- English (UK)

- English (UK)

Analysis

A Traders’ Playbook; The markets doing the work of central banks

This suggests that if we get a hot US CPI print this week then market players will increase exposure to yield curve steepeners trades, with reduced interest to short US 2yr Treasuries - In turn, this should limit the upside in the USD, given the near-zero correlation between the USD and the 2s v 10s Treasury curve.

With a focus on the US bond market, consider the US Treasury department will be issuing $101b in 3-, 10- and 30-year Treasuries this week and that could move markets around.

White - US 2s v 10s curve

Red – The USD index (DXY)

Technically, we are seeing that the USD appears to be consolidating, and while it comes with a hefty dose of risk, momentum accounts are again looking at the JPY shorts. While risk may be impacted by geopolitical news flow, NZDJPY longs look interesting for a potential breakout, especially with China coming back online, where we can see ‘green shoots’ appearing in economics. For those whose strategy thrives in higher vol regimes, then cast their eyes to LATAM FX, where outsized moves in the COP, CLP and MXN have come up on the day trader's radar.

US CPI aside, it will be a central banker fest this week, where an extensive list of Fed, BoE and ECB officials will be speaking at NABE (National Association of Business Economics) and IMF conferences. It feels like the market has made up its mind that the ECB and BoE hiking cycle is over, so Fed officials could move markets more intently.

We also get US Q3 earnings roll in, with the big money centres in play, and this puts the US30 index front and centre for index traders this week. For the political watchers, the process of finding a new House speaker will evolve and that could have big implications for the next shutdown negotiations from 17 November.

Amid rising geopolitical concerns crude remains front of mind, and we watch the reaction for the futures open, with S&P 500 and NAS100 futures skewed modestly lower on the re-open.

Marquee economic data to navigate:

US CPI (12 Oct 23:30 AEDT) – arguably the marquee event risk of the week. The economist’s consensus is we see both headline and core CPI increase 0.3% MoM. This should take the year-on-year clip on headline CPI to 3.6% headline (from 3.7%), and core CPI at 4.1% (4.3%). The market’s pricing of headline CPI (in CPI fixings) is 0.25% MoM and 3.54% YoY.

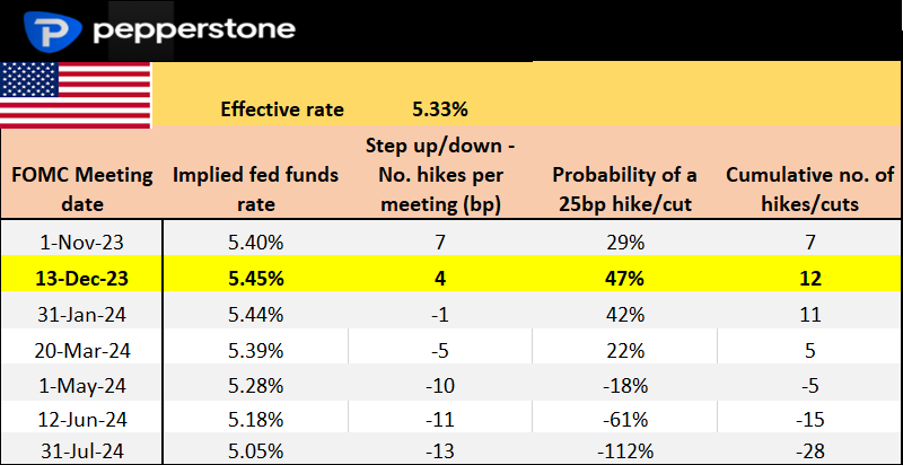

A 3-handle on core CPI would be welcomed news and see USD longs cover and see XAUUSD and NAS100 push higher. Above 4.3% could see pricing for the November FOMC increase to around 40% (currently 29%) and see bond yields rise, putting renewed upside into the USD.

US swaps pricing per FOMC meeting

US PPI inflation (11 Oct 23:30 AEDT) – final demand is expected at 0.3% MoM, with core PPI eyed at 2.3% yoy. The market is less sensitive to PPI than the CPI print, but a big beat/miss to consensus could hold implications for how economists estimate PCE inflation (due 27 Oct)

China new loans (no set day this week) – While incredibly hard to forecast, the market sees a rebound in credit with new yuan loans eyed at CNY2.5t (1.35t). Above consensus numbers could see China/HK equity build on Friday’s impressive rally and see AUD & NZD outperform.

China CPI/PPI inflation (13 Oct 12:30 AEDT) – The lowflation regime in China continues but should gently rise to 0.2% (from 0.1%) on consumer prices and -2.4% on producer prices. USDCNH has consolidated through China’s Golden Week holiday, but should we see a trend emerge, the direction of this cross could influence G10 pairs.

China trade data (13 October no set time) – The modest improvement seen in the China economic data flow should continue with exports expected at-7.3% (from -8.8%) and imports at -6% (from -7.3%). Better-than-feared numbers could see China equity push higher.

BoE credit conditions report (12 Oct 19:30 AEDT) – we get the UK monthly GDP and industrial production (both due at 17:00 AEDT) and both should remain weak. The BoE’s credit data should also be lowball, notably given what we’ve seen in recent mortgage approval numbers. Traders will be paying attention to BoE speeches this week with swaps pricing essentially pricing the BoE to have finished its hiking cycle.

Mexico CPI (9 Oct 23:00 AEDT) – the market eyes headline CPI at 4.5% (from 4.64%) & core CPI at 5.75% (6.08%). The MXN finds few friends – largely due to weaker crude prices – but local data could play a greater role this week. USDMXN has found supply into 18.40, but swing traders may look at the 17.90 area to buy pullbacks for another leg higher.

US Q3 earnings this week – Citi, JP Morgan (13 Oct), Bank of America, Wells Fargo, UnitedHealth

This week we get the US big money centres out with earnings. The focus falls on asset quality, loan demand, net interest margins (NIM) and any commentary on the recent tightening of broad financial conditions.

A focus on the US30 index

When we look at the companies included in the US30, there are only two banks (of the 30 constituents) - Goldmans and JP Morgan. However, the US30 holds an incredibly high relationship with the XLF ETF (S&P financial sector ETF), with a 10-day correlation of 93%. With so many of the major financial institutions reporting, assuming this relationship holds up, the US30 should mirror the movement in the US banks.

Another important risk for US30 traders this week is how the market reacts to earnings from United Health (UNH - report on 13 October). UNH commands a massive 10% weight on the US30, arguably the biggest weight on the index. UNH is not a stock that CFD traders look at as closely as a say Tesla or Nvidia, given its more defensive price action. It’s one for the range traders, where buying into $460 and shorting into $520 has worked well over the past 12 months. However, given the weighting, US30 traders should be aware of the influence the stock can offer.

The market prices an implied move of 2.6% move on the day of UNHs reporting, which is in fitting with the average price change over the past 8 quarterly reporting periods. UNH has seen some large percentage moves over earnings and recall in the last earnings report the stock rallied 7.2% - so a sizeable rally/decline would influence the US30 given the weight.

While macro factors such as moves in bond yields, the USD and oil prices will influence the US30, one can see that earnings this week could also play a major role – time to buy the dip, or are we about to see a leg lower in the index?

Central bank speakers

Fed speakers – on first blush Fed governor Christopher Waller may be the marquee speech to listen to.

ECB speakers – A big week of ECB speakers to navigate – EUR traders, how do you like your noise? As said, the market is fairly sure that the ECB are on hold for a lengthy period.

BoE speakers – with the markets feeling the BoE wont hike further, comments from BoE officials Mann, Pill and Bailey will be closely watched to increase confidence on that pricing.

RBA speakers – Assistant governor Christopher Kent (11 Oct 12:00 AEDT).

Related articles

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.