- English (UK)

- English (UK)

Analysis

A traders’ week ahead playbook – Powell and US payrolls could set the market alight

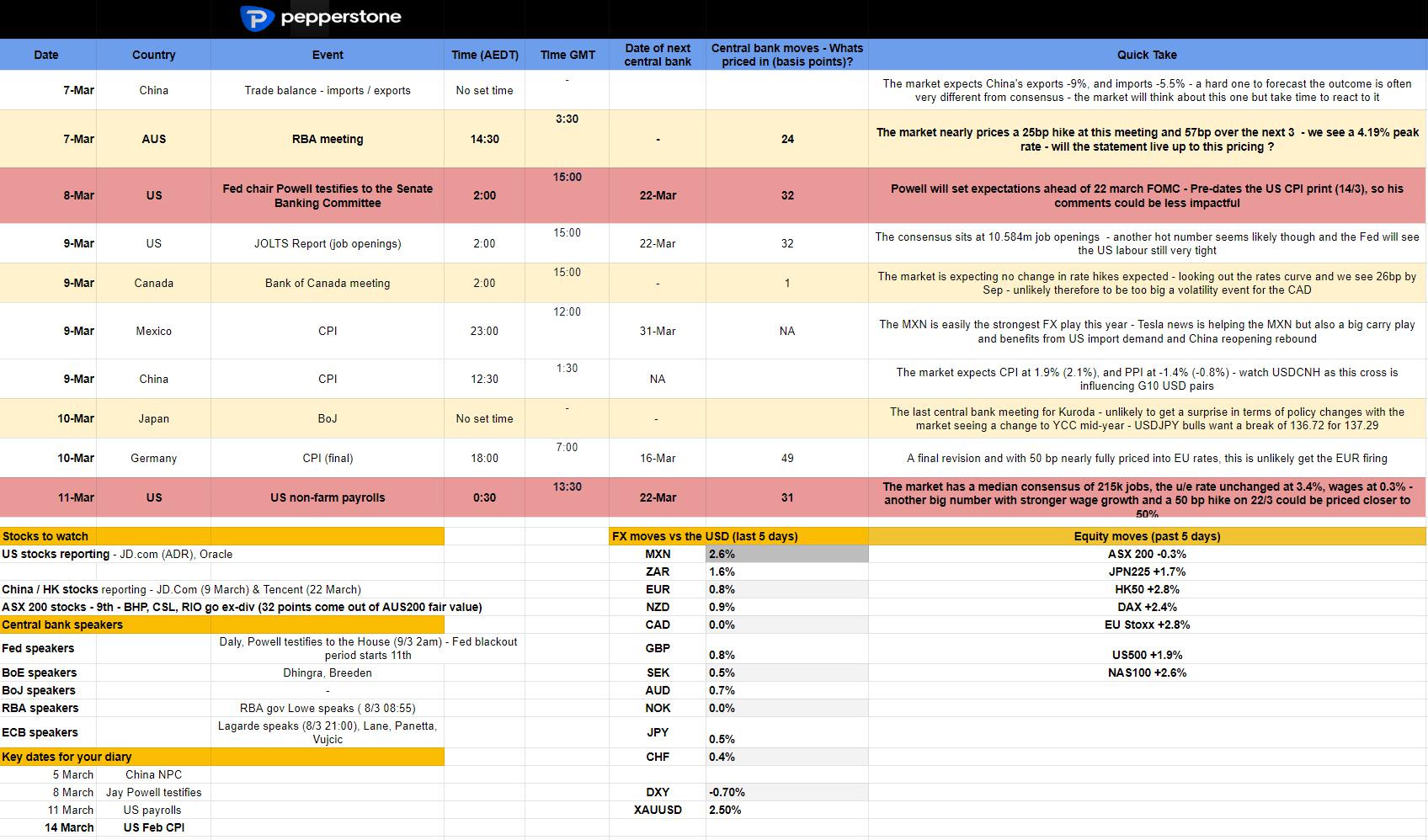

- The week ahead playbook

- Calendar of key event risks

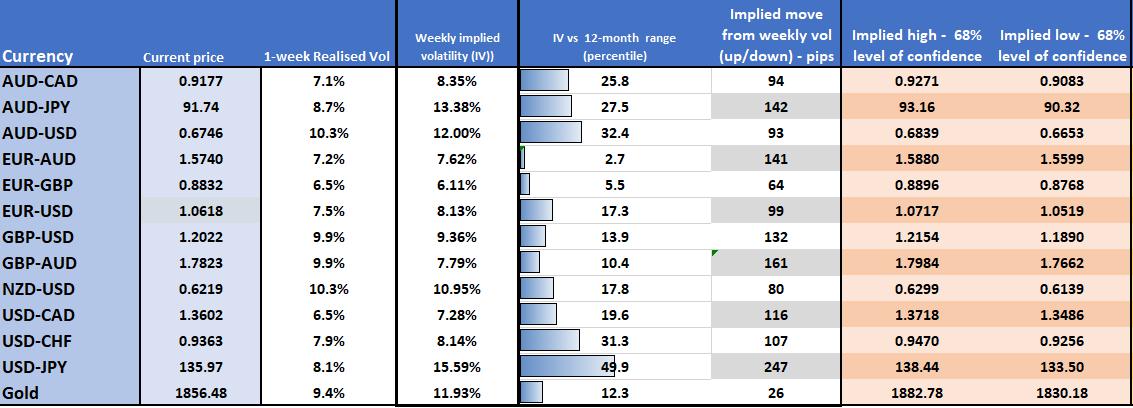

- Implied volatility matrix – how does the market see event risk playing into vol?

In US rates markets, we see 31bp of hikes priced for the 22 March FOMC meeting, which implies a 25% chance of a 50bp hike – a modest risk premium of 50bp feels appropriate as a hedge in case we get an NFP print above 300k and a core US CPI print (14 March) above 0.5% MoM.

Last week the market added 4bp added to the US terminal/peak rate pricing for September, where we see peak fed funds now priced at 5.44%, with the US 2yr Treasury closing at 4.85%, having been as high as 4.94%. The UST 10yr printed 4.06% last week but closed on Friday at 3.95%, and this seems to have had some effect on market sentiment - should we see lower bond yields this week then risky assets could see some positive follow-through.

The NFP playbook for the USD

The USD remains sensitive to interest rate pricing, but despite higher Fed rate expectations, other rates markets (such as ECB pricing) saw a more aggressive hawkish repricing. Subsequently, the USD was offered well by the market, with the DXY closing -0.7%.

(DXY daily chart)

There is good supply into 104.92, which the USD bulls want gone, a fate which would see 106 as the next stop. The USD shorts have the 1 March low of 103.72 in mind, where buyers could hold things up. An NFP below 150k would help their position, but above 300k jobs is a risk, where the market looks at the January blowout (517k) print and says perhaps that wasn’t just a one-off seasonal outcome.

Powell to offer key insights to traders

Chair Powell then cranks things up on Tuesday (Wed 02:00 AEDT) – the market is expecting some movement from his words, but trading any speech is tough, so I’d be reacting and not anticipating.

Powell will likely defend the Fed’s actions and likely make out they are going to do everything they can to bring down inflation to target.

Both the market and Fed are living data point to data point, so they are essentially flying blind until we get NFP and US CPI which – in theory – could result in them targeting a terminal rate north of 6% and require 50bp increments to get them there in a quicker fashion. Of course, that will be portrayed in the ‘dots plot’ projection (which come in the March meeting), which would need to be taken far higher for 2023.

USDJPY looks especially sensitive to the US labour market reads and Powell’s speeches, where price will remain a slave to interest rate expectations. Traders have been sellers into 136.70 (38.2% fibo of the Oct-Jan selloff), where clients now see risks as finely balanced, and the long/short skew reflects that. My preference is to wait for a close through the supply and trade a momentum move, which may not come.

RBA meeting – a 25bp hike is a done deal but is 4.2% a shared vision?

AUDUSD should get a run this week from traders with some focus on the RBA meeting – 1-week AUDUSD implied vol sits at 12%, which implies a 90-pip move on the week (higher or lower), expectations that suggest that the market isnt too concerned with higher range expansion.

A 25bp hike is a done deal, so it’s more about the guidance and whether the tone of the statement marries with peak RBA rates pricing of 4.2%. AUDUSD finds good support into 0.6700, so the bears may nibble away at that, but RBA actions aside, much of the move in the AUD will be driven by USDCNH and price action in the HK50 - Especially in the wake of China’s NPC meeting on Sunday, where the market will react to the growth target of 5%, which some will see as a somewhat underwhelming.

Staying in FX markets and the trade of buying carry (income) is firmly in play – the MXN is the poster child of such flow and the market has a love affair with MXN - lower volatility, solid China data and news of Tesla starting production in Mexico have all helped – this week Mexican CPI could cement another 25bp hike (to 11.25%) from the Mexican central bank at next meeting 31 March.

The MXN is the flavour du jour at present and is by far the best-performing currency globally, but has it gone too far? There is no consensus expectation on Mex CPI, but core CPI of 0.7% MoM or greater and the MXN should push on – one for the radar, and with its leverage to an increasing share of US imports it’s the fundamental and technical juggernaut.

Bullish equity breakouts

Equity markets remain resilient in the face of higher interest rates – while rates are going up until we see growth roll over again then traders will continue to support – EU equity looks especially remarkable, with key breakouts and new cycle highs in the GER40, EUSTX50 and SPA35 – clients are heavily skewed short in these indices and don’t trust this move – for me, the move continues to represent a geographical asset allocation rebalance, valuation and the relative expense to FX hedge US investments.

For EU equity bears to really see some drawdown then growth needs to be the dominant concern – consider we saw 17bp added to EU peak rate pricing last week, where the market now prices the ECB hiking close to 4% later this year – partly supporting EURUSD into 1.0630 – but EU equity held on.

US equity also held a solid move on Friday, although much of this has been attributed to short covering – the rally off the 200-day MA in the US500 was certainly impressive though and we watch to see if we get follow-through - the longs will be looking for 4091, with 4155 a possibility.

Gold working into $1861

Gold is also getting a firm workout from clients and while overall open interest is high, the skew in long/short positions is now 62% short. We’ve seen XAU rally in all currencies, which suggests this is not just a weak USD story and momentum favours the longs here, although the 3 Feb low of $1861 may attract sellers, especially as this marries with the 38.2% fibo of the Feb sell-off. One for the radar, and while XAU has its eyes on the US bond market, the NFP report is the key risk - gold bulls will want a number below 150k to get the party started.

Nat Gas also gets a run, and traders are attracted to the movement with price now eyeing $3, having rallied 43% in the past 8 bars.

The week ahead calendar – the key events

*Click on the Twitter link if this isn't clear.

Implied volatility matrix – we see the implied volatility priced by options dealers – this offers an implied move which can be helpful for risk purposes.

Related articles

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.