- عربي

- English

Catastrophic CPI Poses BoE and GBP A Headache

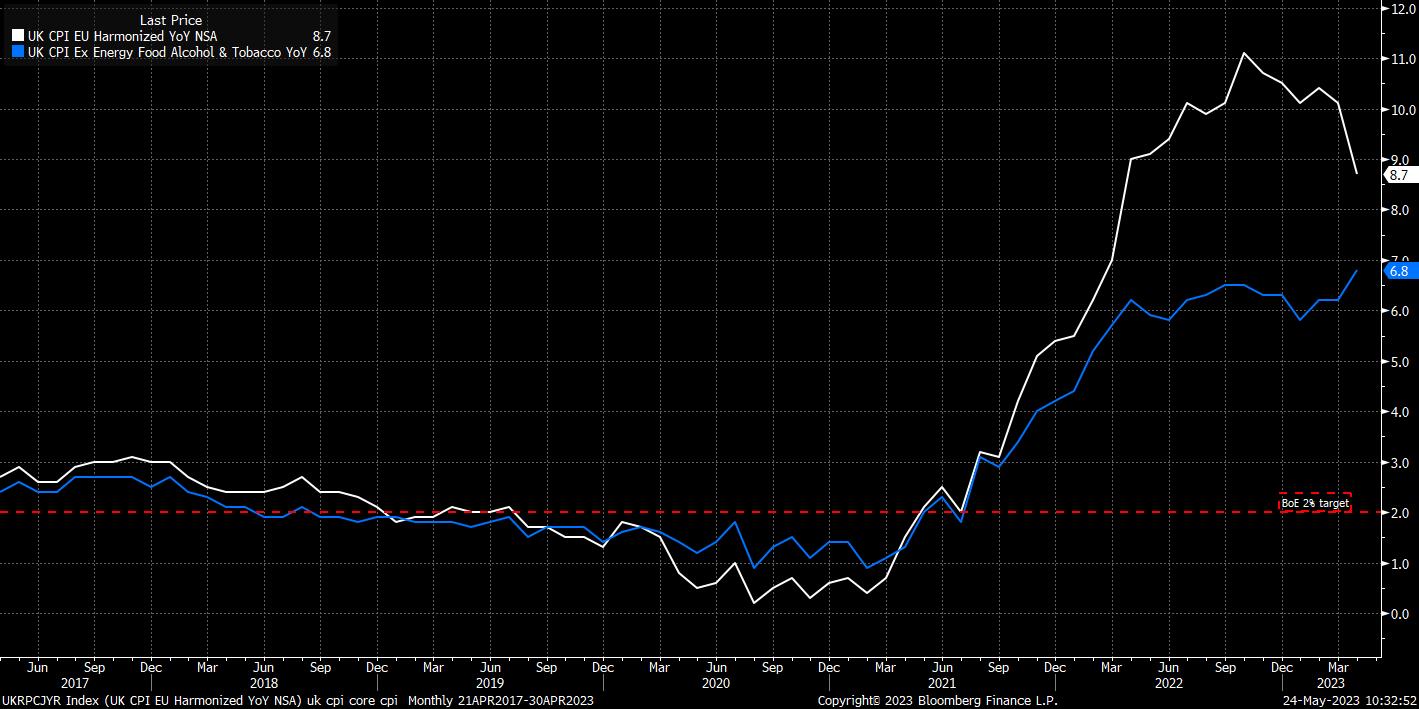

Headline CPI rose by 8.7% YoY in April. While lower than the 10.1% seen a month prior, the figure was considerably above the 8.2% consensus, and even more disappointing when one considers that almost the entire decline came by virtue of the base effects from last year’s sharp rise in energy prices, rather than any disinflationary forces currently within the economy. Food inflation remains the primary issue, rising a whopping 19.3% YoY.

Stripping out energy and food prices, however, paints no better a picture. Core CPI surged 6.8% YoY last month, the fastest pace since the early-90s, and above all estimates submitted to both Bloomberg and Reuters.

Furthermore, both metrics are considerably above the BoE’s own forecasts; Governor Bailey’s Tuesday comments that “inflation has turned a corner” are now looking very premature indeed.

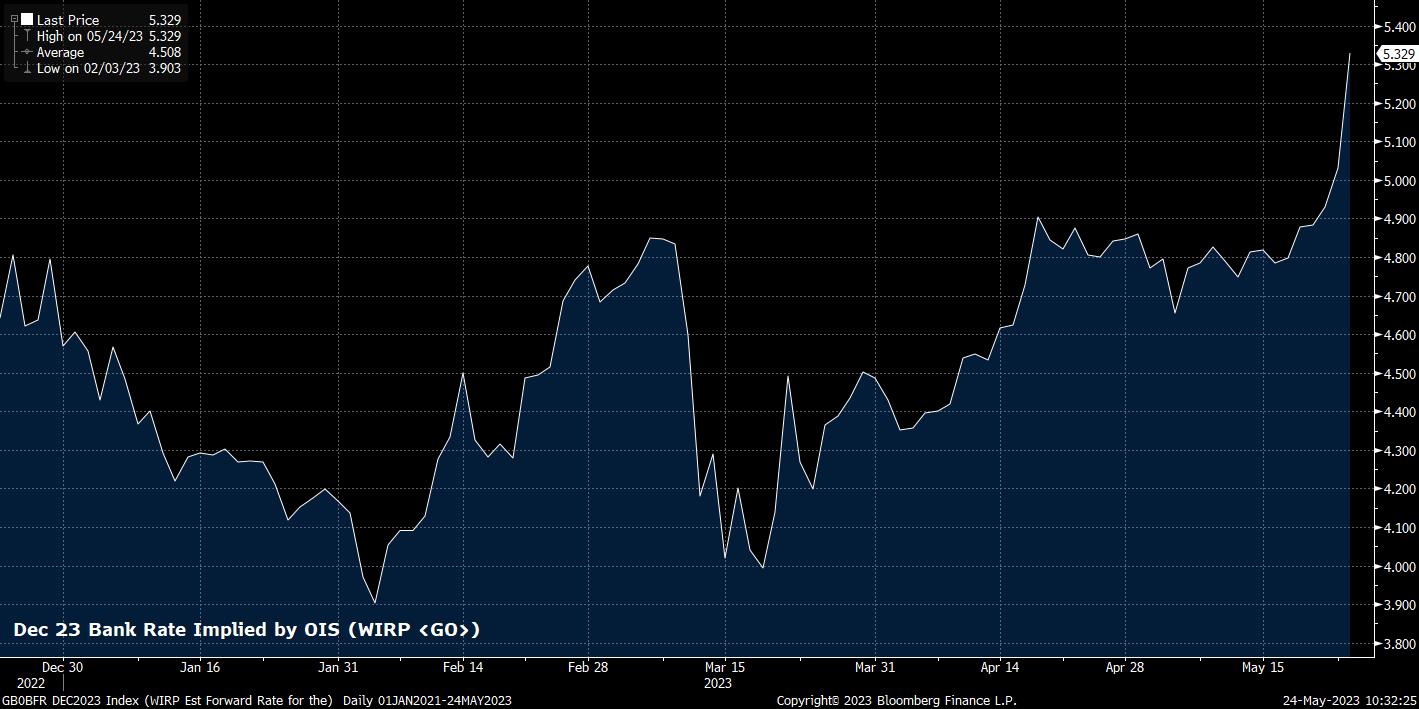

Unsurprisingly, the market has undergone a significant hawkish repricing since the data dropped. Money markets now price 30bps of tightening for the June MPC decision, fully expecting another 25bps move, plus assigning a roughly 1-in-5 chance that the BoE plump for a larger 50bps hike. Looking further ahead, markets now envisage Bank Rate peaking at 5.35% at the end of the year, up from around 5% a week ago.

Of course, the last time that markets were expecting a terminal rate around these levels was during the fall-out from PM Truss’ disastrous ‘mini-budget’. In contrast to then, the pricing feels a lot more realistic this time around, though it’s important to consider that with the BoE set to continue hiking in 25bp clips, the economy is likely to lose momentum rather too quickly to permit such a degree of tightening. Expecting a peak rate around 5% may be more realistic.

It's also important not to jump to conclusions digesting the disastrous inflation figures. There is another inflation report due before the next MPC, which will likely have a more significant impact on the decision that the Committee take.

Despite this, it is hard to argue against the UK economy being in ‘stagflation’ at this point – inflation remains high, and rising; signs of softness are beginning to emerge in the labour market; and, incoming activity data pointing to, at best, anaemic economic growth. This poses a significant headache for the BoE, one largely of their own making, and leaves few good options.

Doing nothing from here on in will only serve to make the inflation problem worse; modest further tightening would likely have little-to-no impact on inflation, but will dent economic growth; a significant degree of additional hikes, in line with market pricing, would likely have an impact on inflation, but also destroy the demand side of the economy. In short, the ‘Old Lady’ is stuck between a rock and a hard place.

Laying things out like this, it’s tough to be bullish on the GBP over the medium-term.

_2023-05-24_10-31-18.jpg)

Cable’s recent rally has rather run out of steam, with the 1.27 handle proving too much of a stretch for the quid. Since, price has fallen back into the broad 1.19 – 1.25 range which has been in place since the end of 2022, having also closed below the 50-day moving average for two days running, flipping momentum in the bears’ favour.

Shorts will be targeting a break of the recent lows at 1.2380 in order to continue recent downside momentum; a move towards the mid-1.22s seems plausible, particularly considering the hawkish Fed repricing that continues to act as a tailwind for the USD.

"لم يتم إعداد المواد المقدمة هنا وفقًا للمتطلبات القانونية المصممة لتعزيز استقلالية البحث الاستثماري، وعلى هذا النحو تعتبر بمثابة وسيلة تسويقية. في حين أنه لا يخضع لأي حظر على التعامل قبل نشر أبحاث الاستثمار، فإننا لن نسعى إلى الاستفادة من أي ميزة قبل توفيرها لعملائنا.

بيبرستون لا توضح أن المواد المقدمة هنا دقيقة أو حديثة أو كاملة ، وبالتالي لا ينبغي الاعتماد عليها على هذا النحو. لا يجب اعتبار المعلومات، سواء من طرف ثالث أم لا، على أنها توصية؛ أو عرض للشراء أو البيع؛ أو التماس عرض لشراء أو بيع أي منتج أو أداة مالية؛ أو للمشاركة في أي استراتيجية تداول معينة. لا يأخذ في الاعتبار الوضع المالي للقراء أو أهداف الاستثمار. ننصح القراء لهذا المحتوى بطلب المشورة الخاصة بهم والإستعانة بخبير مالي. بدون موافقة بيبرستون، لا يُسمح بإعادة إنتاج هذه المعلومات أو إعادة توزيعها.

تداول العقود مقابل الفروقات والعملات الأجنبية محفوف بالمخاطر. أنت لا تملك الأصول الأساسية و ليس لديك أي حقوق عليها. إنها ليست مناسبة للجميع ، وإذا كنت عميلاً محترفًا ، فقد يؤدي ذلك إلى خسارة أكبر من استثمارك الأساسي. الأداء السابق في الأسواق المالية ليس مؤشرا على الأداء المستقبلي. يرجى النظر في المخاطر التي تنطوي عليها، والحصول على مشورة مستقلة وقراءة بيان الإفصاح عن المنتج والوثائق القانونية ذات الصلة (المتاحة على موقعنا على الإنترنت www.pepperstone.com) قبل اتخاذ قرار التداول أو الاستثمار.

هذه المعلومات غير مخصصة للتوزيع / الاستخدام من قبل أي شخص في أي بلد يكون فيه هذا التوزيع / الاستخدام مخالفًا للقوانين المحلية."