- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

As noted, Bank Rate should remain at a post-crisis high 5.25% this week, an outcome expected by all but two respondents to the latest Bloomberg survey, and a decision implied as a 97% probability by money markets.

Since the decision to hit the pause button at the September MPC meeting, there has been relatively little incoming economic data, with just one inflation print, and one jobs report, in the intervening period. Consequently, the vote split is likely to be similar to the 5-4 vote to maintain Bank Rate six weeks ago, with the difference that ex-Deputy Governor Cunliffe has now left the Committee, being replaced by Sarah Breeden.

It seems unlikely that the marginally more dovish Breeden will dissent at her first meeting, hence a 6-3 vote to leave Bank Rate unchanged becomes the base case for the November decision, with the 'core’ of the MPC, including Governor Bailey and Chief Economist Pill, again voting to keep policy on hold. Put simply, it is unlikely that there has been enough data to significantly change any MPC member’s view on the appropriate policy move since the last set of deliberations.

Consequently, the MPC’s policy statement is likely to broadly reiterate the sentiments of the September meeting. Once again, the MPC are set to retain a data-dependent tightening bias, noting a readiness to raise rates further “if there were evidence of more persistent inflationary pressures”, while repeating a particular emphasis on wage growth and services price inflation when determining future rate decisions. The statement should also reiterate the MPC’s view that terminal Bank Rate has now been reached, repeating the requirement for policy to be “sufficiently restrictive for sufficiently long” in order to return inflation to target.

On that note, OIS has continued to reprice in a dovish direction since the last meeting, with market pricing now largely onboard with the Bank’s own view, pricing just 7bp of further hikes this year, while foreseeing the first Bank Rate cut next September. Importantly, it is this pricing upon which the MPC’s latest economic forecasts, due at this meeting, will be conditioned.

Speaking of those forecasts, as a result of the significant dovish repricing seen since the last projections in August – at which point markets had been pricing a terminal rate around 125bp higher than at present – expectations for both GDP and CPI should receive a modest upward revision.

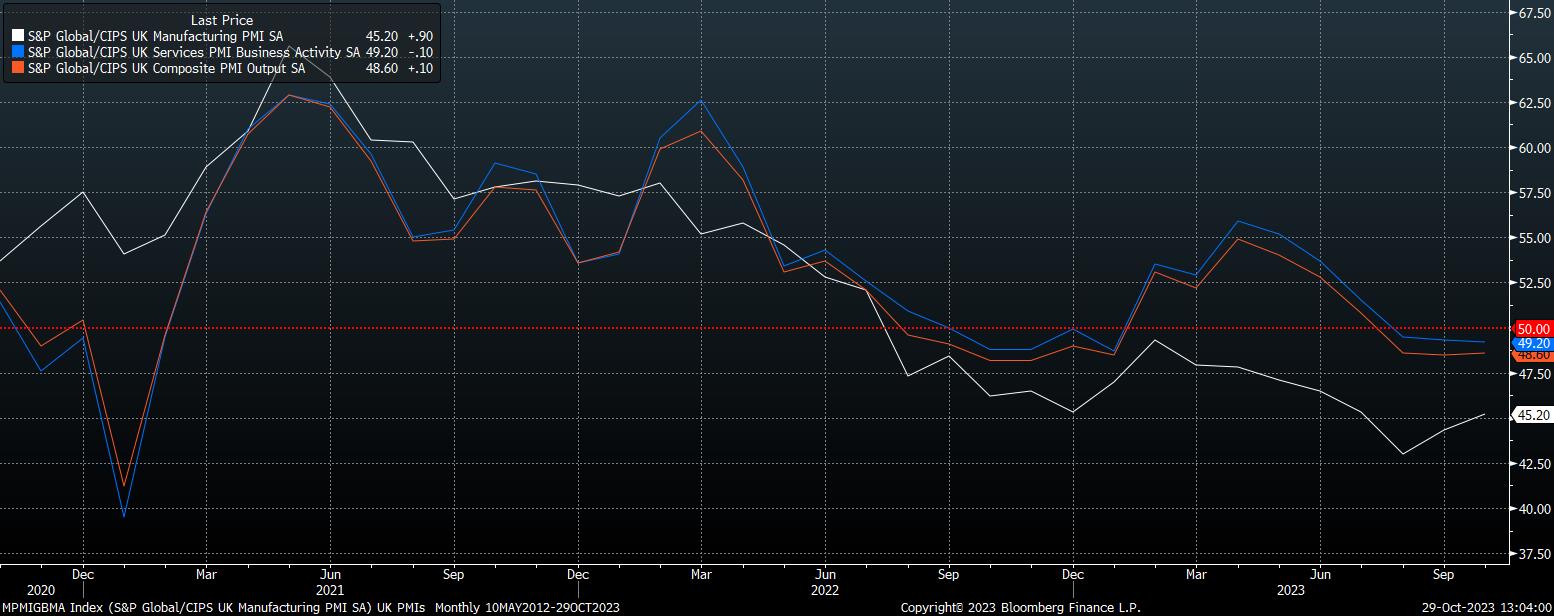

The upward GDP revision will come despite stronger evidence emerging of slowing economic momentum in the UK. Recent PMI surveys have painted an increasingly glum picture of the British economy, with the composite gauge now having printed below the 50 handle for three consecutive months, and leading indicators with the survey pointing to further pressure on the economy in the months ahead, particularly as the pace of remortgaging on to higher-fixed-rate deals continues through the winter.

Nevertheless, the substantially lower market rate path than at the time of the August forecast compilation will likely result in a mechanical upgrade to the BoE’s current expectation of 0.5% GDP growth both this year and next, and 0.3% in 2025.

Furthermore, the ONS’ recent substantial upgrade to prior GDP figures, which added almost 2% to the size of the UK economy, will also be reflected in the MPC’s latest projections, providing a further upward impulse, even if recent data points to, at best, a sluggish pace of expansion.

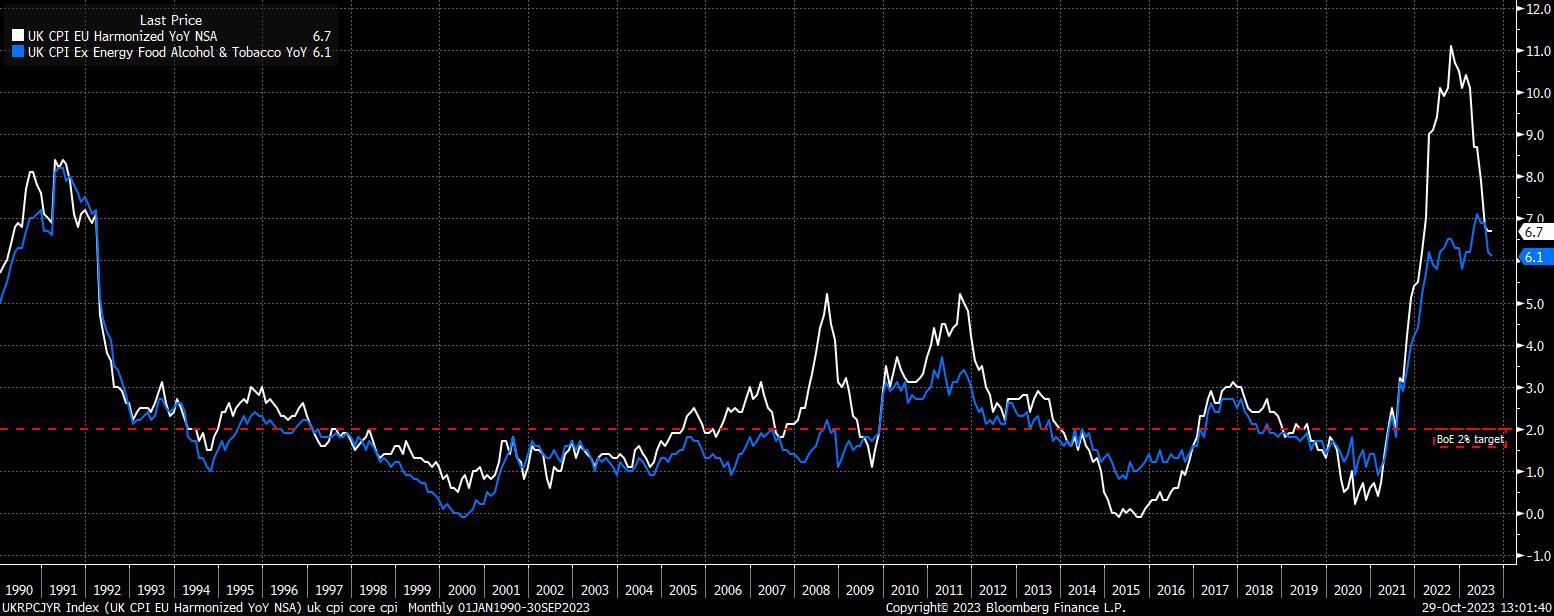

Meanwhile, on inflation the lower market rate path, along with higher energy prices amid conflict in the Middle East, should combine to cause a modestly higher CPI forecast, with risks to said forecast continuing to be described as tilting to the upside, particularly as earnings growth continues at an annual pace of over 8%.

The key question when it comes to CPI expectations, however, will be when the BoE see headline inflation falling back to the 2% target, currently expected in Q2 25. Typically, this would be interpreted as a signal that the MPC may have to tighten further, though the lack of trust in and reliability of said forecasting models means any forecast tweaks are unlikely to lead to a policy response.

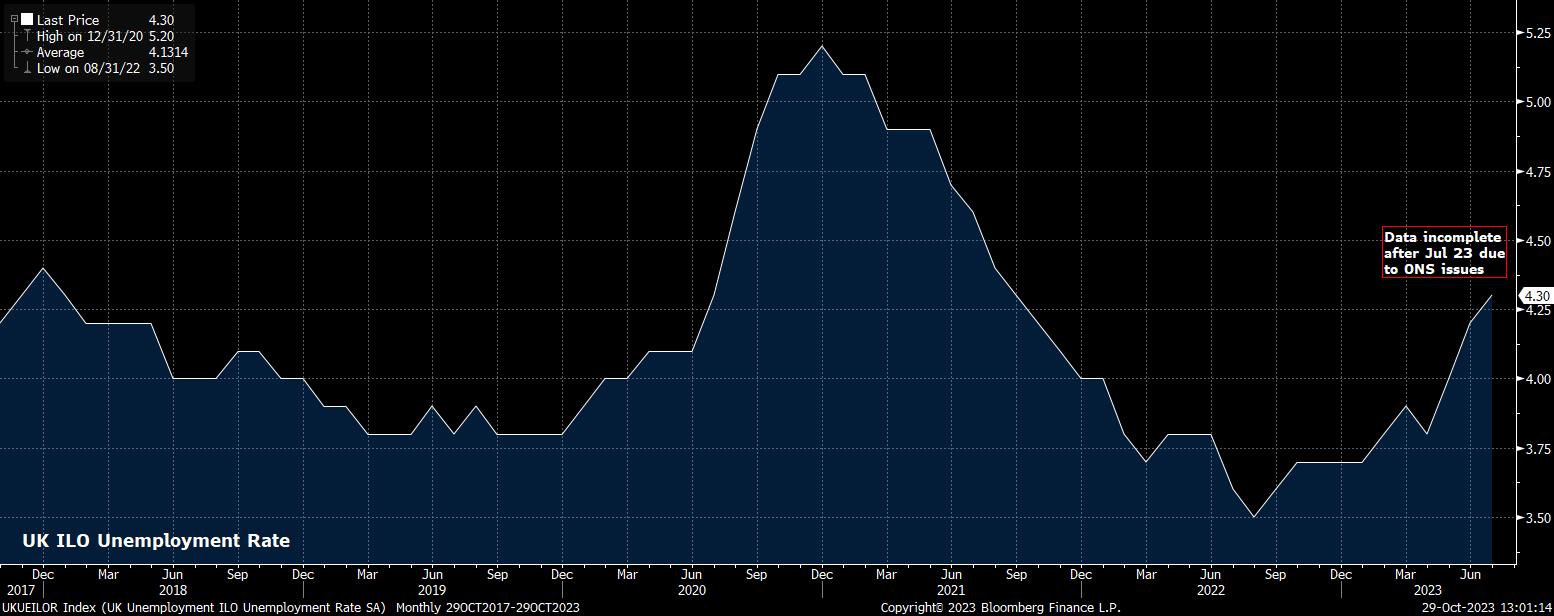

Lastly, on jobs, the MPC are unlikely to make significant revisions to their current labour market expectations, with unemployment likely to gradually rise to 4.8% by the end of the forecast horizon, as the lagged effects of the last 18 months of policy tightening are increasingly felt.

It should be noted, however, that UK employment figures are the subject of increasing questions over their reliability due to low survey response rates and the ONS introducing an ‘experimental’ methodology for data collection. Hence, both markets and policymakers are unlikely to place too much weight on any labour market statistics for the time being.

Turning to the financial markets and, as discussed earlier, the upcoming BoE decision stands out as one of the most predictable of the cycle thus far. Hence, any impact on UK assets seems set to be relatively limited, and likely short-lived.

For the GBP, risks continue to be tilted to the downside, particularly with the bar high for any form of hawkish surprise from the ‘Old Lady’ this week, and with the quid having failed miserably to regain significant ground as it has consolidated over the last couple of weeks.

_2023-10-29_12-59-40.jpg)

The bulls still require a close back above the 1.23 handle, and ideally the 50-day moving average, to regain control. However, these upside targets appear a stretch for now, with key support at 1.2110 coming under increasing pressure, and a closing break below this level likely leaving the pair targeting the 1.20 figure in relatively short order.

As for equities, the FTSE 100 has for some time now taken little notice of BoE decisions, instead being driven largely by fluctuations in the value of the GBP, and more broadly shifts in global risk appetite.

Consequently, the London market has endured a rather tough time of late, as geopolitical risk has been increasingly priced into markets amid rising tensions in the Middle East, seeing the FTSE 100 fall almost 7% from its September peak. The bulls will be looking for support around the 7,200 figure to hold firm, though technical levels mean relatively little amid the volatile and fluid geopolitical backdrop.

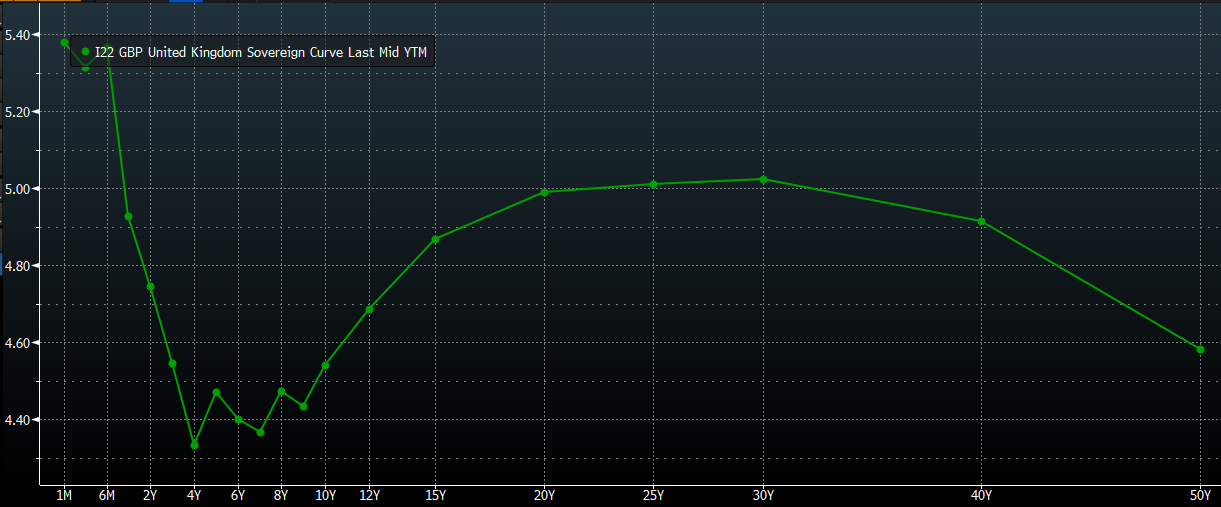

Finally, in fixed income, front-end gilts appear well-priced based upon the current policy stance.

2-year yields have held steady just shy of 5% for some time now, while the 10-year tenor has traded in a tight range since July, having proved somewhat immune to the brutal sell-off that has been taking place at the long-end of sovereign curves elsewhere in DM. Any dramatic moves stemming from Thursday’s BoE announcement appear unlikely, particularly with bonds likely more focused on global developments, such as the US Treasury’s quarterly refunding announcement.

Related articles

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.