Tech’s Dwindling Rate Sensitivity

Before getting on to that, however, it’s necessary to delve into the weeds of bond maths, and outline some definitions.

As noted above, duration is a mathematical concept that refers to the sensitivity of an asset – typically a bond – to changes in interest rates; the higher the duration, the more sensitive an asset is to shifts in rates, and vice versa. Bond duration is relatively easy to measure, as fixed income products pay a regular amount, on a fixed schedule, for the life of the instrument. In contrast, equities do not necessarily pay a regular amount on a regular timescale, with said payments instead being constructed as dividends, which are paid subject to a company’s performance and financial situation at a given time. With this in mind, one could consider equity duration as a measure of how long an investor must receive dividends in order to be repaid the purchase price of the stock. It is that irregularity of cash flows that makes equity duration difficult to measure and means that, at best, it is only possible to approximate a value for such a concept.

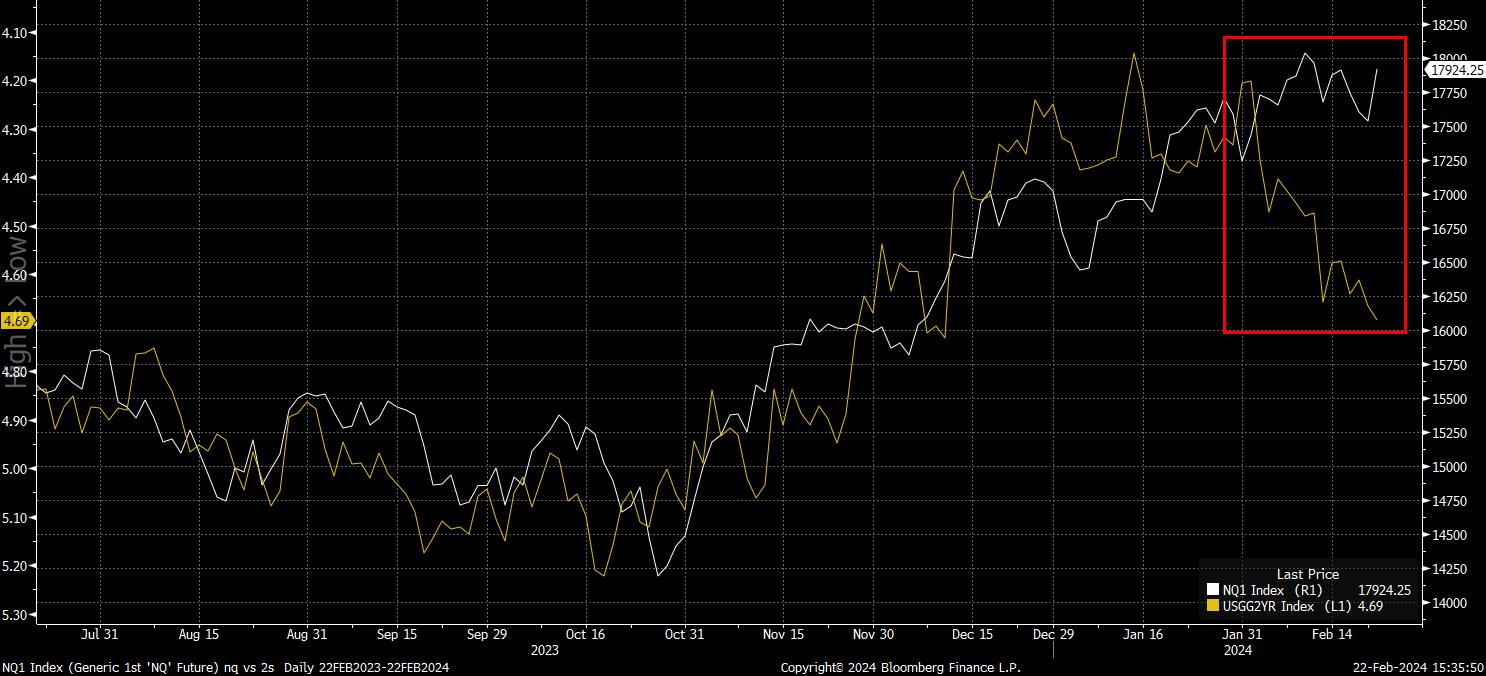

With all of that said and done, there are ways that one is able to gauge the relationship between equities and fixed income. At a, perhaps, crude level, a simple overlay chart helps to paint a picture – as shown below, the inverse relationship (2s are on an inverted Y-axis here) between front-end rates and the Nasdaq 100 has broken down since the end of January.

Alternatively, for those of a statistical persuasion, one can look at the correlation between equity and bond prices. This is exactly what I’ve done below, in examining the 20-day correlation between a market-cap weighted index of ‘magnificent seven’ stocks, and the 2-year Treasury yield.

As is easy to see, the correlation between the two has flipped positive over the last few weeks, implying that stocks and bonds are now moving in the opposite direction to each.

In any case, while all this is interesting, it means little on its own without considering the implications of such a shift.

The first is that, in contrast to what has been the prevailing logic for some time now, higher real rates may not in fact prove to be the headwind to risk that we have expected. However, on the same note, there is perhaps a case to be made that lower real rates, which are likely to prevail as central banks ease policy as the year progresses, may not prove to be as much of a boon for the tech sector as in prior cycles. Despite this, the broader policy backdrop should remain supportive for risk, with the central bank put remaining alive, and more flexible than before.

On a similar note, it could also be argued that the broader market is, perhaps, less exposed to any potential resurgence in inflation, or stickier-than-expected price pressures, owing to the less rate-sensitive nature of the market’s most dominant sector.

The final significant conclusion from all this, particularly after NVDA earnings yesterday, the tech behemoths have proved that they are able to deliver on earnings expectations, and in many cases vastly surpass said estimates, no matter the interest rate environment. Of course, this is much more of a longer-term consideration for the sector, though does bode well for longer-run profitability.

Related articles

Pepperstone不代表這裡提供的材料是準確、及時或完整的,因此不應依賴於此。這些資訊,無論來自第三方與否,不應被視為建議;或者買賣的提議;或者購買或出售任何證券、金融產品或工具的招攬;或參與任何特定的交易策略。它不考慮讀者的財務狀況或投資目標。我們建議閱讀此內容的讀者尋求自己的建議。未經Pepperstone的批准,不允許複製或重新分發此信息。