- English

Analysis

The NAS100 had its best day since 14 Nov, as tech led the way courtesy of Nvidia’s new product launch, with new graphic cards that can lead the way in AI PCs. Tech aside, the rally was broad-based, with 84% of stocks closing higher and energy the only sector closing lower.

Long NAS100 / short US30 is a trade that I see as having further juice, with Boeing subtracting 132p from the US30 alone. Either way, new equity highs seem to be the more likely risk here.

Further tailwinds for risk appreciation have come from a NY Fed 1- and 3-year inflation survey which showed further moderation, while Fed member Bostic detailed he thought inflation had come down more than expected. Crude prices falling 3.8% and an 8.6% fall in EU Nat Gas prices seem to be giving risk a kick, as are the modest falls in US nominal and real yields too.

As always, we try and justify a move in markets after the fact, but it’s the flows that count and that we trade, and price action suggests weak shorts have covered, with the bull’s regaining composure.

Can it last? Well, one suspects that comes down to the outcome of this week's US CPI data and while much of the macro discussion has swung on the future of balance sheet runoff (‘QT’), those long equity/short USDs will need to see further downside momentum in core CPI and going someway to justifying the 25bp cut priced for March and 142bp of cuts priced for the year.

As we see below the event risk heats up this week, with CPI prints all over the shop and China’s data flow and credit stats also a factor. US earnings kick into gear with the banks giving us insights into their asset quality and credit trends. Bitcoin is already flying high as the market is firmly of the view the SEC give its blessing for the cash ETF, and there is no signs that the market is ready to sell the fact just yet.

We also start to focus on political issues although whether the market trades these themes is another factor. Next week we get the Taiwan elections and that could have implications for USDTWD. We also start the proceedings in the US election with the Iowa caucus, although most are looking more at the Primary in New Hampshire (23 Jan) with Nicki Haley polling quite well in that state. And so it starts….

Good luck to all.

Key marquee event risks to navigate:

Tokyo CPI (9 Jan 10:030 AEDT) – the market eyes 2.5% yoy on headline CPI (from 2.6%) and 3.5% on core (3.6%). The Tokyo CPI print leads the national CPI numbers, so they could influence BoJ expectations and by extension the JPY.

Aus monthly CPI (10 Jan – 11:30 AEDT) – the market eyes the monthly CPI print at 4.5% (from 4.9%). The monthly print comes before the all-important Q4 CPI print on 31 Jan. Aussie interest rate futures price a cut in May at 25%, with 43bp of cuts priced by Dec 2024. AUDUSD looks supported by the rally in US equities, although to get the pair firing through 0.6750 we may need to see a reversal higher in Chinese/HK equity markets.

BoE gov Bailey testifies to parliament (11 Oct 01:15 AEDT)

ECB member Schnabel speaks (11 Jan 01:00 AEDT) – EU swaps price a 25bp cut in the March ECB meeting at 50% - EURGBP is on the radar with momentum skewing the cross to lower levels and potentially a re-test of 0.8540.

Fed speakers - NY Fed member John Williams offers his 2024 economic outlook (11 Jan 07:15 AEDT)

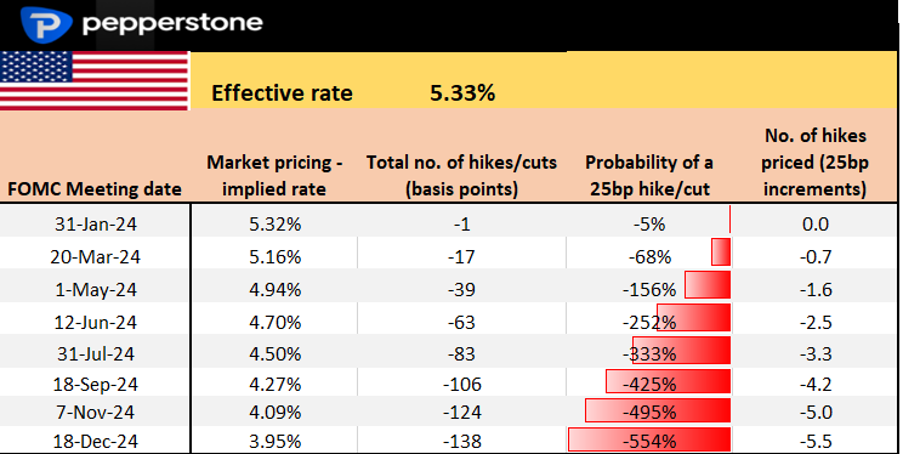

US CPI (12 Jan 00:30 AEDT) – this is the marquee event risk for the week so watch exposures over this key data point. The market looks for headline CPI at 0.2% mom / 3.2% yoy (from 3.1%) and core CPI at 0.3% mom / 3.8% yoy (from 4%). US swaps price a 25bp cut in the March FOMC at 69%, with 140bp of easing by Dec 2024 – this pricing will come into review on the CPI print, and by extension, the USD and equity markets will move in sympathy.

US swaps pricing per meeting

China's new yuan loans and aggregate financing (no set time or date this week) – the market looks for a small lift in new yuan loans to RMB1350b. There is a growing view that credit will soon increase as banks ease borrowing costs, but is there a demand for cheaper credit?

China CPI/PPI (12 Jan 12:30 AEDT) – the market looks for China’s CPI to come in at -0.4% yoy, and PPI -2.6% yoy. We see the Chinese bond rallying strongly with 10yr govt bond yields at multiyear lows, suggesting a market high on easing PBOC easing expectations – A weak CPI print should only increase expectations of a RRR cut.

China trade balance (12 Jan – no set time) – this can be a notoriously hard data point to price risk around given the outcome is typically someway off the median consensus estimates. As it stands the view is we see a 1.6% rebound in exports, and 0% growth in imports. The HK50, CHINAH and CN50 could be sensitive to the outcome of this print and traders will want to see a solid rebound to initiate longs.

Other CPI prints – Mexico (9 Jan 23:00 AEDT), Columbia (10 Jan 10:00 AEDT), Norway (10 Jan 18:00 AEDT)

Other key events to navigate:

- Crypto traders - The SEC deadline on Bitcoin cash ETF (10 Jan – no set time)

- US bond auctions - 3YR Treasury ($52B - 10 Jan 05:00 AEDT), US 10YR ($37b – 11 Jan 05:00 AEDT), 30YR ($21b – 05:00 AEDT)

- US banks earnings due out on Friday - Blackrock, JP Morgan, Bank of America, Wells Fargo, and Citi

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.