markets, pro-cyclical/growth currencies (AUD, ZAR, and NZD) were sold, while the JPY has shown its hand once again as the place to be at present. The sheer pace of the JPY rally since mid-July would be a growing concern for Japanese authorities, but it seems that there is further to go in the unwind of the JPY-funded carry trade and with Japan Q2 GDP (due today at 09:50 AEST) likely to be revised higher, this better growth may only increase the JPY inflows. We are seeing Japanese equity being carved up, and one questions if greater cracks emerge in the Japanese funding markets.

China needs to be front of mind

Another area of concern is the message we’re hearing from commodity markets. While US data has started to impact, China’s growth rate is firmly at the heart of the commodity trade. Brent Crude tells a powerful message of weak demand and eyes the $70 level – we also see the Brent futures curve (I’ve used the front-month futures vs 8th-month contract) $1 from inversion for the first time this year. Copper is hardly looking red hot, and a downside break of 398.20 and we could be revisiting YTD lows. Chinese equities are in a strong downtrend and rallies are used as exit liquidity. Importantly, the China 10yr government bond yield and Dalian iron ore futures are at or not far off YTD lows.

It all sets us up for another big week in markets, where measures of cross-market volatility could easily rise this week – a factor which could result in a further liquidation of risk. The marquee event risks for traders to navigate this week:

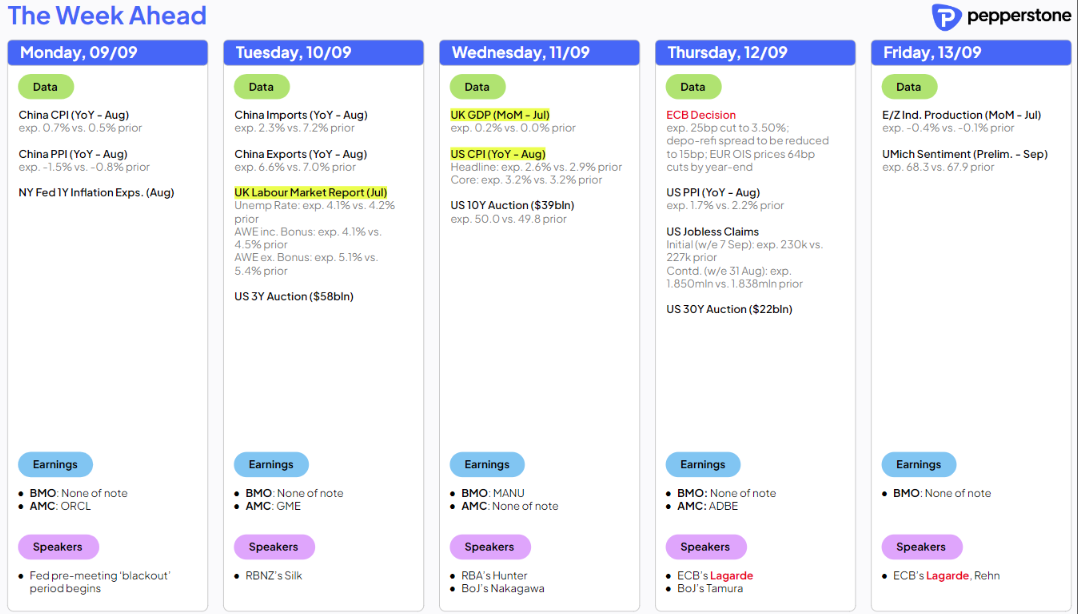

US (Aug) CPI (Wed 22:30 AEST) – With the Fed giving off strong vibes that its war on inflation is essentially over, the Aug US CPI print may be less influential on cross-market price action than in months gone by. That said, a weaker print than what’s expected could give the market an increased belief that the Fed are behind the 8-ball and has the scope to ease by 50bp. A core CPI print at 3.2% y/y - which would be unchanged from the July inflation reading – wouldn’t offer any clarity on the 25bp v 50b debate and could result in further drawdown in risky assets (such as equity and the AUD).

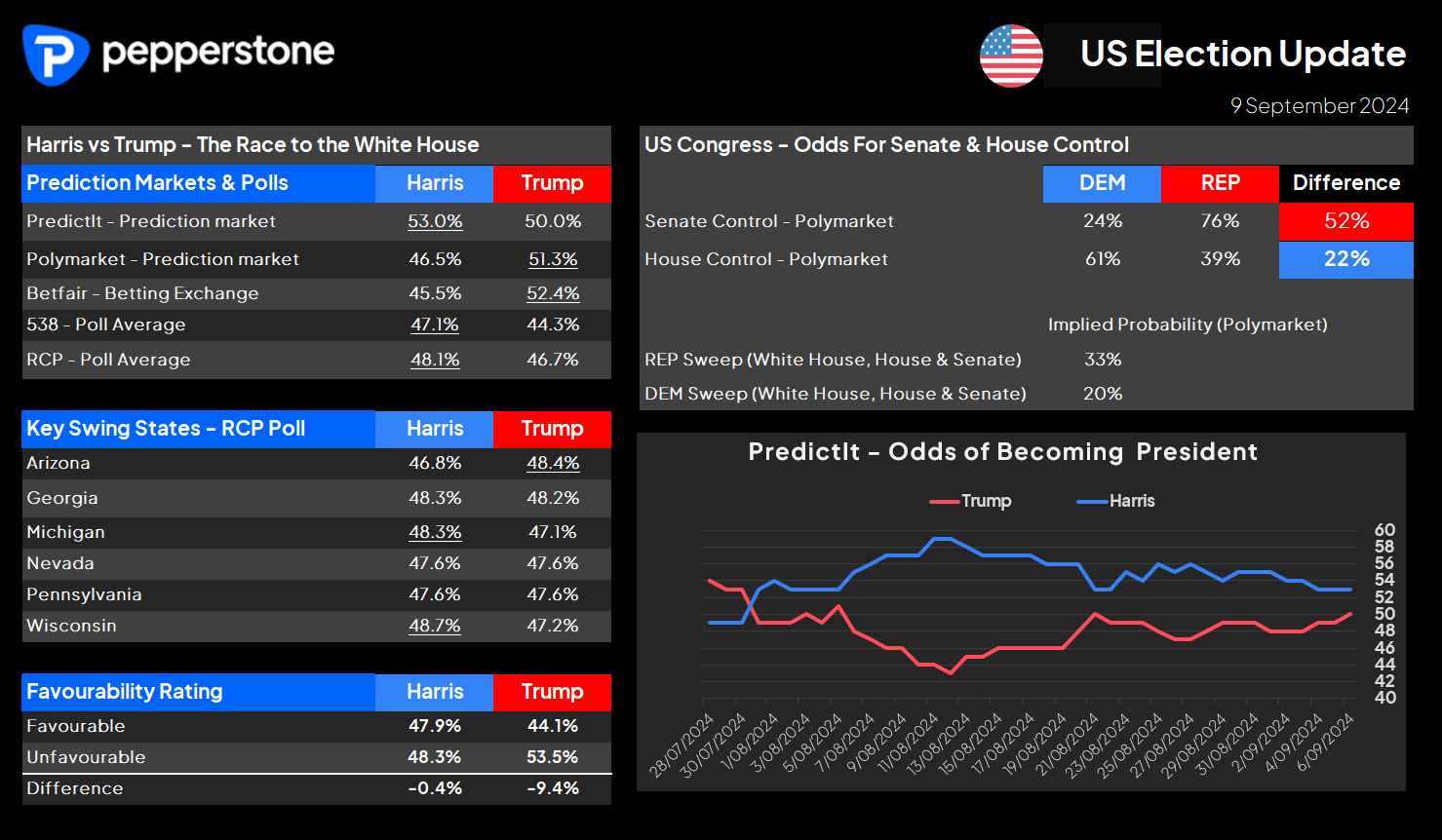

US Presidential debate between Trump and Harris on ABC (Tuesday 9 pm EDT, Wednesday 11 am AEST, 2 am UK) – While I am hesitant to suggest the debate will result in increased market volatility, the debate will clearly get great attention from the media and a wide range of market players. That said, post-debate we could start to see an increased sensitivity to changes in the prediction markets and polling post-debate. I have laid out the current standings in the US Election Dashboard, where we currently see Trump narrowly ahead in the prediction sites. Recall that the prediction markets focus on the outcome of the electoral college, while the polls are more geared toward the popular vote. We also see the implied probability the REPs get the Senate at 75%, with the DEM’s holding a 61% probability of control of the House.

The ECB Meeting (Thursday 22:15 AEST) – The ECB will almost certainly cut rates by 25bp, an outcome that is fully discounted. We also see expectations (priced into EU interest rate swaps) for a further 25bp cut by December, with the possibility of 2 25bp cuts. Therefore, the ECB’s statement outlook and guidance on policy and new economic projections is where we are likely to promote a reaction in the EUR and EU equity indices. China growth data – Throughout the week we see China’s CPI, trade data, home sales, industrial production, and retail sales data. Given the focus on China’s growth, the outcome of this data dump could matter more than usual. One can pull up a chart of Dalian iron ore, Brent crude, copper, China equity or the China 10-year govt bond yields to see why China needs to be firmly on the radar.

Apple’s “Glowtime” event (Monday 1 pm EDT) – The event will be streamed on Apple’s website and keenly viewed by shareholders and tech heads. With so many of the new features having been reviewed in the media, is the share price due for a ‘sell the news’ event? Good luck to all,

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.