- English

- عربي

Per FactSet, S&P 500 earnings growth is seen at 8.8% on a YoY basis in Q2, marking the fourth consecutive quarter of growth for the index while also, if delivered, marking the highest rate of earnings growth since the first quarter of 2022.

Revenues, meanwhile, are seen rising 4.6% YoY for the S&P as a whole, marking the 15th straight quarter of revenue growth for the index, with 9 of the 11 sectors set to report a YoY revenue increase.

Nevertheless, as has been the case for some time, the market continues to look ‘expensive’ per traditional valuation metrics. The S&P 500’s forward 12-month P/E ratio currently stands at 21.2, well above both the 5-year average of 19.3, and the 10-year average of 17.9. Furthermore, there remains an ‘earnings gap’, between the level at which the S&P 500 trades, and the index’s adjusted EPS.

_spx_v_2024-07-10_06-55-38.jpg)

In any case, and as s typical of reporting season, earnings expectations have been gently massaged lower throughout the quarter. On the whole, street EPS estimates for the S&P 500 fell around 0.5% over the three months to the end of June, though it is important to note that such a downward revision is somewhat lower than the 5-year average of 3.4%.

That said, while lower in magnitude than has been seen during recent reporting seasons, the gradual decline in earnings expectations once more reaffirms the importance of positive forward-looking guidance when it comes to unlocking a substantial post-earnings rally in individual stocks. It is, relatively speaking, easy for a firm to massage earnings expectations lower, and to then deliver a chunky beat; it is substantially harder to pull off the same trick when it comes to issuing guidance.

Meanwhile, at a sector level, while 9 of the S&P’s 11 sectors are set to report YoY revenue growth, 8 of the 11 are set to report YoY earnings growth. This includes 4 – Communication Services, Health Care, Information Technology and Energy – where consensus foresees YoY growth in excess of 10%. At the other end of the scale, the Materials sector is set to report the most significant YoY earnings decline.

As is typical, banks kick-off reporting season, with JPMorgan (JPM), Wells Fargo (WFC), and Citi (C) set to report before the opening bell on Friday. These will subsequently be followed by Goldman Sachs (GS) on Mon 15th, before Morgan Stanley (MS) and Bank of America (BAC) wrap things up on Tues 16th.

Overall, banks are set to report a YoY earnings decline in the high single-digits, with the general feel of earnings, and guidance, likely to be broadly similar to that seen in the first three months of 2024. Net interest income remains capped by relatively slow loan growth, while net interest margins continue to bottom out, ahead of the first Fed cut, for which my base case remains September. Broader macroeconomic commentary from bank CEOs will also be in focus, as the US remains on course for a ‘soft landing’, despite cracks beginning to emerge in the labour market.

_kbw_b_2024-07-10_06-55-29.jpg)

Beyond the banks, and although still some weeks away, it will be earnings from the ‘big tech’ behemoths that market participants also seek to focus on.

The Communication Services sector – including Meta (META) and Alphabet (GOOGL) is set to report the highest YoY earnings growth of any of the 11 sectors in the index, while Information Technology – which comprises stocks such as Nvidia (NVDA) – is set to notch the third highest YoY earnings growth rate. Of course, NVDA’s earnings, albeit not due until towards the end of August, will be one of the most significant releases of earnings season, not least as investors seek to gauge how much juice is still left in the tank, after a stellar 165% YTD advance at the time of writing.

_mag_7_2024-07-10_06-55-01.jpg)

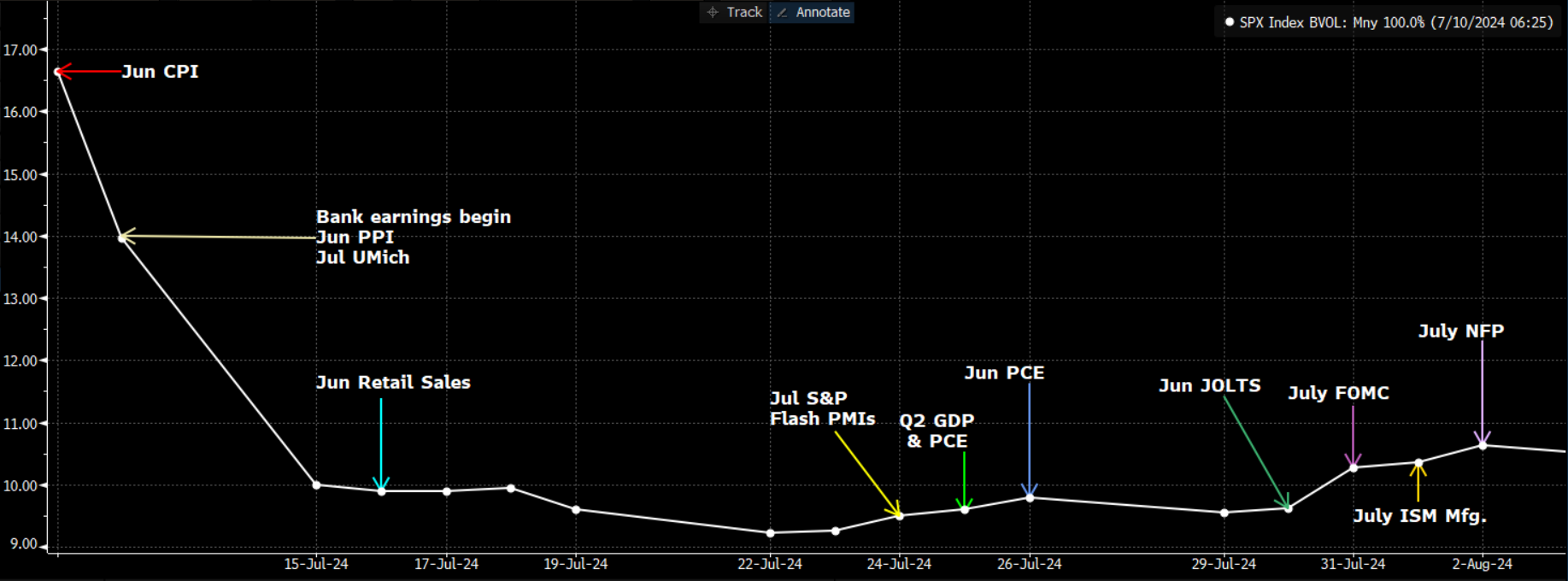

Of course, it is not only earnings season that the equity market must navigate, with a number of other significant risk events looming on the horizon in the short-term.

The most obvious, and significant, of these, is the June CPI report, due tomorrow (Thurs 11th July), and seen by many – including your scribe – as a key determinant of whether the aforementioned September FOMC cut remains plausible. Both policymakers and market participants alike will be looking for further evidence of disinflation, particularly after the April and May CPI prints showed a continued cooling in price pressures. Beyond this, there remains the Q2 GDP (and all-important PCE) release, as well as the usual round of top- and second-tier macro releases, plus the July FOMC meeting at the tail end of the month.

Despite this, and although earnings season naturally presents a key risk for equities more broadly, the medium-term path of least resistance should continue to lead to the upside. Not only is the ‘Fed put’ still in place, in a flexible and forceful form, but both economic and earnings growth should remain resilient, even if the latter fails to meet the relatively high bar that Street analysts have set. Dips, therefore, should remain relatively shallow, and continue to be seen as buying opportunities.

Related articles

.jpg?height=420)

.jpg?height=420)

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.