- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

- English

- 简体中文

- 繁体中文

- ไทย

- Tiếng Việt

- Español

- Português

- لغة عربية

ISM manufacturing preview: Four reasons it could move markets

The Federal Reserve needs more conviction to implement a rate cut, and that conviction will be found in economic data releases throughout March. One of the first releases is the ISM manufacturing index, which prints 3 March (AEDT). It will be an early insight into the magnitude of supply disruptions US companies have faced.

Here’s four reasons why this data release matters in March.

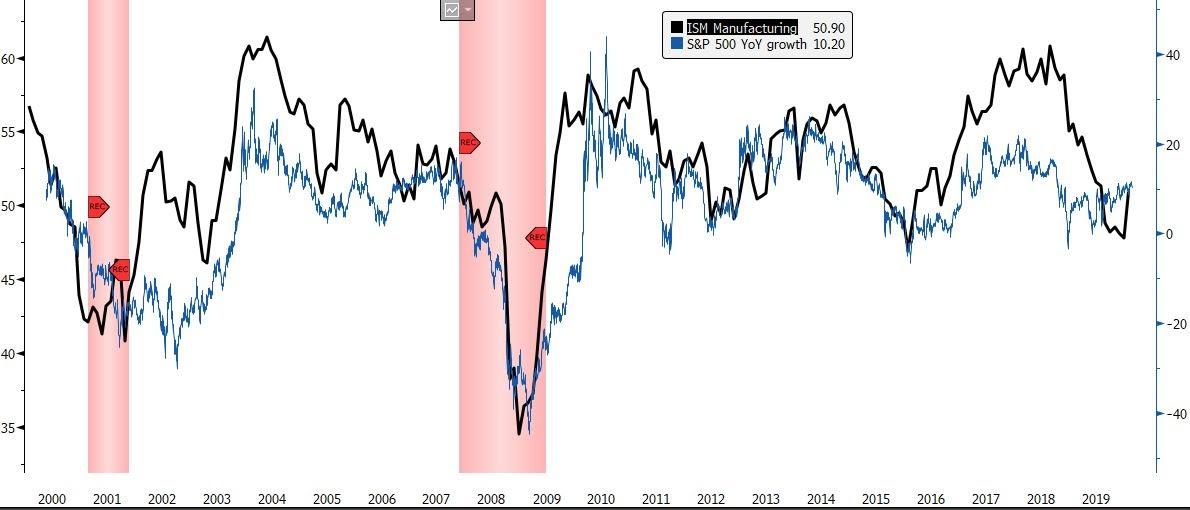

1. ISM always matters

First of all, it’s important to know that markets usually pay close attention to the manufacturing index, and the chart below shows why. It has long been a leading indicator of annual growth in the S&P 500 index. Strong manufacturing data tends to indicate stronger annual S&P growth. The same is true in the opposite.

You see better growth in the S&P when ISM manufacturing is in expansion. With expectations of 51.0, it’s an easy stumble for ISM to print below 50, in contraction, and spook markets.

Last week’s PMI release was met with a considerable market response. Markets don’t typically pay much attention to this data print, yet equities sold off when PMI services revealed contraction with a print of 49.4. The response to usually unimportant data makes the ISM release even more important than normal this time.

2. US outperformance and USD strength

The USD has mostly outperformed the rest of the world during the coronavirus outbreak due to its relative isolation from the panic and being less reliant on global trade than other countries. That all looks in dispute now that President Trump has acknowledged the risk of an outbreak in the USA.

But let’s say the data prints above expectations of 51.0, showing the US has been more resilient to global supply disruptions than expected. It would maintain faith in the strong US economy and that it can better withstand a global downturn than others due to it being more self-reliant.

A higher print would provide markets a moment of relief and perhaps a small rebound until the next bout of bad news.

3. ISM manufacturing, gold, and the prospect of a weaker USD

Let’s now consider that ISM manufacturing goes the other way and prints below the consensus of 51.0. A print below 51 will be bad news, but particularly a move below 50, which indicates contraction. This would tell markets that the US is indeed vulnerable to the virus fallout and could spark a move to safe havens and further equity sell-offs.

Although the US relies less on global trade than most other nations, its manufacturing could have still taken a considerable hit. Whether global supply chain disruptions or reduced demand for US exports from virus-affected nations, major US companies, including Apple, United Airlines, and Mastercard, have announced short-term revenue targets will not be met. The fear is that these are only the first companies to announce disruption and there could be many more to come. US equities have priced in this risk in the last few days with a serious correction, with the S&P 500 falling over 350 points. A bad ISM print could be taken as confirmation that the US economy and its companies will face considerable virus disruption. That takes us to point four: Fed policy.

4. Fed policy

The sentiment from the Fed continues to be that policy is well-calibrated and any CoVID-19 economic fallout is expected to be short and the shock absorbed by a strong US economy.

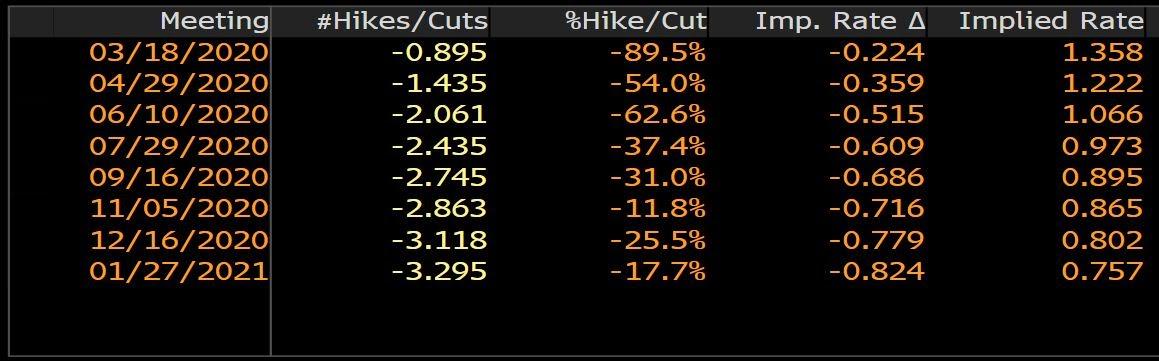

Despite the Fed’s upheld optimism, markets are pricing higher probabilities of rate cuts as virus panic increases. There are now three full rate cuts priced for this year, with a 90% chance of a 25 basis point (bp) cut priced in for the March meeting.

US Federal Funds implied rate. Markets are pricing a 90% chance of a rate cut at the March meeting, with three full cuts priced by December.

Source: Bloomberg

The Fed will be awaiting data before they reconsider their optimistic stance and the ISM is the first of many prints that will take their attention, although it won’t be enough in isolation. The Fed will also consider employment and inflation data, among others.

If next week’s ISM data is particularly poor, this would be further justification for the equity sell-off that wiped over four months worth of gains, and could even encourage more declines.

The Fed would then be pressured to address the markets and either respond with a cut, or continue to assure markets that policy is, in their view, well-adjusted and the strong US economy can absorb any temporary virus supply shock.

Otherwise if it prints at or above expectations, markets will be calmer and might quietly bid up the troubled equity market, and will give more breathing space for the Fed to ride out the storm.

Higher chances of a rate cut means a weaker USD. The greenback has been a safe haven during the virus outbreak so if that hot USD begins to cool, money will flow into the traditional safe havens: JPY, CHF, and notably gold.

I bring attention to gold because there are several cases of the virus in Japan and one reported in Switzerland. If these numbers increased and materially impacted the countries’ production, it could weigh on the currencies. Gold is the purest, safe hedge against a virus spreading to every corner of the world.

Ready to trade?

It's quick and easy to get started. Apply in minutes with our simple application process.

The material provided here has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Whilst it is not subject to any prohibition on dealing ahead of the dissemination of investment research we will not seek to take any advantage before providing it to our clients.

Pepperstone doesn’t represent that the material provided here is accurate, current or complete, and therefore shouldn’t be relied upon as such. The information, whether from a third party or not, isn’t to be considered as a recommendation; or an offer to buy or sell; or the solicitation of an offer to buy or sell any security, financial product or instrument; or to participate in any particular trading strategy. It does not take into account readers’ financial situation or investment objectives. We advise any readers of this content to seek their own advice. Without the approval of Pepperstone, reproduction or redistribution of this information isn’t permitted.