- English

- عربي

Nvidia Earnings Beat Expectations but Shares Slide as AI Concerns Linger & Investors Want More

Key Takeaways

• Revenue beat analyst forecasts by more than $2 billion

• April quarter guidance significantly exceeded expectations

• Margins remained strong and are expected to hold up

• Shares initially surged above $200 before reversing sharply

• AI CapEx returns and long-term visibility remain key concerns

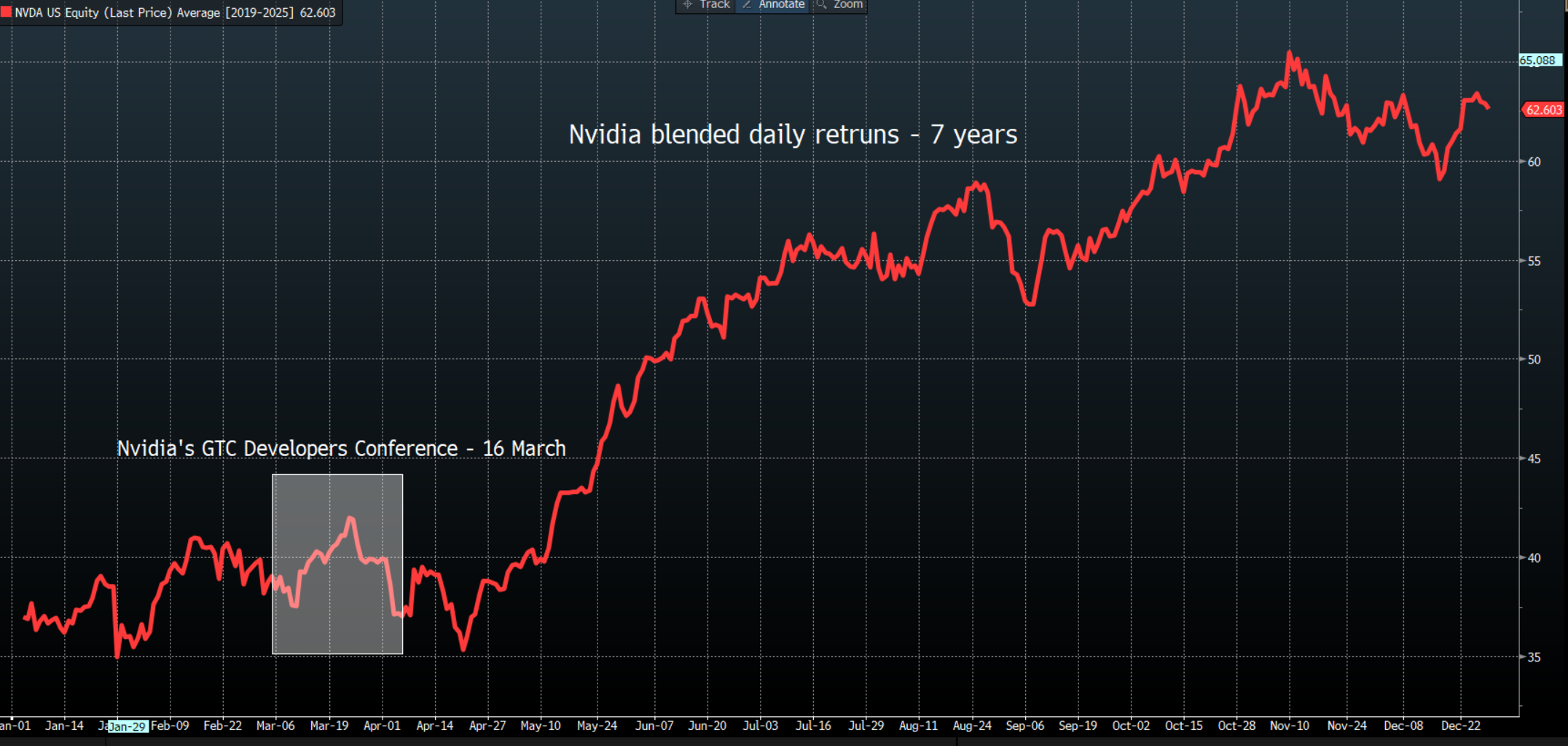

• Nvidia's GTC conference on 16 March could be the next major catalyst for the share price

Nvidia Delivers a Strong Earnings Beat

As we wrote about yesterday, Nvidia delivered a clear upside surprise in its latest quarterly results. Revenue came in more than $2 billion above the central analyst forecast, while guidance for the April quarter was materially stronger than expected.

Margins also impressed, and management indicated they are likely to remain resilient into the next reporting period. Commentary around demand trends was upbeat, reinforcing the strength of the current AI investment cycle.

Immediately following the release, Pepperstone’s Nvidia 24-hour CFD surged to $203.35. Market participants quickly focused on whether the stock could close decisively above $200 and potentially challenge the all-time highs near $212.

Strong Numbers, Weak Price Action

Despite the impressive earnings performance, the rally proved short-lived. Sellers quickly took control, reversing early gains. During US trade, Nvidia dropped sharply from around $196.50 and consolidated near $184 into the close. The scale of the decline surprised many, given the strength of the reported figures and raised questions about underlying investor sentiment.

Competition and Long-Term Outlook in Focus

While the earnings numbers themselves were difficult to fault, investors appear increasingly focused on broader risks.

Competitive inroads, particularly in China, remain a point of attention. There is also a growing desire for clearer visibility into Nvidia’s growth trajectory into 2027. The anticipated Rubin platform ramp could provide meaningful revenue and earnings tailwinds, but markets may be hesitant to fully price in that upside without firmer guidance.

Additionally, rising DRAM pricing and memory supply constraints could eventually pressure margins, introducing another variable into forward estimates.

AI CapEx and Funding Questions Persist

A key theme weighing on sentiment is the return on investment from the hyperscalers’ (Amazon, Meta, Microsoft, Alphabet, Oracle) massive capital expenditure commitments.

Although AI demand remains robust, investors are questioning whether capital markets will continue to support such aggressive funding cycles across the broader ecosystem. This concern extends beyond Nvidia and was reflected in selling pressure across the semiconductor space, including Broadcom, Advanced Micro Devices, Marvell, Taiwan Semiconductor Manufacturing Company, and SK Hynix.

Nvidia's GTC Developers Conference as the Next Catalyst

Attention now shifts to Nvidia’s GTC Developers Conference on 16 March. Historically, GTC has been a positive event for the share price, often serving as a platform to showcase product leadership and long-term strategic vision.

This year, markets will be looking for deeper insight into the operating environment, clarity around earnings potential into 2027, and demonstrations of next-generation technologies, including Grok SRAM low-latency inference CPUs and optical networking innovations.

If management can provide stronger forward conviction, GTC may prove to be the catalyst that earnings alone were not.

Analyst Earnings Upgrades Despite Market Scepticism

Following the results, analysts revised price targets higher, suggesting that the fundamental story remains intact.

However, price action tells a more cautious story. Nvidia remains a highly tradable stock, attractive to traders keen to trade on both the long and short side. For now, the market appears unconvinced about sustaining a breakout above $200.

A broader improvement in macro conditions and renewed confidence in AI and high-growth semiconductor valuations may be required before a durable uptrend can reassert itself.

Conclusion

Nvidia delivered exceptional earnings and strong forward guidance, yet the stock failed to maintain its breakout attempt. The reaction underscores lingering concerns around competition, AI investment returns, and long-term growth visibility.

With the GTC conference approaching, investors are looking for more than strong quarterly results. They are seeking reassurance that Nvidia can maintain its leadership and justify premium valuations in an evolving AI landscape.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.