- English (UK)

- English (UK)

Analysis

Rate hikes incoming? Why these dates must be on your trader radar

This is certainly a new talking point being had in some circles….

Looking at the higher timeframes, I’d argue that while we are seeing signs of distribution in the US500 and NAS100, life is pretty good and sentiment in risky assets should stay upbeat.

That is as long as the ‘Fed put’ is alive and well, and money managers see limited reasons to sell down equity holdings, knowing that the Fed have the capacity to cut rates and could even inject liquidity because the trajectory of inflation allows it.

With the Fed put in play, and 3 to 4 cuts priced through the year, why sell out of risk? Why not just stay long high beta growth/A.I equity and look periodically at hedges (they are still cheap)?

It may be hard to reconcile, but risk should even remain firm if interest cuts are almost fully priced out of the US rate curves – that is as long as the driver is strong growth dynamics. Full and buoyant labour markets, lively consumption, and demand. We may get higher bond yields but tactically it would pay to roll out of high-quality growth equity and into small caps, where the US2000 would outperform…either way, all is not lost, and the bulls will find long opportunity to drive returns.

The toxic mix for risk

Where we see the toxic mix for markets comes is if we see ‘right tail’ concerns ramp up leading to higher term premiums in US Treasurys and a spike in long-term US bond yields (both nominal and real). This comes from a higher supply of government bonds, which seems unlikely given we’ve only just seen the US Treasury Department's net borrowing requirements result in little fanfare. Or we see a turn in the collective’s belief in where inflation shaded, leading to a concerted view that Fed policy is not as tight as assumed.

My colleague Michael Brown covered his views on this dynamic in this note, and it’s well worth a read here.

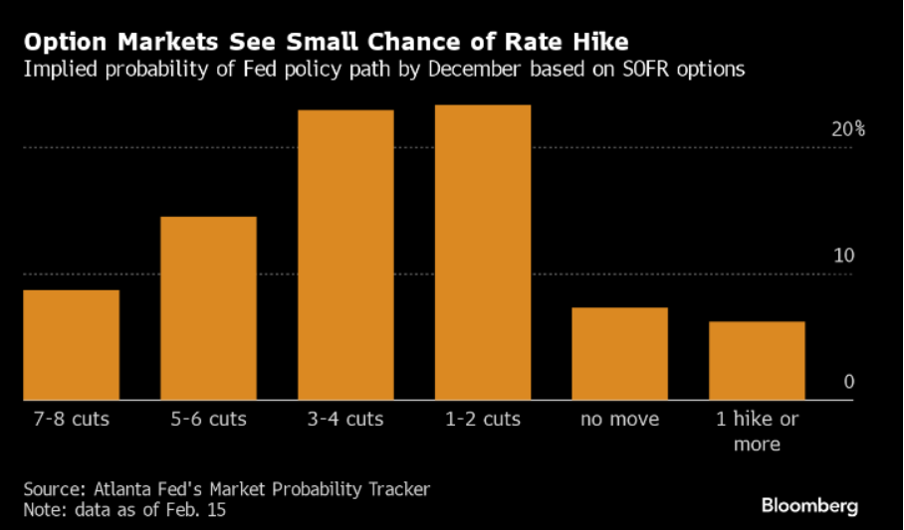

However, another development worth touching on is as we look ahead to what is likely to be a hot US core PCE inflation (due 29 Feb), are that pockets of the trading community are starting to bet on rate hikes later this year. We can see that priced in SOFR options (see the Atlanta Fed probability tracker).

While the concentration weight of bets is clearly for rate cuts to play out this year, when we look at the full distribution of outcomes (in a bimodal distribution) we can see bets for hikes are now being made and while that may be early and proven incorrect is red flag that put us on notice.

This, perhaps, very early conversation on future hikes has been given an additional tailwind with a recent opinion piece put out by ex-NY Fed President Bill Dudley that perhaps Fed policy isn’t actually as tight as many thought. Larry Summers (former US Treasury Secretary) also suggested that there’s a meaningful chance the next move might be a hike.

If interest rate and bond traders truly increase their belief that rate hikes are back on, then it will create huge uncertainty across markets. Uncertainty in this case will lead to traders having lower conviction to price risk and that leads to higher implied and realised volatility and equity drawdown.

As it stands this is all priced at a very low probability. However, in the past few days, it has come up in conversations more and more and it is a risk that if we recognize now, we can react more effectively.

It therefore puts incredible emphasis on these data points, and I think the market is under-pricing the risk of volatility here.

- 29 Feb – US Core PCE Inflation – the market will be looking for core PCE to run at a hot 0.4% mom putting us on edge – this is expected though.

- 8 March – US nonfarm payrolls (NFP) – it seems unlikely we’ll see another 300k+ payrolls, or a 4.5% YoY rate on average hourly earnings, but predicting NFPs is a tough game, and should we see big numbers again and traders will reduce risk – good news may be bad news here, especially if the wage data is hot.

- 11 March – US CPI inflation – the big risk in this sequence of key data points. If we see another core CPI print above 0.35% mom, with core services and the ‘super core’ (core services ex-rents and shelter) read hot then traders will reduce bets of a June cut and hike bets will be increased as a hedge.

- 14 March – PPI inflation – along with various components from the Feb US CPI print, the PPI print will adjust expectations for the (Feb) US core PCE print due on 29 March.

- 20 March – FOMC meeting – while big focus falls on the economic projections and dots, will assess the statement - could we see a small rise in concerns about the trajectory of inflation?

If you were to ask what could cause a prolonged drawdown in equity markets that spills out into risk FX and commodities, then it either comes from rising recession risk or higher inflation.

While most expect the upcoming US CPI prints to resume its trend to target, which would cause relief in markets, it makes sense that the “what if” sees the February data series getting huge attention from market players. Given some market players are already having the conversation about the possibility of hikes, if the February inflation data comes in hot it would almost certainly lead to higher volatility across markets.

These dates matter, put them on the risk radar.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.