- English (UK)

- English (UK)

Analysis

Perhaps the best place to start is by examining how fixed income products can, and typically do, react to shifting macro environments. Of course, there are plenty of variables at play here, though the ones we typically focus most on are monetary policy, inflation, and economic growth (with, of course, the latter two driving the former).

It’s important to note that these factors impact different parts of the curve in different ways. The front-end of the curve, bonds maturing between 0-3 years, is typically most impacted by shifts, or expected shifts, in monetary policy – i.e., benchmark interest rates. Meanwhile, the belly of the curve (3-7 year maturities), and the long-end (maturities of 7 years or greater), tends to be much more significantly impacted by changes in longer-run growth and inflation expectations – falling growth expectations should see long bonds rally, while rising growth and inflation expectations tend to see yields move higher, and prices concurrently decline.

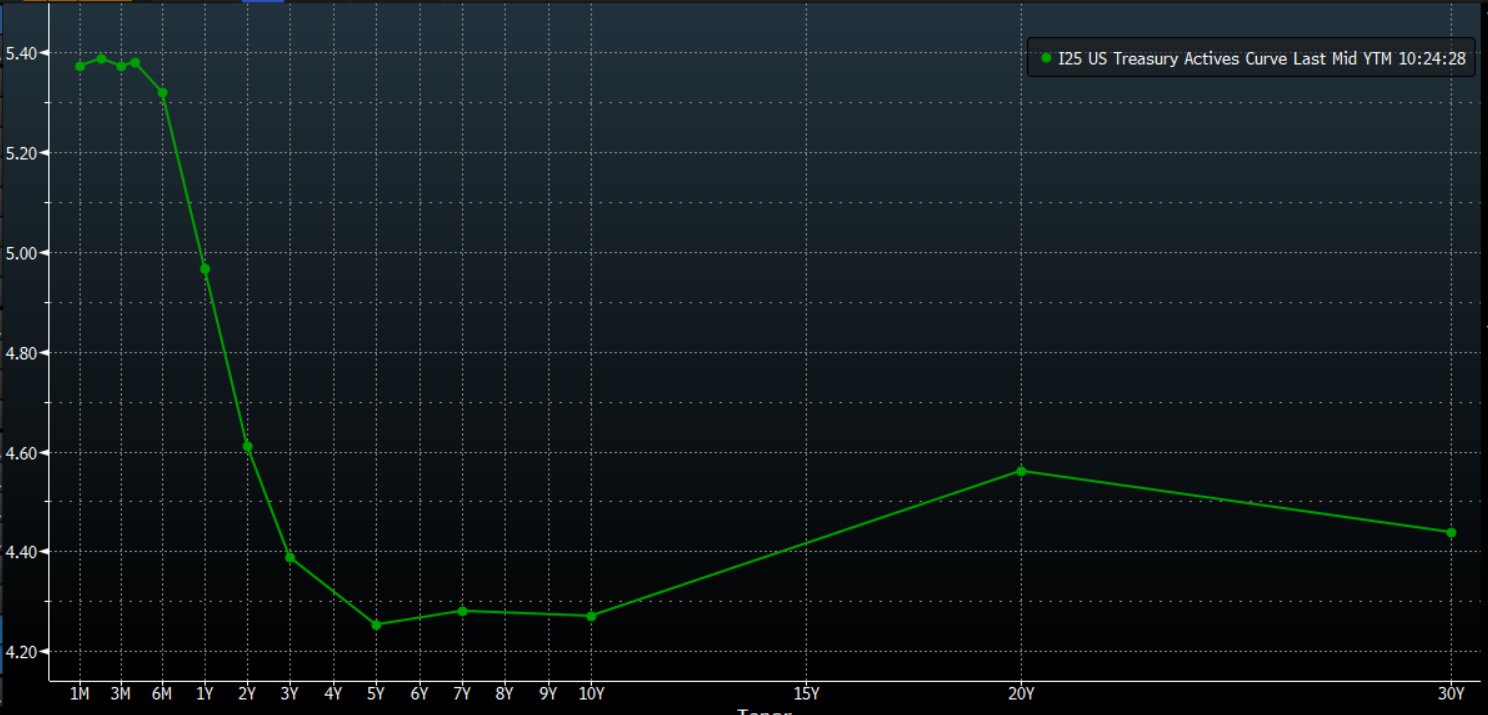

All these mentions of the ‘curve’ lead us nicely on to how one can use this concept to express a view on macro themes in a range of different ways. Before that, though, it’s worth noting that the curve is simply a visual representation of the yields of bonds of the same quality, or same issuer, but of different maturities.

Typically, this curve will be upward sloping, with higher yields at the long-end than the front-end, as investors demand additional yield premium that is typically demanded by investors for longer maturity debt due to the greater interest rate risk that is being taken on. However, at times, the curve can either be flat – where yields are similar across all maturities – or even inverted, where the curve slopes downwards, as the front-end yields more than the long-end. This latter scenario typically attracts significant attention, as an inverted curve is often seen as a harbinger of recession.

Naturally, as new information develops, and is discounted, the curve will shift in one of two ways – either to steepen, or to flatten. The way in which these shifts occur, whether they are led by the front- or the long-end, as well as whether they are a result of selling pressure, or rising demand, can be used to draw numerous conclusions, and provide trading opportunities.

For example, if one foresees a rise in geopolitical risks, or an impending economic slowdown, the natural expectation would be for the curve to bull flatten, so named as such macro factors typically foreshadow a central bank rate cut, which is typically a bullish factor for risk. To execute such a position, one would buy the long end of the curve, typically 10s or 30s, while selling short the front-end. Such a trade would have the implication of no longer speculating on the outright level of yields, instead focusing on the differential in yield, or price, between the bonds in question.

Alternatively, if one were expecting an environment where inflation and growth expectations are rising, typically seen early in the cycle, you’d expect a steeper curve, and a hawkish repricing of the policy outlook. One could gain exposure to such a bear steepening of the curve, where long-end yields rise faster than their counterparts at the front-end, by buying the front-end, and selling the long-end, again focusing on the rate differential rather than absolute level of yields.

It is not only the curve that is of interest when it comes to fixed income. For instance, one can also look at cross-country yield spreads as a way to play policy divergence. Such policy divergence is increasingly likely to emerge as the year progresses, and DM central banks begin their easing cycles.

For instance, the ECB seem the frontrunners in the race to deliver the first cut, perhaps as soon as April, given the rapid disinflation which continues across the eurozone, and intensifying downside growth risks facing the bloc’s economy, the most recent of which being continuing, and escalating, geopolitical tensions in the Middle East. In contrast, the much bumpier path back to the 2% price target, and the nature by which both the FOMC and BoE seek additional ‘confidence’ that price pressures have been squeezed out of the economy before moving to a less restrictive stance, mean cuts are much more likely to be delayed until the summer.

While one could, of course, play such a policy divergence in the FX market, simply via short EUR/USD, it is also possible to gain ‘cleaner’ exposure to such a theme through the fixed income space. If one expected the yield spread between Treasuries and Bunds to widen, as would likely occur in the above scenario, being long bunds and short 10-year Treasuries would be one way of gaining exposure to such an idea.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.