- English

Analysis

A Trader's Playbook: China Stimulus Expectations Lift Sentiment

Talk of fiscal support from the Chinese authorities has been making waves. On Friday, it’s no surprise that we saw $3.18b net buying into China’s mainland equity markets amid a 4% rally in the Chinese/HK equity indices – this supported EU and US equity sentiment, copper and the AUD found a better bid (notably vs the EUR and CHF).

AUDCHF daily – the big mover in G10 FX last week. Can it squeeze to 0.6050?

After a nirvana US nonfarm payrolls report (a strong level of job creation amid softer wages and a higher unemployment rate), we now head into the Fed’s blackout period, with the market favourable to the Fed leaving rates unchanged next week but signalling a strong bias to hike again.

Next week’s US CPI print could alter the consensus view of a Fed ‘skip’, but with the core of the Fed leaning to a pause – for now, this is supporting risk, and we roll into the new week with the bulls on top.

US500 daily chart – 4306 is the next big upside level.

Digging further into the equity move and breadth was solid on Friday, with 92% of stocks closing higher, led by materials, industrial and energy, but the chase is on – FOMU (Fear of Meaningfully Underperforming) is a factor, few want to sell, portfolio hedges are being unwound rapidly, and it was momentum frenzy, with the 0DTE crowd have a large hand in this chase higher.

There is a heightened focus on the US Treasury Department starting to tap the market to rebuild its low cash balances – we get three sizeable US T-bill sales this week, equating to $173b, so the eyes of the market will be whether this is supported by bank reserves or RRP balances. Again, US banks will be keenly watched (put the KRE ETF on the radar) because if bank reserves prove to be the larger support of T-bill issuance, it may start to weigh on sentiment here.

Finally, crude saw a 2.6% rally on Friday, largely due to a solid rally in China’s markets. Some would have been covering shorts ahead of the weekend OPEC meeting. However, those running longs would be heartened at the news that the Saudis will reduce output by an additional 1m bpd. The news on potential China stimulus and the tape in its equity markets will continue to dictate how crude trades - but the Saudis want a crude price above $80 and a steeper backwardation in the futures curve. Keep an eye on the CAD and NOK as tradeable crude proxies.

Marquee Event Risk For The Week Ahead

RBA meeting (Tues 14:30 AEST) – We could be looking at a lively RBA meeting with the market pricing a 50% chance of a hike. There is greater conviction from economists, with 17 of 25 economists (surveyed by Bloomberg) calling for a pause. Market positioning is mixed, with asset managers running a sizeable AUD short position, while fast-money leveraged funds are progressively long of AUD. RBA action will likely have a short-lived impact on the AUD before it reverts to a tradeable proxy of China data and moves in the HK50 and CHINAH.

Bank of Canada (BoC) meeting (8 June 00:00 AEST) – BoC meetings here have been predictable affairs of late, but there is some uncertainty at this meeting – it’s a risk event to consider for CAD traders. The interest rate markets price a 44% chance of a 25bp hike, although the economist community are far more certain, with only 6 of 31 (surveyed by Bloomberg) calling for the hike. Into the meeting, the risk for the CAD seems skewed to the downside, where the BoC likely hold and guides to a hike in July conditional on a hot employment report.

China trade balance (Wed - no set time) – the market looks for a further lift in the trade surplus to $94.15b. To get to this increase, surplus exports are expected to decline by 2%, while imports are expected to decline by 8%. This is a key data point given the impact China has on market sentiment, but this is so incredibly hard to forecast that the market is conditioned to be shocked.

China CPI/PPI inflation (Friday 11:30 AEST) – The market expects CPI to come in at 0.2% YoY and PPI at -4.2% YoY. With elevated expectations of imminent policy easing from the PBoC, we’d need to see a blowout upside print to reduce expected policy easing calls. The bad news (i.e., lower inflation) should further increase policy-easing expectations and prove good news for the HK50 and the AUD.

China’s new yuan loans (no set time) - the market is looking for new loans to increase to RMB1570b (from RMB718b). With calls for renewed economic stimulus, I expect credit data to start reflecting this going forward to rise from here. I don’t expect the May credit data to move markets too intently unless it’s a substantial beat/miss.

US ISM services (Tues 00:00 AEST) – the market looks for the diffusion index to rise to 52.4 (from 51.9). In a quiet week of US economic data, the services ISM report has the potential to influence market sentiment. However, after Fed chair Powell and VC Jefferson recently leaned towards a pause (or a skip), it’s hard to see this moving rate expectations for the June FOMC meeting too intently. The US CPI print (due 13 June) is the likely decider on whether the Fed pause or hike.

Canada May employment report (Tues 22:30 AEST) – the market expects 25k net new jobs to have been created in May, with the unemployment rate eyed at 5.1% (from 5%). The form guide suggests a higher probability of a beat, with the last 8 employment reports coming in above expectations. Momentum in USDCAD is lower, and we see good support into 1.3330.

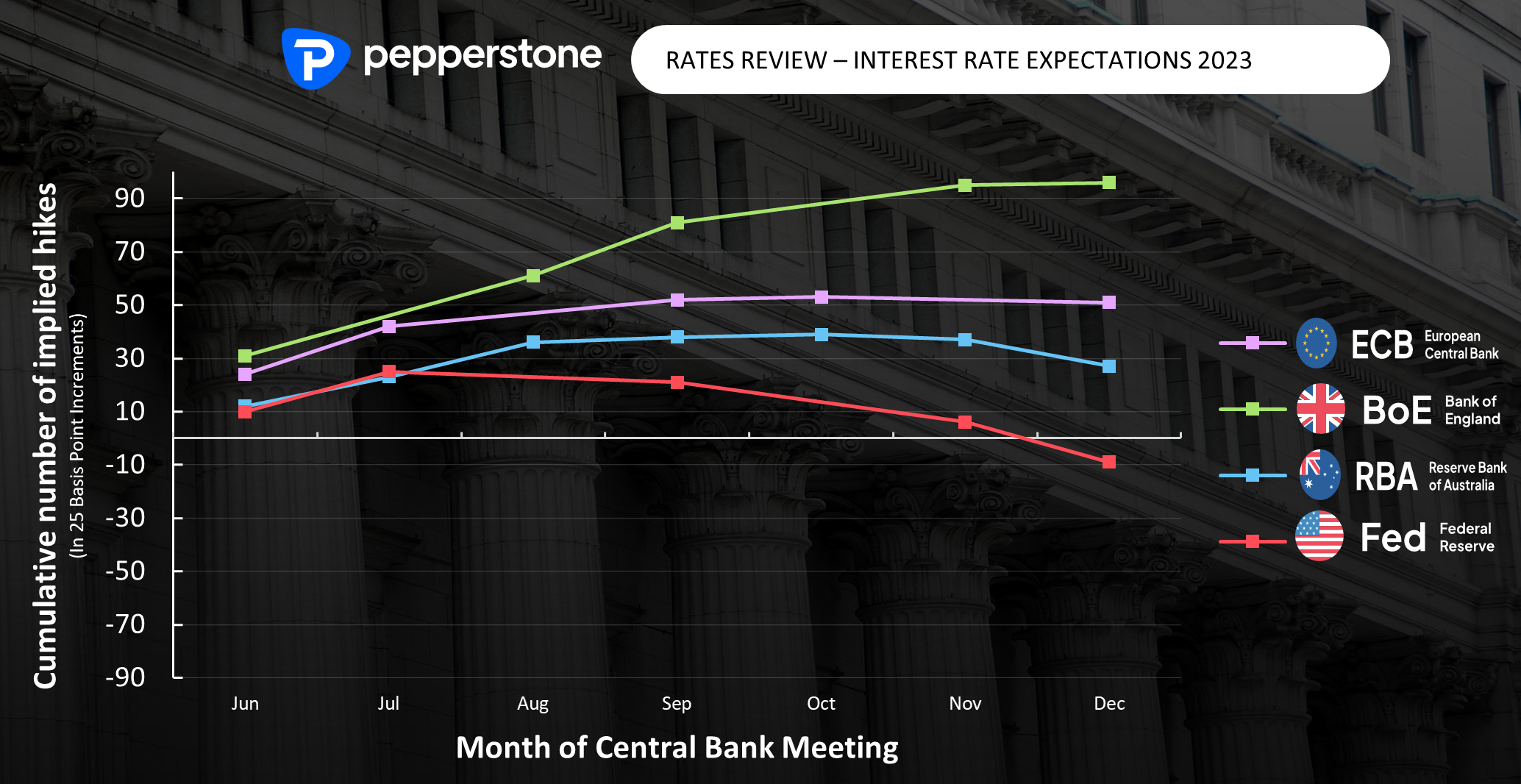

Rates Review

We look at the market pricing of interest rate expectations and the cumulative number of hikes/cuts (in basis points) for each upcoming meeting. For example, we see 10bp of hikes (a 40% chance of a hike) priced for the June FOMC meeting but 9bp of cuts to have been implemented by December.

Central bank speakers to navigate:

Fed speakers – the Fed is in a blackout period until the FOMC meeting (14 June), so we can breathe a little easier.

ECB speakers – we hear from Lagarde, Nagel, Guindos, Panetta, Guindos, De Cos, and Centeno – EU rates market price 24bp of hikes for the 15 June ECB meeting, and a peak rate of 3.66% by October.

RBA speakers – RBA gov Phil Lowe speaks the day after the RBA meeting (Wed 09:20 AEST). RBA deputy gov Michele Bullock speaks shortly after (Wed 09:50 AEST)

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.