2 Out Of 2 Upside Inflation Surprises – Will CPI Be A Third?

Firstly, on Monday, the latest survey of consumer expectations from the New York Fed pointed to a noticeable uptick in both short-, and longer-run metrics:

- 1y: 3.3% vs. 3.0% prior

- 3y 2.8% vs. 2.9% prior

- 5y: 2.8% vs. 2.6% prior

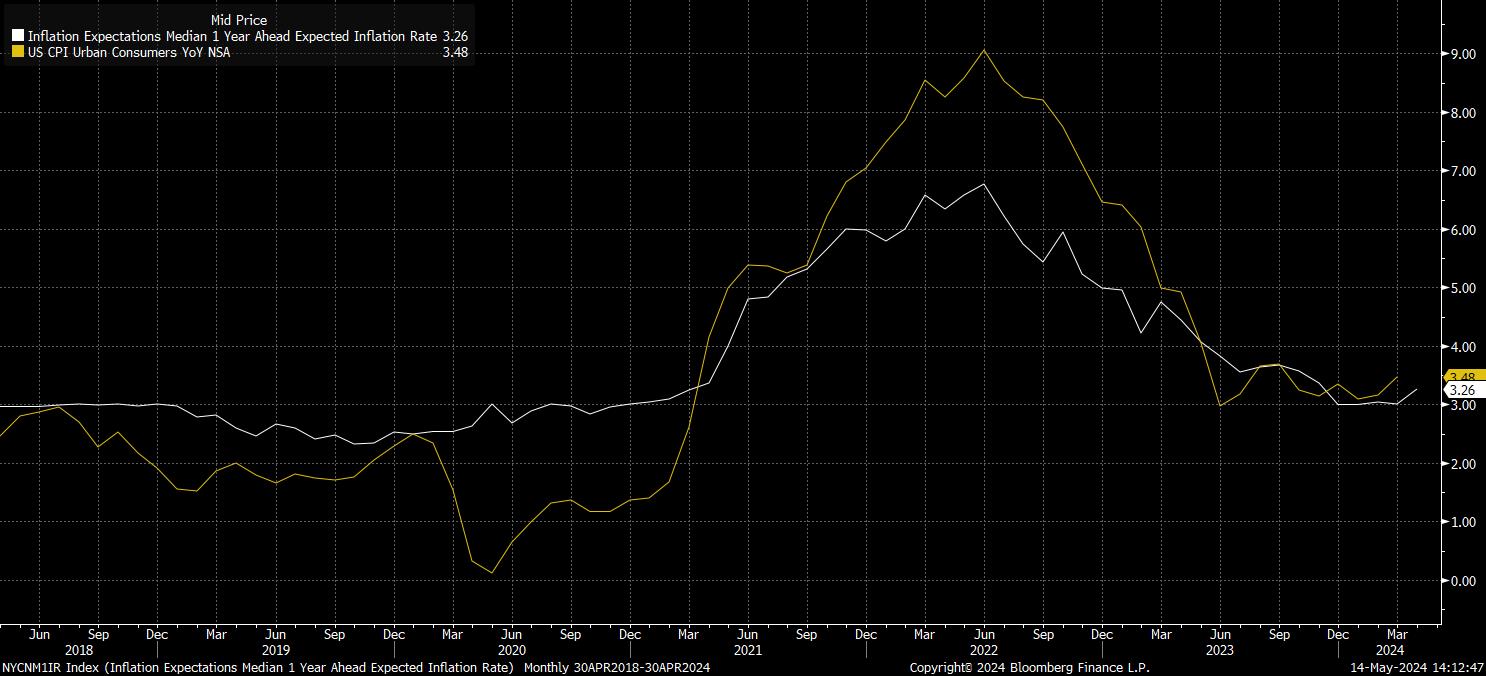

While this did elicit a modest hawkish reaction, most evidently in the front-end of the Treasury curve, there is a slight issue – consumers have an abysmal track record at predicting inflation. Shifts in inflation expectations are typically closely tied to moves in actual inflation, as opposed to the general public looking into their proverbial crystal balls to judge where inflation may end up, as the chart shows.

Secondly, PPI, which came in hotter across the board. Both headline and core PPI rose 0.5% MoM in April, while also rising by 2.2% YoY and 2.4% YoY respectively, with the annual metrics also coming in somewhat hotter than consensus had expected.

At face value, a worrying report. However, there is again something of a problem with such a top-level assessment. Digging into the data, one notices that the MoM prints were revised sharply lower in March, by 0.3pp to -0.1% MoM apiece. Hence, effectively, the 0.3pp beat vs. consensus in the April data, nets off against the downward revision to the prior month’s figures, helping to explain the short-lived nature of the hawkish cross-asset reaction seen in the aftermath of the print crossing newswires.

So, where does this leave us ahead of CPI tomorrow?

In short, I’d argue that both of the above represent more ‘noise’ than they do ‘signal’, particularly when the statistical relationship between a PPI beat and subsequent upside CPI surprise is, at best, ropey. Instead, risks to the April CPI figure appear to be relatively evenly balanced. While energy prices, driven primarily by gasoline, continued to rise on the month, food inflation was a touch soft, and used car prices also notched a relatively significant decline.

Nonetheless, with the YoY headline CPI metric having surprised to the upside of consensus expectations for three straight months, plenty will be expecting another such beat of the 3.4% median expectation.

Interestingly, the CPI fixings market is priced for a print marginally hotter than consensus on an annual level, at 3.41% YoY, while also pricing a marginally cooler than consensus MoM print, at 0.36% MoM.

Whatever, the short-term playbook over the CPI figure is relatively straightforward. A hotter-than-expected figure will likely elicit a hawkish reaction (stocks & bonds softer, USD firmer), with the magnitude of such a move greater, the greater the degree of surprise.

Naturally, the inverse is true on a cooler than expected figure, though given the aggressively hawkish nature of Fed pricing – per the USD OIS curve – with just 40bp of easing priced through year-end, the balance of risks points to a more significant reaction in the event of a cool print. This is particularly the case with the FOMC having set an incredibly high bar to delivering another hike, while also appearing somewhat desperate to cut rates, particularly in the event of potential labour market weakness.

Related articles

Pepperstone不保证这里提供的材料准确、最新或完整,因此不应依赖这些信息。这些信息,无论来自第三方与否,不应被视为推荐;或者买卖的要约;或者购买或出售任何证券、金融产品或工具的邀约;或者参与任何特定的交易策略。它不考虑读者的财务状况或投资目标。我们建议阅读此内容的任何读者寻求自己的建议。未经Pepperstone批准,不得转载或重新分发这些信息。