- English (UK)

- English (UK)

Analysis

The euro has that age old problem of wider spreads to deal with once more.

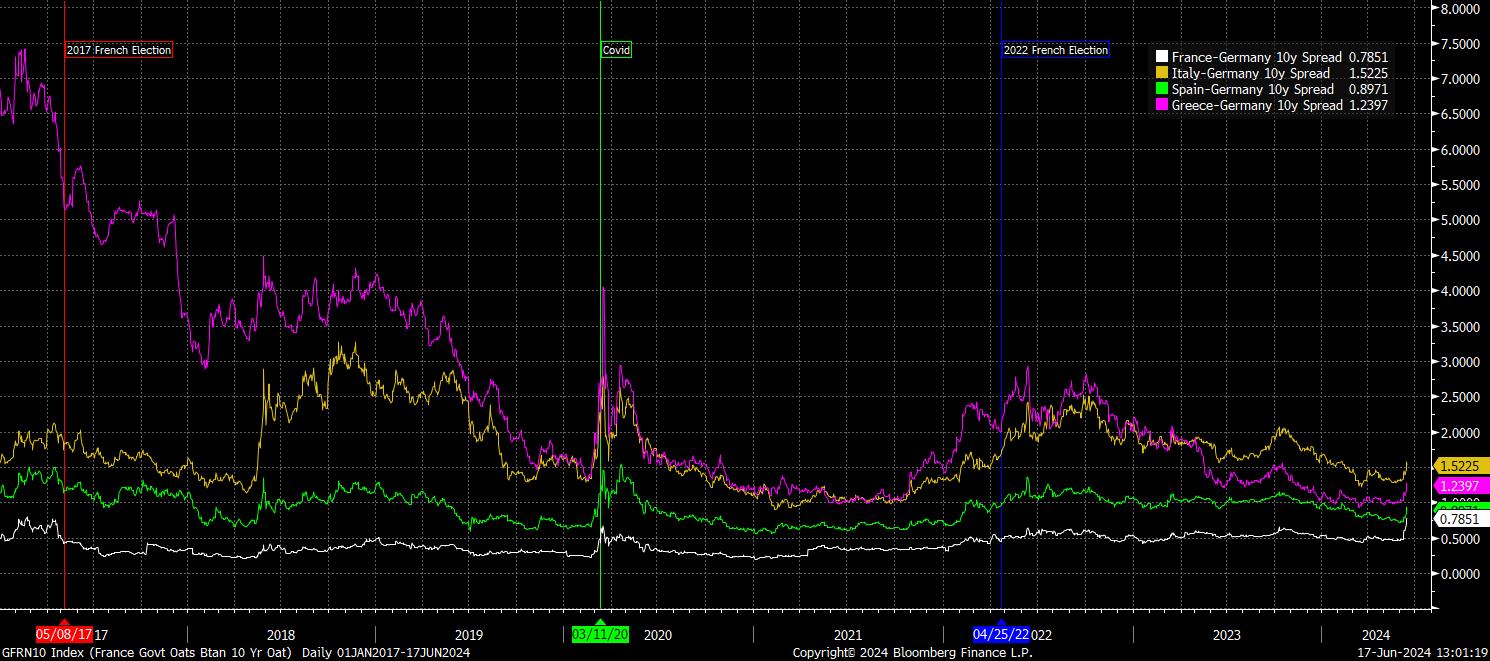

While, traditionally, it was core vs. periphery spreads that caused market angst, this time around it is core vs. core spreads which are sparking some degree of turmoil, as the 10-year France-Germany (OAT-Bund) spread blows out to over 80bp, its widest since November 2012, having widened almost 30bp last week, close to the biggest one-week move on record.

This move, however, is not just a French problem. In fact, eurozone spreads widened significantly across the board last week – the BTP-Bund spread hit its widest since February, as did the Spanish-German spread, while the Greek-German spread touched wides since late-2023.

Traditionally, wider spreads have proved a substantial headwind for the EUR, as the below chart evidences. This is due to the increased fragmentation risk that wider spreads represent, with higher yields naturally straining the ability to which an economy may be able to borrow, typically hitting periphery countries with much higher debt burdens the hardest.

_Daily_01_2024-06-17_13-03-19.jpg)

Perhaps most worryingly, for policymakers at least, is that spreads have widened so significantly despite the ECB maintain a relatively dovish stance. At the June meeting, despite a hotter-than-expected May HICP print, and notable upward revisions to the 2024 and 2025 inflation forecasts, the Governing Council still delivered the 25bp cut to which they had effectively pre-committed. Furthermore, speakers since the June decision have continued to display a relatively dovish bias, with the next 25bp cut highly likely to be delivered immediately after the summer break.

Of course, the cause of wider spreads is not monetary policy, but politics. The EU Parliament elections showed a lurch rightwards and towards populism across the European electorate, from France’s ‘National Rally’, to Italy’s ‘Brothers of Italy’, Germany’s ‘AfD’, and similar such shifts in support across the remainder of the bloc.

It is, however, in France where the ramifications of the aforementioned election results have been most significant, with the surge in support for Le Pen’s RN party leading President Macron to surprise markets in calling snap legislative elections, scheduled for 30th June and 7th July.

Typically, markets have a woeful record at accurately discounting political, and geopolitical, risks, particularly when they appear unexpectedly. So it would seem once again this time around, with not only FI, but also French equities experiencing a rather brutal sell-off.

Naturally, amid this elevated uncertainty, risks to the EUR are tilted firmly to the downside, at least until some clarity on the makeup of the next French parliament is obtained. This is particularly true given that the bar for the ECB to intervene and close spreads using the TPI – contrary to Lagarde’s blunder four years ago! – seems a relatively high one, especially after Chief Economist Lane’s remarks that recent market moves are not “disorderly” and simply represent a market repricing.

Whatever the result of the short-term political uncertainty, however, the common currency may not find itself ‘out of the woods’ so easily. Fiscal profligacy remains a substantial concern, and one that would likely be exaggerated were ‘populist’ parties to find increasing support at the ballot box. For instance, both France and Italy already find themselves at risk of falling subject to the EU Commission’s ‘Excess Deficit Procedure’, and said risk only intensifying were budget deficits to further deteriorate from already worrying levels.

Short EUR, then, will likely remain the preferred position for some time, with recent political turbulence serving as the catalyst to bring the bloc’s other issues back to the forefront of participants’ minds. With the outlook for the buck remaining a little cloudy, however, expressing a bearish EUR view via the GBP or the CHF may well be a more apt strategy.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.