- English

Gold Falls Below $5,000: Safe-Haven Logic Takes a Back Seat as Inflation Hedging Drives the Market

.jpg?height=93&quality=30)

On Wednesday, gold (XAUUSD) experienced a significant pullback, dropping 3.7% in a single day and falling below the key support zone of $4,850–$4,900. This move occurred amid escalating geopolitical tensions, clearly diverging from traditional safe-haven logic, and raising new questions about gold’s short-term pricing dynamics.

In the current environment, two competing logics are pulling gold in different directions: on one hand, geopolitical risk supports safe-haven demand; on the other, a high-interest-rate environment significantly raises holding costs. This tension between “safe-haven attributes” and “non-yielding assets” means gold no longer benefits unilaterally from risk events, resulting in a more complex volatility structure.

Escalating tensions trigger de-risking: the core of gold’s decline

Reports indicate that Iran’s South Pars gas field and several energy facilities were attacked, with Iran declaring some Gulf energy infrastructure as “legitimate targets.” The conflict has spread from military engagements to energy infrastructure, driving Brent crude prices up over 7%. In stark contrast, gold did not strengthen alongside oil; instead, it accelerated its decline.

This divergence highlights a shift in market pricing focus. Some traders have turned to long positions in options linked to rising oil volatility to hedge inflation risk, which is a more targeted strategy than simply holding gold. Meanwhile, gold had already priced in a significant portion of geopolitical risk, leaving little momentum for further gains unless the conflict escalates unexpectedly.

As tensions rise, the market is moving into a de-risking phase. Risk assets, including U.S. equities, are under pressure, and liquidity has tightened. Forced cross-asset liquidations, margin calls, and portfolio rebalancing by institutions have all added to selling pressure on gold.

Moreover, the $5,000/oz level serves as an important psychological support. A breach triggers algorithmic sell orders and short-term stop-losses, amplifying the pullback. In this context, gold’s short-term volatility is driven not only by fundamentals but also by concentrated, short-term capital flows.

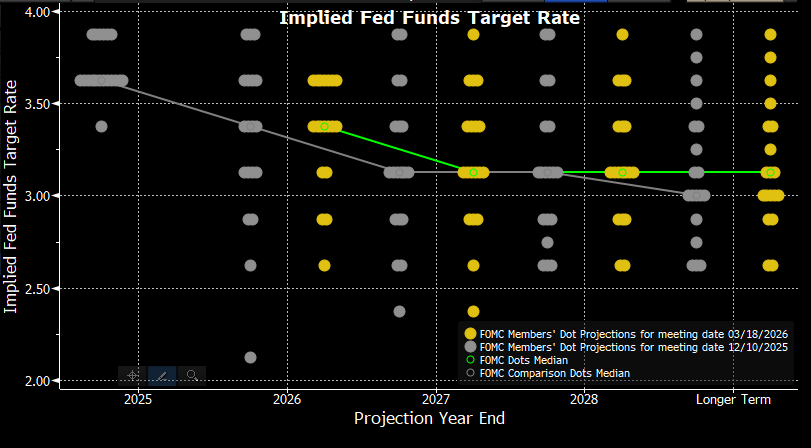

Federal Reserve holds steady: safe-haven funds redistributed

Beyond liquidity dynamics, the market’s re-pricing of the interest-rate path has been a key factor in this pullback.

At the March FOMC meeting, the Federal Reserve kept rates unchanged and continued to signal a “wait-and-see” approach. Although the dot plot still indicates a rate cut in 2026 and 2027, internal expectations have diverged, and inflation projections for 2026 were revised upward. This reflects growing uncertainty around the policy path, particularly amid rising energy prices.

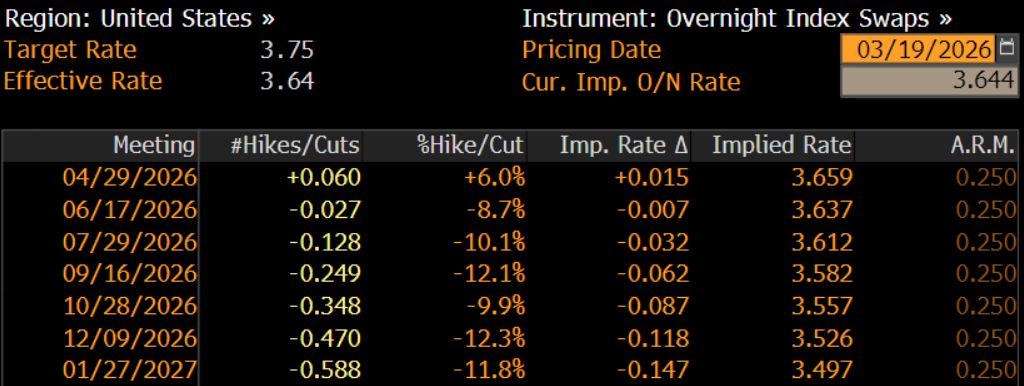

More importantly, the market has sharply narrowed expectations for rate cuts. USD swap markets show that the implied rate cut for this year has dropped below 12 basis points. In other words, the market is moving from a “loosening expectation” back to a “higher-for-longer” framework.

Powell reinforced this message during his press conference. He noted that rising energy prices could boost inflation but emphasized the difficulty of gauging its persistence and stressed that policy is not pre-set. This signals that the Fed is more likely to remain on hold in the near term rather than easing.

In this environment, the main challenge for gold is the lack of rate support. Extended periods of high rates increase the opportunity cost of holding gold, reducing its appeal.

By contrast, the USD has attracted more buying. Beyond safe-haven demand, the U.S.’s lower dependence on energy imports, rising inflation concerns, delayed rate cuts, and the narrative of the U.S. as a potential energy alternative exporter all helped push the dollar index back above 100.

For dollar-denominated gold, this creates a double headwind: prices are suppressed, and purchasing costs for non-dollar traders rise, further constraining global demand.

Pullback continuation or rebound ahead?

Overall, this sharp decline in gold reflects a confluence of factors: large-scale risk asset liquidations, a hawkish shift in Fed expectations, and a stronger dollar. This appears more like a “pricing logic adjustment” than a reversal of the long-term trend.

In the medium to long term, gold’s structural support remains intact. Ongoing central bank purchases, unresolved U.S. fiscal deficits, and persistent geopolitical risk continue to underpin the metal. Thus, the current pullback is better viewed as a technical adjustment driven by news and capital reallocation rather than the end of the bull market.

In the short term, the market’s core focus is shifting from “safe-haven demand” to “inflation hedging,” with gold no longer the preferred instrument. In this context, changes in energy prices, especially whether oil supply recovers, will be key drivers of gold’s performance.

If the conflict persists and the Strait of Hormuz faces transport disruptions, global energy inventories could tighten further, leading to heightened volatility in gold as bulls and bears vie for control.

In a more extreme scenario, if high oil prices significantly suppress demand before pushing long-term inflation higher, the market could pivot to trade “policy shifts,” even pricing in potential Fed Put ahead of time. While the probability is low, such a development could trigger a rapid and sizable rebound in gold prices.

Conversely, if there is tangible progress toward conflict resolution or effective restoration of energy supply, the previously priced-in risk premium could quickly unwind, putting additional pressure on gold.

In today’s highly news-sensitive market, price swings can be rapid and dramatic. Rather than merely betting on direction, managing positions and risk exposure remains paramount.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.